{kind=link}

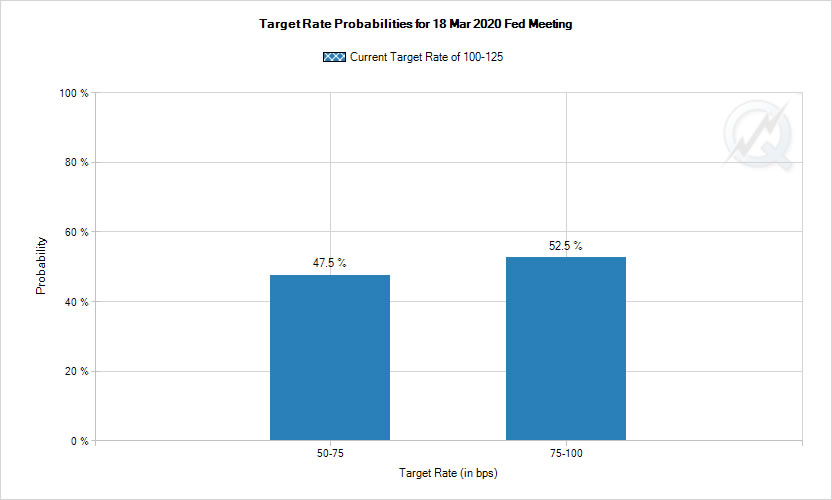

Commodity currencies are back under pressure today, led by Aussie, as Europe equities are back in red. DOW futures point to a deep gap down. Wuhan coronavirus pandemic continues to spread all over the world and it’s accelerating. Yen and Swiss Franc are the strongest today, followed by a recently turned safe-haven Euro. Dollar is mixed as it’s rally attempts are capped by expectation of more Fed rate cut. Even after this week’s -50bps cut, fed funds futures are pricing in 47 chance of another -50bps cut on March 18, and 52.5% chance of a -25bps cut. That is, a cut is fully priced in, just a matter of size.

South Korea’s cases showed no sign of slowing, reaching 6088, with 40 deaths. Iran surpassed Italy as number two affected country outside China, with 3513 cases and 107 deaths. In Europe, Italy remain the most serious one with 3089 cases and 107 deaths. Germany, with 444 cases is catching up, while France has 285 cases and 4 deaths, Spain has 248 cases and 3 deaths Switzerland (95) and UK (90) will likely break 100 soon. 361 cases are reported Japan so far, 162 in the US.

In Europe, currently, FTSE is down -1.96%. DAX is down -2.03%. CAC is down -2.16%. German 10-year yield is down -0.0186 at -0.655. Earlier in Asia, Nikkei rose 1.09%. Hong Kong HSI rose 2.08%. China Shanghai SSE rose 1.99%. Singapore Strait Times dropped -0.22%. Japan 10-year JGB yield rose 0.0295 to -0.111.

US initial jobless claims dropped to 216k, matched expectations

US initial jobless claims dropped -3k to 216k in the week ending February 29, matched expectations. Four-week moving average of initial claims rose 3.25k to 213k. Continuing claims rose 7k to 1.729m in the week ending February 22. Four-week moving average of continuing claims dropped-7.5k to 1.721m.

Q4 non-farm productivity was revised down to 1.2%. Unit labor costs was revised down to 0.9%.

BDI: German industrial sector to stay in recession this year

Germany’s BDI industry group said in a report today that “the industrial sector is likely to remain in recession” this year. That would be the “longest since reunification” in 1990.

It added, “With the production slumps in China and the quarantine measures taken by individual countries, it is becoming clear how vulnerable the export-oriented and internationally organized German economy is.”

Separately, VDMA engineering association economist Ralph Wiechers also said, “we have to expect disruptions along the supply chain from China to Germany.”

Italy to spend EUR 5B on coronavirus support

Italy’s Deputy Economy Minister Laura Castelli indicated that the government will likely raise coronavirus support spending to EUR 5B. She added that it’s “necessary to raise the bar as much as possible, also considering the fact that Italy has registered a lower than expected deficit”. It’s believed that the government is also considering to ask for a temporary suspension of EU’s European Stability and Growth Pact, which limits the country’s spending.

Economy Minister has promised fiscal stimulus of EUR 3.6B, including tax break and other measures. But that seems insufficient since Italy is now the third country that’s most affected by coronavirus pandemic, with 3089 cases and 107 deaths. Measures could include supporting parents to stay home to take care of their children, increase in healthcare funding and temporary redundancy benefits.

Education Minister Lucia Azzolina said schools and universities all over the country would be closed from Thursday until at least March 15.

Serious divergences between EU and UK for post Brexit relationships

EU chief Brexit negotiator Michel Barnier warned that there are “serious divergences” with the UK, after ending the first week of negotiations on post Brexit relationship. The talks were held in a “constructive spirit” but in a “demanding context”.

In particular, he pointed four areas that are at odds, including competition policy, cooperation in criminal justice matters, control of U.K. fishing waters, and on the way any deal would be structured.

Nevertheless, Barnier remained hopeful as “there are many serious divergences, an agreement is possible — even if difficult.”

76% of UK firms expect Brexit uncertainty to persist until at least 2021

BoE’s Monthly Decision Maker Panel report noted that “Businesses expect uncertainties around Brexit to take longer to be resolved than in the January survey.” 76% of businesses expected uncertainty to persist until at least 2021, sharply higher than 59% in January survey.

Only 4% said they’re fully prepared for potential extra requirements for trading with EU. 38% were as ready as they can be, 31% partially prepared and 5% not prepared at all. 39% said increased tariffs is the most significant obstacles for trading with EU, 36% said restrictions on movement of people, 30% said custom declarations and checks.

IMF: Global growth in 2020 will be lower than 2.9%

IMF announced a USD 50B aid package for low-income and emerging market countries, to help combat the impact of the Wuhan coronavirus global outbreak. USD 10B in rapid-disbursing emergency financing is available for low-income countries. The rapid financing instrument will provide USD 50B for emerging markets.

Managing Director Kristalina Georgieva said global growth in 2020 will “dip below” 2.9% for 2019. That is, at least 0.4% worse than 3.3% growth projection for 2020 as estimated in January. She warned that “how far it will fall and how long the impact will be is still difficult to predict”.

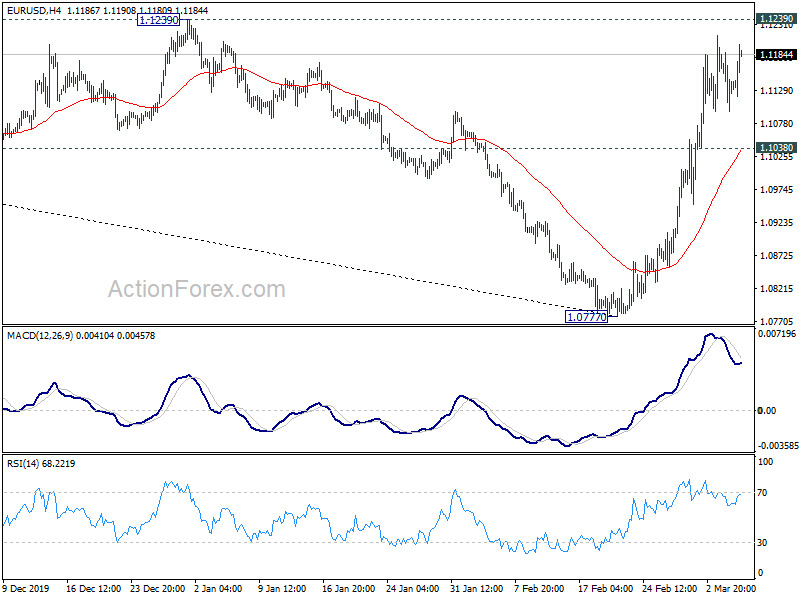

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1091; (P) 1.1139; (R1) 1.1182; More…

Intraday bias in EUR/USD remains neutral with focus on 1.1239 key resistance. Decisive break of 1.1239 will confirm medium term bottoming at 1.0777 and turn outlook bullish.. On the downside, break of 1.1038 minor support will turn bias back to the downside for retesting 1.0777 low. That would also retain near term bearishness.

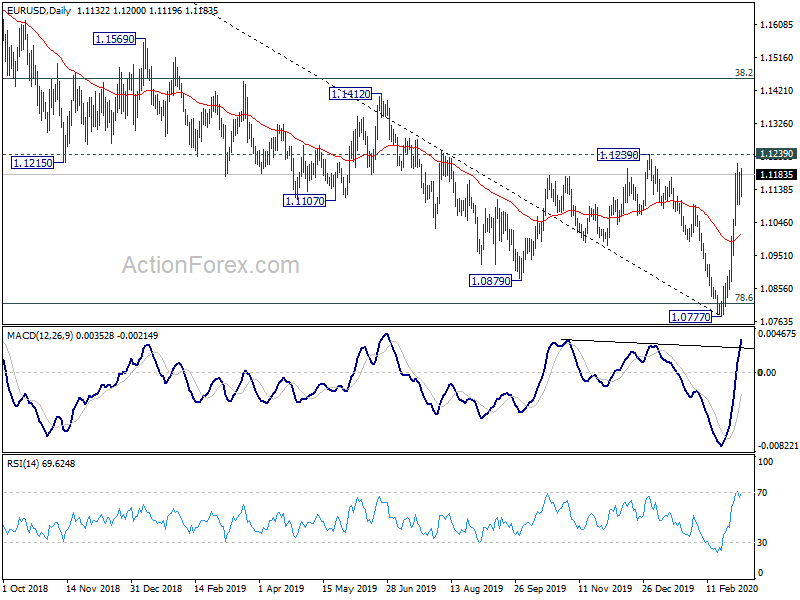

In the bigger picture, as long as 1.1239 resistance holds, larger down trend from 1.2555 (2018 high) is still in favor to extend through 1.0777 low. However, sustained break of 1.1239 will also have 55 week EMA (1.1154) decisive taken out. That should confirm medium term bottoming, with bullish convergence condition in weekly MACD. Further rise could then be seen back to 38.2% retracement of 1.2555 to 1.0777 at 1.1456 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Jan | 5.21B | 4.80B | 5.22B | 5.38B |

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | -26.30% | 27.80% | ||

| 13:30 | USD | Initial Jobless Claims (Feb 28) | 216K | 216K | 219K | |

| 13:30 | USD | Nonfarm Productivity Q4 | 1.20% | 1.40% | 1.40% | |

| 13:30 | USD | Unit Labor Costs Q4 | 0.90% | 1.40% | 1.40% | |

| 15:00 | USD | Factory Orders M/M Jan | -0.30% | 1.80% | ||

| 15:30 | USD | Natural Gas Storage | -112B | -143B |