{kind=link}

Dollar remains generally firm today as supported by solid job and manufacturing data. Euro’s selloff seem to have temporary passed a near term climate and focuses turn to other major currencies. Australian Dollar suffer deep selling after job data, dragging New Zealand Dollar lower. Meanwhile, Yen is closing following as markets are deeply concerned with the economic and political of contagion of China’s Wuhan coronavirus. Sterling is not too far behind, partly thanks to the rebound in EUR/GBP after depending a key support level.

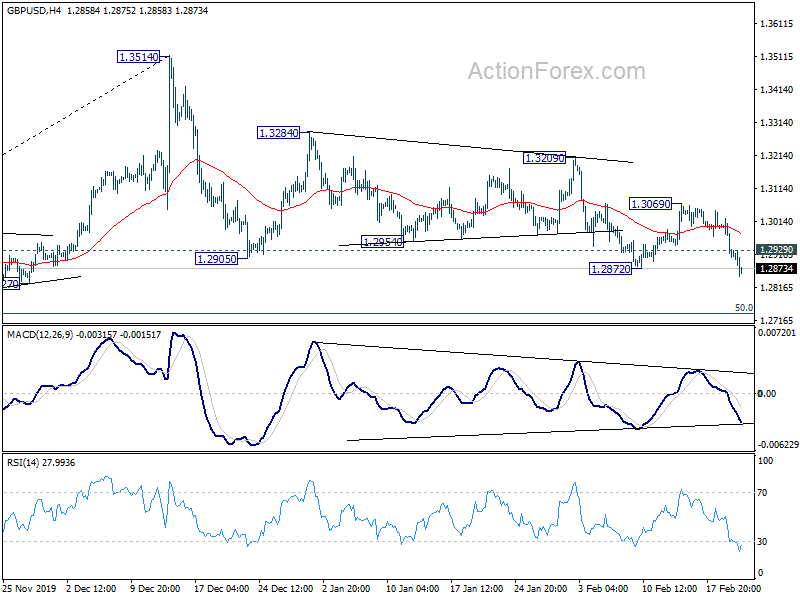

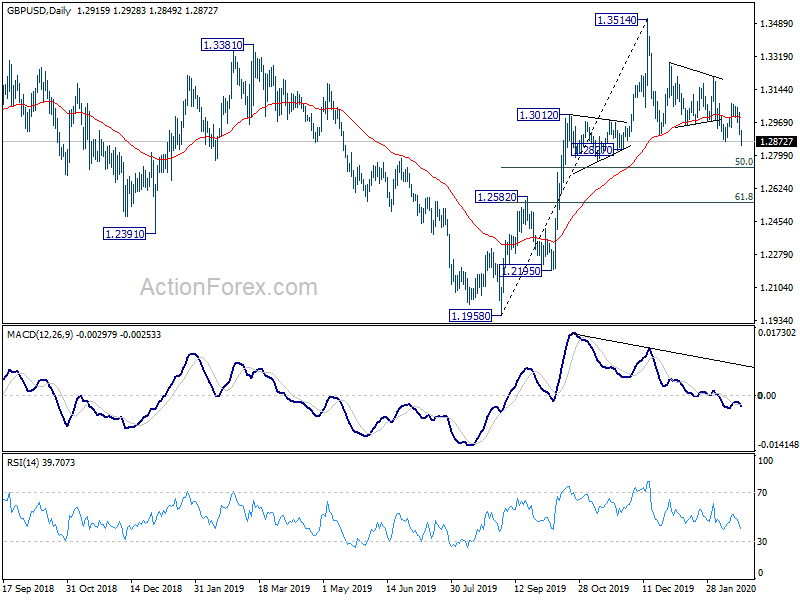

Technically, GBP/USD’s break of 1.2872 support suggests resumption of whole corrective fall from 1.3514. Next target is 1.2736 fibonacci level. EUR/GBP defended 0.8762 key support and rebounded strongly. Further rise should be seen back towards 0.8537/8595 resistance zone. USD/CHF continues to lose upside momentum just ahead of 0.9851 fibonacci level. The next move, a break of the fibonacci resistance or rejection from there, could depend on whether EUR/CHF could get rid of 1.0608 temporary low.

In Europe, currently, FTSE is down -0.02%. DAX is down -0.25%. CAC is down -0.30%. German 10-year yield is down -0.0143 to -0.430. Earlier in Asia, Nikkei rose 0.34%. Hong Kong HSI dropped -0.17%. China Shanghai SSE rose 1.84%. Singapore Strait Times dropped -0.47%.

Philly Fed manufacturing index rose to 36.7, highest since Feb 2017

Philadelphia Fed manufacturing outlook index rose to 36.7 in February, up from 17, beat expectation of 12. That’s also the highest reading since February 2017. Current indicators for general activity, new orders, and shipments increased this month, suggesting more widespread growth. Future indexes also showed improvement, indicating continuation of growth in the next six months.

Initial jobless claims rose 4k to 210k in the week ending February 15, matched expectations. Four-week moving average dropped -3.25k to 209k. Continuing claims rose 25k to 1.726m in the week ending February 8. Four-week moving average of continuing claims dropped -5.25k to 1.772m.

From Canada, ADP employment grew 25.9k in January. New housing price index rose 0.0% mom.

ECB: Sept easing package gradually transmitted to the economy

In the accounts of ECB January 22-23 meeting, it’s noted that the package of stimulus measures announced last September “have lowered term premia and contributed to the overall substantial easing in financial conditions.” There were also “indications” that the package was “being gradually transmitted to the economy”.

“Market sentiment had turned positive and risk appetite among market participants seemed strong.” Additionally, “uncertainties were perceived as receding”, mainly due to US-China trade deal and stabilization in economy outlook. But monetary policy “had to remain highly accommodative for a prolonged period of time”, with inflation “still far away” from target, and “robust convergence” of inflation towards target was “not yet assured”.

Meanwhile, “risks remained tilted to the downside” even though they had become “less pronounced”. Also, “it was cautioned that a more optimistic outlook for the economy needed to be communicated carefully in order not to give rise to a premature tightening of financial conditions.”

ECB de Guindos: Eurozone underlying fundamentals for moderate expansion remain in place

ECB Vice President Luis de Guindos said today that “the underlying fundamentals for a continued though moderate expansion of the euro area economy remain in place, as foreseen in the December 2019 Eurosystem staff projections.” However, “risks surrounding the euro area remain tilted to the downside.. In particular, the outbreak of the coronavirus and its potential effect on global growth add a new layer of uncertainty.”

Germany Gfk consumer sentiment dropped to -9.8, coronavirus weighs

Germany Gfk consumer sentiment for March dropped slightly by -0.1 to 9.8, matched expectations. Nevertheless, on the positive side, economic expectations rose for the second consecutive month, up from -3.7 to 1.2, back above long term average around 0.

“The consumer climate has been unable to continue the previous month’s positive trend. The spread of the coronavirus has undoubtedly contributed to uncertainty among consumers,” explains Rolf Bürkl, consumer expert at GfK.

“A decline or halt in production in companies in China triggered by the virus could affect production in Germany as well, or even cause it to come to a complete standstill. This could result in reduced working hours and possibly reductions in staff. And this would not be of benefit to consumer confidence.”

Also released, Germany PPI rose 0.8% mom, 0.2% yoy in January. Swiss trade surplus widened to CHF 4.78B in January.

UK retail sales rose 0.9%, ex-fuel sales rose 1.6%

UK retail sales rose 0.9% mom in January, much higher than expectation of 0.4% mom. Retail sales ex-fuel rose 1.6% mom, also much higher than expectation of 0.6% mom. On quantity bought terms, non-store retailing rose 0.3% mom, non-foodstores rose 0.5% mom, food stores rose 0.7% mom.

CBI industrial trends orders rose to -18 in February.

Australia unemployment rate surged to 5.3%, adds to case of April RBA cut

Australia employment grew 13.5k in January, better than expectation of 10.0k. Full time jobs rose 46.2k while part-time jobs dropped -32.7k. But unemployment rate surged to 5.3%, up from 5.1%, worse than expectation of 5.1%. Participation rate rose 0.1% to 66.1%.

The surge in unemployment rate somewhat deviates from RBA’s expectation that it will stay in 5.00-5.25% range for some time before falling to 4.75% in 2021. Also, it has to be considered that the impact of coronavirus outbreak in China hasn’t been reflected there. There is risk of a sudden spike in the data of the coming months. Today’s data adds much weight to the case for RBA to finally deliver another rate cut in April, after much hesitation.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2878; (P) 1.2951; (R1) 1.2993; More…

GBP/USD’s break of 1.2872 support suggests resumption of whole corrective fall from 1.3514. Intraday bias is back on the downside for 50% retracement of 1.1958 to 1.3514 at 1.2736 next. On the downside, above 1.2929 minor resistance will turn intraday bias neutral first. But further fall is expected as long as 1.3069 resistance holds, in case of recovery.

In the bigger picture, rise from 1.1958 medium term bottom is not completed yet despite current pull back form 1.3514. Such rally is expected to resume later to 1.4376 key resistance. Reactions from there would decide whether it’s in consolidation from 1.1946 (2016 low). Or, firm break of 1.4376 will indicate long term bullish reversal. In any case, for now, outlook will stay bullish as long as 1.2582 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI – Input Q/Q Q4 | 0.10% | 0.40% | 0.90% | |

| 21:45 | NZD | PPI – Output Q/Q Q4 | 0.40% | 0.30% | 1.00% | |

| 00:30 | AUD | Employment Change Jan | 13.5K | 10.0K | 28.9K | 28.7K |

| 00:30 | AUD | Unemployment Rate Jan | 5.30% | 5.20% | 5.10% | |

| 07:00 | CHF | Trade Balance (CHF) Jan | 4.78B | 2.54B | 1.96B | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Mar | 9.8 | 9.8 | 9.9 | |

| 07:00 | EUR | Germany PPI M/M Jan | 0.80% | 0.20% | 0.10% | |

| 07:00 | EUR | Germany PPI Y/Y Jan | 0.20% | -0.20% | -0.20% | |

| 09:30 | GBP | Retail Sales M/M Jan | 0.90% | 0.40% | -0.60% | -0.50% |

| 09:30 | GBP | Retail Sales Y/Y Jan | 0.80% | 0.40% | 0.90% | |

| 09:30 | GBP | Retail Sales ex-Fuel M/M Jan | 1.60% | 0.60% | -0.80% | |

| 09:30 | GBP | Retail Sales ex-Fuel Y/Y Jan | 1.20% | 0.70% | 0.70% | |

| 11:00 | GBP | CBI Industrial Trends Orders Feb | -18 | -19 | -22 | |

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | CAD | ADP Employment Change Jan | 25.9K | 46.2K | ||

| 13:30 | CAD | New Housing Price Index M/M Jan | 0.00% | 0.20% | 0.20% | |

| 13:30 | USD | Initial Jobless Claims (Feb 14) | 210K | 210K | 205K | 206K |

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Feb | 36.7 | 12 | 17 | |

| 15:00 | EUR | Eurozone Consumer Confidence Feb P | -8 | -8 | ||

| 15:30 | USD | Natural Gas Storage | -143B | -115B | ||

| 16:00 | USD | Crude Oil Inventories | 3.3M | 7.5M |