{kind=link}

Global stock markets tumble today after China reported a strong daily increase of 15152 Wuhan coronavirus cases on February 12. That was a huge difference from 2015 new cases reported for a day ago. However, the mass difference was due to change in counting method in Hubei province, which is epicenter of the outbreak. It appears that other provinces are not up to speed with the counting method change yet. The overall announcements show deep disorganization in the Chinese government in fighting the outbreak and raise deep concerns over transparency and accuracy of the data, as well as the situation.

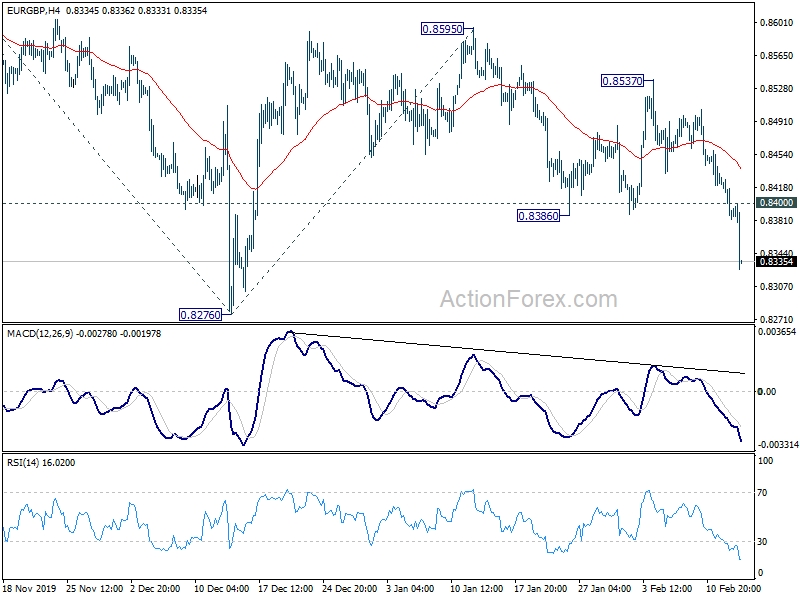

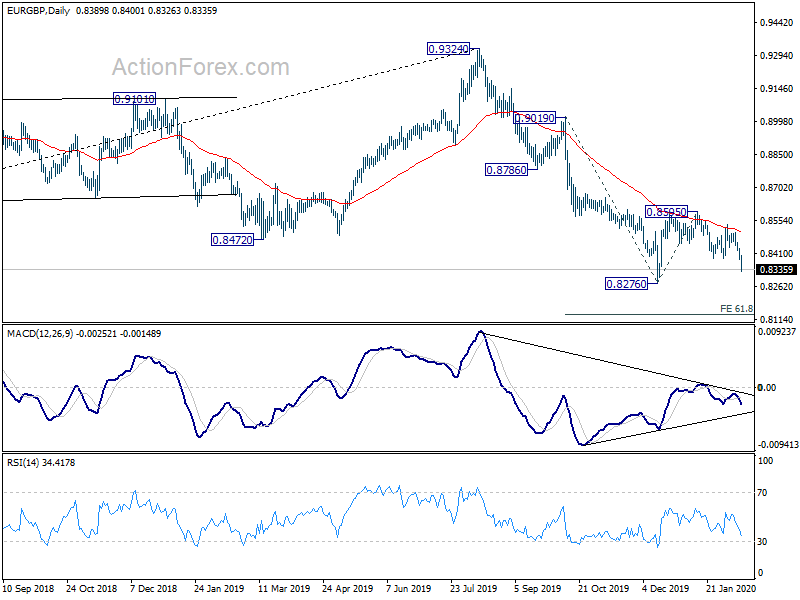

In the currency markets, Yen trading broadly higher today on risk aversion. But it’s outshone by Sterling, which was shot up by resignation of a key official of the UK cabinet. Euro is trading as the weakest one for now, followed by New Zealand and then Australian Dollar. Technically, EUR/GBP is on track to retest 0.8276 low and break will resume larger fall form 0.9324. EUR/JPY breaks 119.24 support and should be on tract to retest 115.86 low. USD/CHF’s break of 0.9788 resistance reaffirm near term bullishness for 0.9851 fibonacci level.

In Europe, currently, FTSE is down -1.55%. DAX is down -0.41%. CAC is down -0.72%. German 10-year yield is down -0.0073 at -0.384. Earlier in Asia, Nikkei dropped -0.14%. Hong Kong HSI dropped -0.34%. China Shanghai SSE dropped -0.71%. Singapore Strait Times dropped -0.10%. Japan 10-year JGB yield rose 0.0087 to -0.031.

US CPI accelerated to 2.5%, core CPI unchanged at 2.2%

US headline CPI accelerated to 2.5% yoy in January, up from 2.3% yoy, matched expectations. CPI core was unchanged at 2.3% yoy, beat expectation of 2.2% yoy.

Also released, initial jobless claims rose 2k to 205k in the week ending February 8, better than expectation of 210k. Four-week moving average of initial claims was unchanged at 212k. Continuing claims dropped -61k to 1.698m in the week ending February 1. Four-week moving average of continuing claims dropped -17.5k to 1.727m.

Sterling surges as Javid resigns as Chancellor of Exchequer

Sajid Javid surprisingly resigns as UK Chancellor of Exchequer today. He’s expected to be replaced by Rishi Sunak, the chief secretary to the Treasury. The Guardian said that Javid was asked by Prime Minister Boris Johnson to “fire all his special advisers and replace them with No 10 special advisers to make it one team”. Javid believed that “no self-respecting minister would accept those terms.”

Sterling responds positively to the news though. Instead of viewing it as some political uncertainty, markets see that Johnson is gaining more control over the cabinet, and thus creating more certainty for the country.

EU keeps Eurozone 2020, 2021 GDP forecast unchanged, raises inflation projection slightly

European Commission kept Eurozone GDP growth forecast unchanged at 1.2% in both 2020 and 2021. Eurozone inflation forecasts is raised by 0.1% in both 2020 and 201, to 1.3% and 1.4% respectively. For the EU as a whole, GDP forecast was also left unchanged at 1.4% in both 2020 and 2021. EU inflation forecast was also raised by 0.1% to 1.5% in 202, but 2021 projection remains unchanged at 1.6%.

Valdis Dombrovskis, Executive Vice-President, said, “Despite a challenging environment, the European economy remains on a steady path, with continued job creation and wage growth. But we should be mindful of potential risks on the horizon: a more volatile geopolitical landscape coupled with trade uncertainties.”

Paolo Gentiloni, European Commissioner for the Economy, said: “The outlook for Europe’s economy is for stable, albeit subdued growth over the coming two years. This will prolong the longest period of expansion since the launch of the euro in 1999, with corresponding good news on the jobs front… But we still face significant policy uncertainty, which casts a shadow over manufacturing. As for the coronavirus, it is too soon to evaluate the extent of its negative economic impact.”

ECB de Cos: Coronavirus keeps balance of risks to downside

ECB Governing Council member Pablo Hernandez de Cos said monetary policy will remain highly accommodative for a prolonged period of time.

But he also warned that “low-for-long interest rate environment could be encouraging excessive risk-taking by some financial intermediaries.” In particular, “asset valuations appear stretched in several advanced economies in markets such as equity, high-yield debt, and property markets.

Meanwhile, China’s Wuhan coronavirus “does keep balance of risks to downside.” Also, “Brexit entails significant risk of further fragmentation, as some companies may relocate to different financial centres.

RBA Lowe: Global interest rates to stay low for years, if not decades

RBA Governor Philip Lowe said today, “it is quite likely that we are going to be in this world of low interest rates for years, if not decades, because it is driven by structural factors.” For now, he added that RBA is not “obsessed” with getting inflation back to 2-3% target in a hurry.

Lowe repeated the central bank’s recent decision regarding balancing the risk of more monetary stimulus. “We’re conscious in our interest rate decisions that when we cut interest rates from cyclical perspectives it encourages people to borrow even more from an already high level of debt because of these structural reasons,” he said. “It’s a consideration in our decisions at the moment.”

Lowe also urged more from the government to help the economy. “We have not had any fiscal stimulus in Australia,” he said. “I would like to see both business and government use the opportunity to make investments. Australian governments and business can borrow at the lowest rates of since Australia became a federation.”

Hawkesby: RBNZ has genuine neutral bias, rates could stay low for a long time

RBNZ Assistant Governor Christian Hawkesby said in a Bloomberg interview that the central bank has a “genuine neutral bias” on rates, and “a genuine openness about where things go from here.” For now, “we can stay on hold, keep rates low for a long time”.

Regarding the impact of China’s coronavirus outbreak, disruptions to New Zealand economy could last just six weeks and save only 0.3% off Q1 growth. “If things are a lot worse, then the projections will look different and the policy response will look different,” he said. “At the moment the markets are probably more relaxed than they were earlier in the month. But equally we know that it’s asymmetric. If the median is six weeks it can’t be a whole lot shorter than that but it could be quite a lot longer.”

On the idea of rate hike, RBNZ is currently adopting a wait and see approached. He said, “When you’re in a period when there is no spare capacity left and we haven’t had inflation below target for a long time then you are in an environment where it’s safer to start lifting interest rates. We’re not close to that time. We’ve still got a long period when we can wait and watch.”

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8372; (P) 0.8401; (R1) 0.8421; More…

EUR/GBP’s break of 0.8386 support suggests resumption of fall from 0.8595. Intraday bias is back on the downside for 0.8276 low. Decisive break there will resume larger decline from 0.9324. Next downside target will be 61.8% projection of 0.9019 to 0.8276 from 0.8595 at 0.8136. On the upside, above 0.8400 minor resistance will turn bias neutral first.

In the bigger picture, decline from 0.9324 medium term top is still in progress. As long as 0.8786 support turned resistance holds, further fall is expected to 61.8% retracement of 0.6935 to 0.9324 at 0.7848. Nevertheless, break of 0.8786 will argue that fall from 0.9324 has completed and turn focus back to this high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jan | 1.70% | 1.50% | 0.90% | |

| 00:00 | AUD | Consumer Inflation Expectations Feb | 4.00% | 4.70% | ||

| 00:01 | GBP | RICS Housing Price Balance Jan | 17% | 3% | -2% | |

| 07:00 | EUR | Germany CPI M/M Jan F | -0.60% | -0.60% | -0.60% | |

| 07:00 | EUR | Germany CPI Y/Y Jan F | 1.70% | 1.70% | 1.70% | |

| 13:30 | USD | Initial Jobless Claims (Feb 7) | 205K | 210K | 202K | 203K |

| 13:30 | USD | CPI M/M Jan | 0.10% | 0.20% | 0.20% | |

| 13:30 | USD | CPI Y/Y Jan | 2.50% | 2.50% | 2.30% | |

| 13:30 | USD | CPI Core M/M Jan | 0.20% | 0.20% | 0.10% | |

| 13:30 | USD | CPI Core Y/Y Jan | 2.30% | 2.20% | 2.30% | |

| 15:30 | USD | Natural Gas Storage | -106B | -137B |