{kind=link}

Yen and Swiss are trading generally softer today as risk markets pick up some momentum again. On the other hand, Australian Dollar is leading other commodity currencies higher. Dollar is mixed for the moment, awaiting Fed Chair Jerome Powell’s testimony. Rally in stock markets could extend if Powell affirms that interest rate will stay low for low. Also, it should be noted that strength in corrective recovery in commodity currencies is so far weak, in particular against the greenback. We might see Dollar extends recent rally should Powell sounds upbeat on the economy

Technically, intraday bias in EUR/USD remains on the downside for 1.0879 low. Decisive break there will bring medium term down trend resumption. Further decline is also expected in AUD/USD as long as 0.6774 resistance holds. Sustained trading below 0.6670 low will confirm medium term down trend resumption too. Meanwhile, further rise is expected in USD/CAD as long as 1.3262 minor support holds. Sustained break of 1.3327 resistance will pave the way to 1.3664 high.

In Europe, currently, FTSE is up 0.82%. DAX is up 0.85%. CAC is up 0.41%. German 10-year yield is up 0.0181 at -0.391. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.39%. China Shanghai SSE rose 0.39%. Singapore Strait Times rose 0.39%.

WHO: China’s coronavirus a very grave threat for the world

World Health Organization director-general Tedros Adhanom Ghebreyesus warned that China’s coronavirus could pose a “very grave threat for the rest of the world”. He told more than researchers and national authorities at the start of a two-day meeting, “what matters most is stopping the outbreak and saving lives.”

Tedros also urged countries to share their data and emphasized “to defeat this outbreak, we need open and equitable sharing, according to the principles of fairness and equity.” However, at the same time, Taiwan, which has 18 confirmed cases, is also allowed to take part in as an observer.

EU to trigger an upward dynamic competition with UK

European Commission President Ursula von der Leyen told the European Parliament that she can agreement with UK Prime Minister Boris Johnson on setting high standards in the post Brexit relations. She said, “I’ve heard ambition in Boris Johnson’s speech, ambition on minimum wage, ambition on parental payments… I have heard ambition on cutting carbon emissions, ambition on guaranteeing that our firms are competing in full fairness.”

“This is what we also want. Let us formally agree on these objectives. We can formally trigger an upward dynamic competition that would benefit both the United Kingdom and the European Union,” she added.

UK GDP flat in Q4, poor production offset services and construction

UK GDP grew 0.3% mom in December, above expectation of 0.2% mom. For Q4, GDP growth was flat at 0.0% qoq, matched expectations. Services rose 0.1% in the quarter while construction grew 0.5%. But production contracted -0.8%, offsetting the contributions of the other two sectors.

Head of GDP Rob Kent-Smith: “There was no growth in the last quarter of 2019 as increases in the services and construction sectors were offset by another poor showing from manufacturing, particularly the motor industry. The underlying trade deficit widened, as exports of services fell, partially offset by a fall in goods imports.”

For December, industrial production rose 0.1% mom, dropped -1.8% yoy, versus expectation of 0.3% mom, -0.8% yoy. Manufacturing rose 0.3% mom, dropped -2.5% yoy, versus expectation of 0.5% mom, -3.7% yoy. Goods trade balance turned into GBP 0.85B surplus, better than expectation of GBP -10.0B deficit.

Australia NAB business confidence rose to -1, but decline in employment a concern

Australia NAB business confidence rose from -2 to -1 in January. Business conditions were unchanged at 3. Looking at some details, Trading conditions dropped from 6 to 5. Profitability conditions rose from 1 to 2. But employment conditions dropped sharply from 4 to 1.

Alan Oster, NAB Group Chief Economist warned: “The concern this month is the decline in employment. It is now below average and a worry given the labour market has been a bright spot in the economic data. That said, there is a risk that ongoing weakness in business activity sees a pull-back in hiring intentions”.

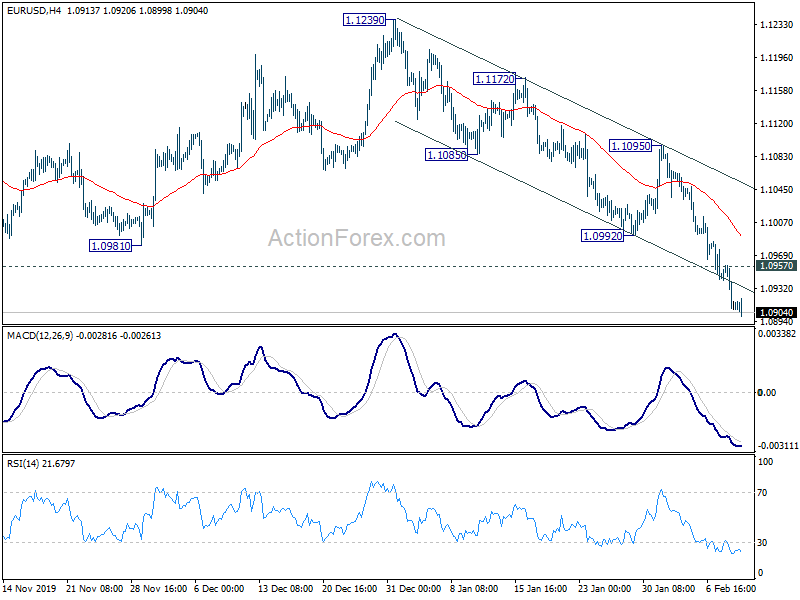

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0893; (P) 1.0926; (R1) 1.0943; More…

EUR/USD’s decline from 1.1239 is still in progress and intraday bias stays on the downside for 1.0879 low. Firm break there will resume larger down trend for 1.0813 fibonacci level next. On the upside, above 1.0957 minor resistance will turn intraday bias neutral first. But recovery should be limited by 1.0992 support turned resistance to bring fall resumption.

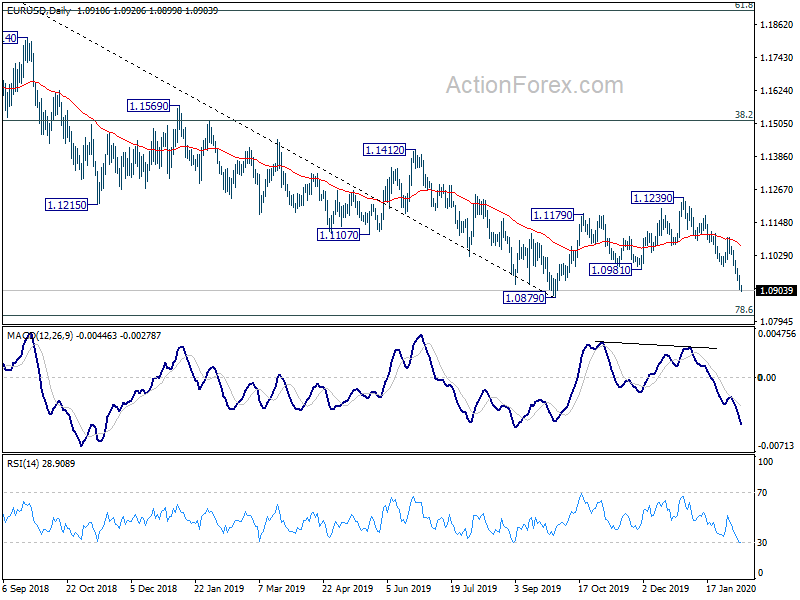

In the bigger picture, rebound from 1.0879 is seen as a corrective that might have completed after rejection by 55 week EMA. Break of 1.0879 will resume the down trend from 1.2555 (2018 high) for 78.6% retracement of 1.0339 (2017 low) to 1.2555 at 1.0813. Sustained break there will pave the way to retest 1.0339 low. For now, this will remain the favored case as long as 1.1239 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Jan | 0.00% | 0.60% | 1.70% | |

| 0:30 | AUD | NAB Business Confidence Jan | -1 | -2 | ||

| 0:30 | AUD | NAB Business Conditions Jan | 3 | 3 | ||

| 9:30 | GBP | GDP M/M Dec | 0.30% | 0.20% | -0.30% | |

| 9:30 | GBP | GDP Q/Q Q4 P | 0.00% | 0.00% | 0.40% | |

| 9:30 | GBP | Industrial Production M/M Dec | 0.10% | 0.30% | -1.20% | -1.10% |

| 9:30 | GBP | Industrial Production Y/Y Dec | -1.80% | -0.80% | -1.60% | -2.50% |

| 9:30 | GBP | Manufacturing Production M/M Dec | 0.30% | 0.50% | -1.70% | -1.60% |

| 9:30 | GBP | Manufacturing Production Y/Y Dec | -2.50% | -3.70% | -2.00% | -3.30% |

| 9:30 | GBP | Index of Services 3M/3M Dec | 0.10% | 0.00% | 0.10% | 0.00% |

| 9:30 | GBP | Goods Trade Balance (GBP) Dec | 0.85B | -10.0B | -5.3B | |

| 13:00 | GBP | NIESR GDP Estimate (3M) Jan | 0.20% | 0.00% |