{kind=link}

While risk sentiments stabilize today, there is no clear momentum of any meaningful recovery in global stock markets. Investors remain on guard against new developments of China’s coronavirus outbreak, which confirmed cases exceed 2003’s SARS already. Yen and Dollar trading generally firmer today, as in early US session. Though, Swiss Franc is pressured together with Aussie and Kiwi.

In Europe, currently, FTSE is up 0.17%. DAX is up 0.17%. CAC is up 0.44%. German 10-year yield is down -0.037 at -0.376. Earlier in Asia, Nikkei rose 0.71%. Hong Kong HSI dropped -2.82% in post-holiday catch up. Singapore Strait Times rose 0.04%. Japan 10-year JGB yield rose 0.0003 to -0.037.

Focus will turn to FOMC rate decisions. Markets are pricing in no chance of a cut today and Fed would in no way spoil such expectations. Fed Chair Jerome Powell would reiterate that monetary policy is at the right place. The committee will need more time to gauge the impacts of last year’s three rate cuts, as well as impact of US-China trade deal phase one etc. Overall, the announcement and press conference will likely be a non-event.

Here are some previews on FOMC:

- Fed To Stay On Hold, But Adopt A More Cautious Tone?

- FOMC Preview: Will Powell Open The Door To A Summer Rate Cut?

- FOMC to Stay Put this Week

- January Flashlight for FOMC Blackout Period

US goods trade deficit widened to $68.3B

US goods trade deficit widened 8.5% mom to USD -68.3B in December, larger than expectation of USD -64.5B. Goods exports rose USD 0.4B to USD 137.0B. Goods imports rose USD 5.8B to USD 205.3B.

Wholesale inventories dropped -0.1% mom to USD 675.6B. Retail inventories was flat at USD 661.2B.

China’s GDP growth could slow to 5% or below in Q1 due to coronavirus outbreak

Zhang Ming, an economist at the Chinese Academy of Social Sciences, said China’s annualized growth could slow to 5.0% in Q1 this year, or even lower, due to coronavirus outbreak. That’s sharply lower than original estimate of 6.0% annualized growth. While there could be recovery afterwards, full-year expansion could flow from 2019’s 6.1% to just 5.7%.

He estimated that the impact of the current coronavirus would be significantly higher than that of SARS back in 2003. Now, China’s economy is much more reliant on services and consumption. The outbreak has also hit sectors including transportation, tourism, catering and entertainment. It could also weigh on the employment market as unemployment rate could exceed 5.3% in the coming months.

In response, Zhang expected the government to step up policy support while PBoC could lower the reserve requirement ratios for banks and interest rates.

Germany Maas: Without meeting EU standard UK will not have full access to the single market

German Foreign Minister Heiko Maas said in a Die Zeit article that “we all want zero tariffs and zero trade barriers” between EU and UK. However, “that also means zero dumping and zero unfair competition.”

He emphasized, “Without similar standards to protect our workers, our consumers and the environment, there can be no full access to the largest single market in the world.”

Mass also urged that EU and UK must conduct the negotiations regarding post-Brexit relationship in a way that “won’t harm the European Union”.

German Gfk consumer sentiment rose to 9.9, economic expectations improved

Germany Gfk Consumer Sentiment for February rose to 9.9, up from 9.7, beat expectation of 9.8. Economic Expectations also rose from -4.4 to -3.7.

Rolf Bürkl, GfK consumer expert: “Initial agreements in the trade dispute between the United States and China will also ease the situation in Germany. As an export nation, the country relies on the free and unrestricted exchange of goods.”

“The positive start for the consumer climate in 2020 confirms our assessment that private consumption will continue to be an important pillar of the German economy this year. For the year as a whole, GfK forecasts real growth in private consumer spending in Germany of one percent.”

Also released, Eurozone M3 money supply rose 5.0% yoy in December, below expectatoin of 5.5% yoy. Swiss ZEW economic expectations dropped to 8.3 in January, down from 12.5.

BoJ: Only halfway out of Japanification, downside risks still significant

In the Summary of Opinions of BoJ’s January 20/21 meeting, it’s noted that there has been “no further increase in the possibility that the momentum toward achieving the price stability target will be lost.”. Therefore, it’s “appropriate” to keep monetary policy unchanged. Nevertheless, the possibility of inflation losing momentum continues to “warrant attention”. It’s “appropriate” to tilt toward monetary accommodation.

Also, Japan is just “only halfway toward moving out of the so-called Japanification” of secular stagnation where low growth, low inflation, and low interest rates last for a long period. Risk of deflation continues to “warrant attention”. Downside risks to economic activity and prices are “still significant”. It’s necessary to be prepared for possible economic downturn as one of the risk scenarios.

Also released, Japan consumer confidence was unchanged at 39.1 in January, missed expectation of 40.8.

Australia CPI rose 0.7% qoq, 1.8% yoy, drought pushed food prices higher

Australia CPI rose 0.7% qoq, 1.8% yoy in Q4, up from 0.5% qoq, 1.7% yoy, beat expectation of 0.6% qoq, 1.7% yoy. RBA trimmed mean CPI rose 0.4% qoq, 1.6% yoy, unchanged from prior quarter. RBA weighted median CPI rose 0.4% qoq, 1.3% yoy, also unchanged from Q3. The set of data affirmed the chance for RBA to stand pat in February, and delay the widely expected rate cut.

ABS Chief Economist, Bruce Hockman said: “Drought conditions are impacting prices for a range of food products. Food prices increased 1.3 per cent this quarter with price rises for beef and veal (+2.9 per cent), pork (+4.7 per cent), milk (+1.7 per cent) and cheese (+2.4 per cent). Both the impact from the drought and lower seasonal supply contributed to price rises for fruit (+6.8 per cent) this quarter.”

“Annual inflation remains subdued partly due to some price falls for housing related expenses. Through the year to the December 2019 quarter, price falls were recorded for utilities (-1.0 per cent) and new dwelling purchase by owner-occupiers (-0.1 per cent), while rent price rises remained modest (+0.2 per cent),” said Hockman.

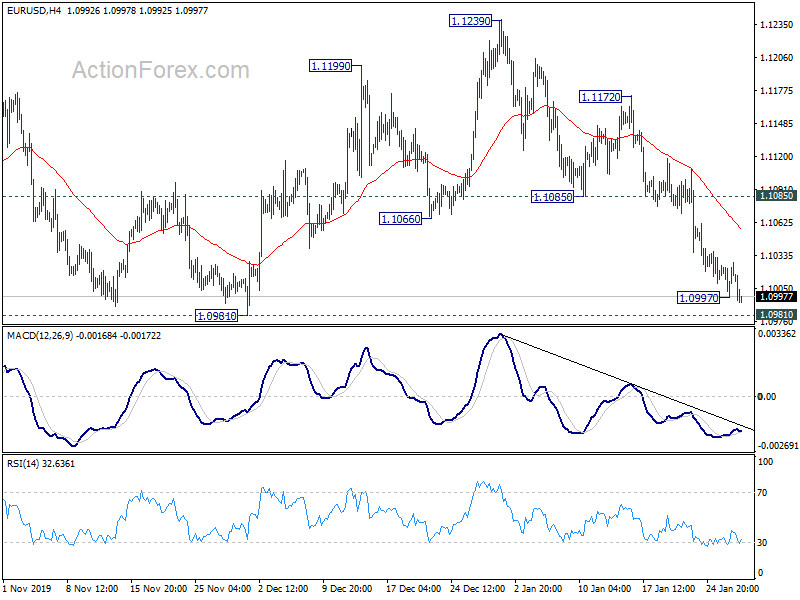

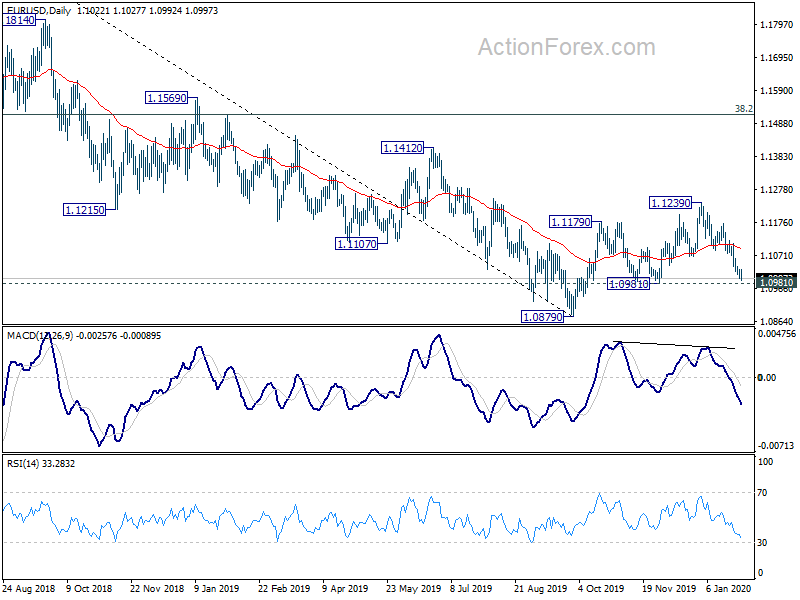

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1005; (P) 1.1015; (R1) 1.1032; More…

EUR/USD’s decline resumes after brief consolidation and intraday bias back on the downside for 1.0981 support. Decisive break there should confirm completion of corrective rise from 1.0879 at 1.1239. Further fall should then be seen to retest 1.0879 low. In any case, near term outlook will stay bearish as long as 1.1085 support turned resistance holds, in case of recovery.

In the bigger picture, rebound from 1.0879 is seen as a corrective move at this point. In case of another rise, upside should be limited by 38.2% retracement of 1.2555 to 1.0879 at 1.1519. And, down trend from 1.2555 (2018 high) would resume at a later stage. However, sustained break of 1.1519 will dampen this bearish view and bring stronger rise to 61.8% retracement at 1.1915 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Dec | 0.10% | -0.10% | 0.00% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 00:01 | GBP | BRC Shop Price Index Y/Y Dec | -0.30% | -0.40% | ||

| 00:30 | AUD | CPI Q/Q Q4 | 0.70% | 0.60% | 0.50% | |

| 00:30 | AUD | CPI Y/Y Q4 | 1.80% | 1.70% | 1.70% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q4 | 0.40% | 0.40% | 0.40% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q4 | 1.60% | 1.50% | 1.60% | |

| 05:00 | JPY | Consumer Confidence Index Jan | 39.1 | 40.8 | 39.1 | |

| 07:00 | EUR | Germany Gfk Consumer Confidence Feb | 9.9 | 9.8 | 9.6 | 9.7 |

| 09:00 | CHF | ZEW Survey Expectations Jan | 8.3 | 12.5 | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Dec | 5.00% | 5.50% | 5.60% | |

| 13:30 | USD | Wholesale Inventories Dec P | -0.10% | 0.10% | -0.10% | |

| 13:30 | USD | Goods Trade Balance (USD) Dec | -68.3B | -64.5B | -63.2B | -63.0B |

| 15:00 | USD | Pending Home Sales M/M Dec | 0.30% | 1.20% | ||

| 15:30 | USD | Crude Oil Inventories | 0.7M | -0.4M | ||

| 19:00 | USD | FOMC Rate Decision | 1.75% | 1.75% | ||

| 19:30 | USD | FOMC Press Conference |