{kind=link}

Australian Dollar rises broadly today as markets pare back bet on RBA rate cut in February, following better than expected job data. Though, upside is limited by risk aversion while Aussie is just following Yen as the second strongest. Asian stocks trade generally, deeply lower, after China halted travel from Wuhan city, the center of outbreak of the new coronavirus. Canadian Dollar is currently the weakest one. Selloff in the Loonie started overnight after dovish BoC, and extends on free fall in oil prices.

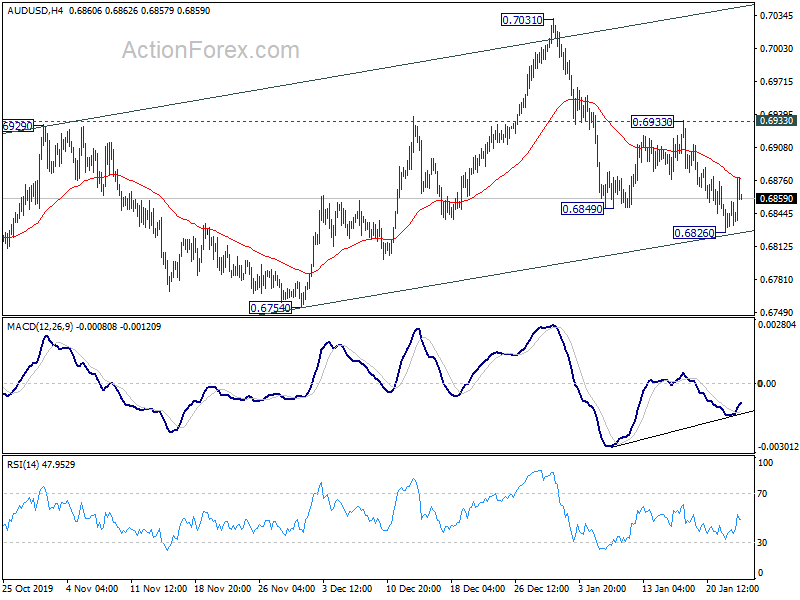

Technically, USD/JPY’s break of 109.76 support should now confirm short term topping at 110.28. Deeper pull back should be seen to 55 day EMA (now at 109.14) and below. AUD/USD formed a temporary low at 0.6826 after drawing support from near term channel. But further decline is still expected as long as 0.6933 resistance holds. USD/CAD is moving away from 55 day EMA and should be targeting 1.3327 resistance. We’re favoring the case that medium term correction from 1.3664 (2018 high) has completed as a triangle at 1.2951. Break of 1.3327 should confirm our view.

In Asia, Nikkei close down -0.98%. Hong Kong HSI is down -2.04%. China Shanghai SSE is down -2.74%. Singapore Strait Times is down -0.62%. Japan 10-year JGB yield is down -0.0153 at -0.018. Overnight, DOW dropped -0.03%. S&P 500 rose 0.03%. NASDAQ rose 0.14%. 10-year yield was flat at 1.769.

Markets pare RBA cut expectation after strong job data

Australia employment grew 28.9k to 12.98m in December, much better than expectation of 14.0k. Full-time jobs dropped slightly by -0.3k to 8.83m. Part-time jobs rose 29.2k to 4.15m. Unemployment rate dropped -0.1% to 5.1%, better than expectation of 5.2%. Participation rate remained steady at 66.0%.

ABS Chief Economist Bruce Hockman said: “Trend unemployment rate decreased slightly to 5.1 per cent, its lowest level since April 2019. While there has been stronger growth in part-time employment over the past year, the underemployment rate is still where it was last December, at 8.3 per cent.”

Australian Dollar recovers as markets push back expectation of February RBA rate cut, due to the upside surprises in job data. ANZ said the data reinforce RBA’s view that the economy appears to have reached a “gentle turning point”. it will be difficult to see RBA easing in February even though rate cuts are more likely than not over the course of 2020. CBA said RBA would now likely cut by 25bps to 0.50% in April, instead of February.

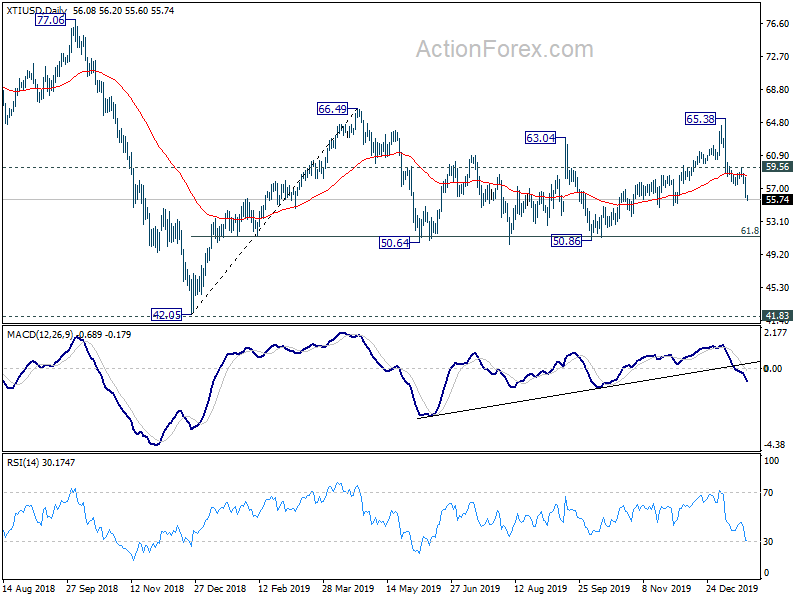

WTI oil dives as IEA forecasts 1m bpd surplus in first half 2020

Oil price dropped sharply overnight after International Energy Agency (IEA) Executive Director Fatih Birol said there would be a surplus of as mush as 1m bpd of oil in the first half of the year. He said, there is an “abundance of energy supply” in oil and gas. And it’s the “reason that recent incidents we have seen – with the Iranian general killed, Libya unrest – didn’t boost international oil prices.”

WTI’s fall from 65.38 resumed by taking out 57.35 support and hits as low as 55.60 so far. Such decline is seen as a leg inside the sideway pattern from 66.49. With 55 day EMA firmly taken out not, further fall should be seen to retest 50.84 key support level. Strong support should be seen from there to bring rebound. For now, break of 59.56 resistance is needed to indicate completion of the decline. Otherwise, near term outlook stays bearish in case of recovery.

ECB to stand pat, reveal details of strategic review

ECB rate decision and press conference is the major focus for today. No change in monetary policy is expected. That is, main refinancing rate will be held at 0.00%. Deposit rate should be kept at -0.50% too. Pace of asset purchase program should also be unchanged at EUR 20B per month.

Forward guidance should also be unchanged as “the Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.”

President Christine Lagarde might acknowledge in the press conference that recent data have shown some stabilization. But momentum of recovery, in particular in the manufacturing sector, has been weak. The board will remain cautious and risk to growth and price remain tilted to the downside.

Most attention will likely be on the details of the strategic review to be announced at the meeting. While this would be lengthy exercise, we expect the market to be particularly interested in the revision of inflation target. There have been talks that the current inflation target as “below but close to 2%” can be revised in favor of a symmetric target.

Here are some suggested previews on ECB:

- ECB to Leave Monetary Policy Unchanged, Focus Turns to Strategic Review

- No Fireworks at ECB Meeting, but PMIs Could Drive Euro

- ECB Preview: Time to Reveal the Scope

On the data front

Japan trade deficit widened slightly to JPY -0.10T in December, better than expectation of JPY -0.24T. All industry activity index rose 0.9% mom in November, above expectation of 0.40%. Eurozone consumer confidence and US jobless claims will be featured later in the day.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6829; (P) 0.6842; (R1) 0.6858; More…

A temporary low is formed at 0.6829 as AUD/USD recovered after drawing support from near term channel. Intraday bias is turned neutral first. Upside of recovery should be limited below 0.6933 resistance to bring fall resumption. We maintain the view that corrective rise from 0.6670 has completed at 0.7031. Below 0.6826 will turn bias to the downside for 0.6754 support to confirm this bearish case. However, break of 0.6933 will turn focus back to 0.7031 instead.

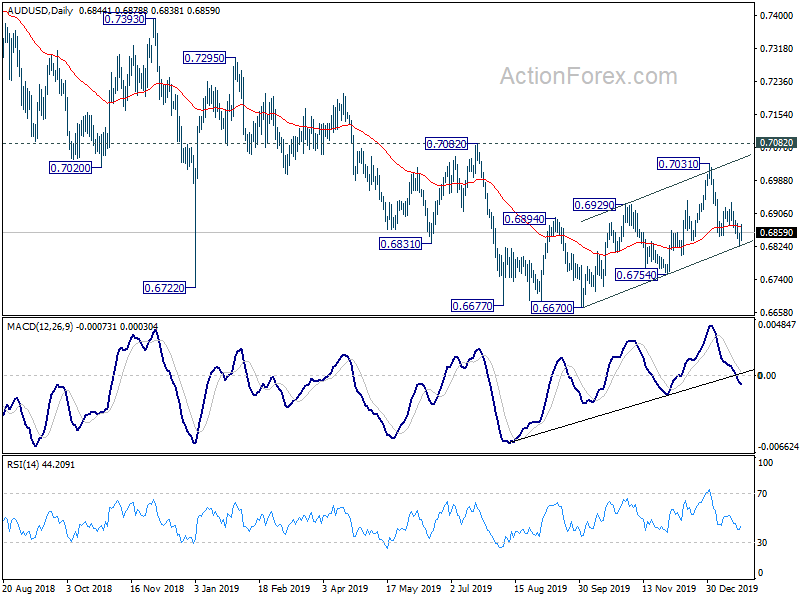

\\In the bigger picture, with 0.7082 resistance intact, there is no clear confirmation of trend reversal yet. That is, down trend from 0.8135 (2018 high) is still expect to continue to 0.6008 (2008 low). However, decisive break of 0.7082 will confirm medium term bottoming and bring stronger rally back to 55 month EMA (now at 0.7484).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Dec | -0.10T | -0.24T | -0.06T | -0.09T |

| 0:00 | AUD | Consumer Inflation Expectations Jan | 4.70% | 4.00% | ||

| 0:30 | AUD | Employment Change Dec | 28.9K | 14.0K | 39.9K | 38.5K |

| 0:30 | AUD | Unemployment Rate Dec | 5.10% | 5.20% | 5.20% | |

| 4:30 | JPY | All Industry Activity Index M/M Nov | 0.90% | 0.40% | -4.30% | -4.80% |

| 12:45 | EUR | ECB Interest Rate Decision | 0.00% | 0.00% | ||

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | USD | Initial Jobless Claims (Jan 17) | 214K | 204K | ||

| 15:00 | EUR | Consumer Confidence Jan P | -8 | -8 | ||

| 15:30 | USD | Natural Gas Storage | -109B | |||

| 16:00 | USD | Crude Oil Inventories | -2.5M |