{kind=link}

Dollar’s selloff continues today and is accelerating. Solid risk appetite isn’t a friend of the greenback this time, nor the Yen which is the second weakest. Sterling is staging a strong rebound as it seems that recent pull back has completed. Commodity currencies are indeed mixed despite persistent strength in oil prices and gold. As for the week, Yen is the weakest one, followed by Dollar. Kiwi is the strongest, followed by Aussie, but the Pound has the potential to over take them.

Technically, GBP/USD’s break of 1.3079 resistance and GBP/JPY’s break of 141.15 resistance suggest that corrective pull back has completed. Further rise is in favor back to 1.3514 and 147.95 respectively. 0.8476 minor support in EUR/GBP will now be watched to confirm broad based come back in Sterling. USD/CHF’s break of 0.9770 indicates resumption of fall from 1.0023 towards 0.9659 support. USD/CAD’s break of 1.3102 also resumes the fall from 1.3327 to 1.3042 key support level.

In Europe, currently, FTSE is up 0.32%. DAX is up 0.55%. CAC is up 0.43%. German 10-year yield is down -0.0028 at -0.241. Earlier in Asia, Nikkei dropped -0.36%. Hong Kong HSI rose 1.30%. China Shanghai SSE dropped -0.08%. Singapore Strait Times rose 0.11%. Japan 10-year JGB yield closed up 0.0021 to -0.011.

ECB: Global recovery projected to be shallow

ECB said in its monthly economic bulletin that more recent information “points to a stabilisation in global growth”. In particular, survey-based data like PMI point to a “moderate recovery in manufacturing output growth and some moderation in services output growth”. Nevertheless, global recovery is projected to be “shallow”, reflecting moderation of growth in advanced economies and sluggishness in some emerging markets.

For Eurozone, however, ongoing weakness of international trade continues to weigh on manufacturing sector and is dampening investment growth. Survey-based data, while remaining weak overall, point to some stabilization of slowdown too.

Measures of underlying inflation in Eurozone “generally remained muted”. ECB added, that “market-based indicators of longer-term inflation expectations have remained at very low levels, while survey-based expectations also stand at historical lows.

BoJ: May need to expand QQE after consumption tax hike, just like 2014

In the Summary of Opinions at BoJ’s December 18-19 meeting, it’s noted there has been “no further increase” in the possibility that momentum toward achieving price target will be lost. Therefore, maintaining the current guidelines for market operations and asset purchases is “appropriate”.

Nevertheless, downside risks to economic activity and prices “continue to warrant attention”, mainly regarding overseas developments. And it’s appropriate to maintain a stance of being “tilted toward monetary accommodation”. With risks “skewed to the downside” BoJ should continue to examine “whether additional monetary easing will be necessary”.

In particular, it’s noted that BoJ expanded QQE around half a year after the previous consumption tax hike in 2014. “It may become necessary to conduct further monetary easing this time as well”.

Japan industrial production and retail sales contracted

Economic data released from Japan showed strain in both the business and consumer sides of the economy. Industrial production dropped for the second month in a row, by -0.9% mom in November. Though, that came in better than expectation of -1.4% mom. Back in October, production dropped -4.5% mom, largest month-on-month decline since 2013. Both months’ data pointed to sharp contraction in factory output in Q4.

Meanwhile, retail sales dropped -2.1% yoy in November too, worse than expectation of -1.7% yoy. Back in October, sales dropped sharply by -7.1% as sales tax hike took effect, worst since 2015. Sales had clearly not recovered yet and is poised to have a weak quarter too.

Though, on the positive side, unemployment rate dropped to 2.2% in November, down from 2.4%, beat expectation of 2.4%. Tokyo CPI accelerated to 0.8% yoy in December, up from 0.6% yoy, beat expectation of 0.6% yoy.

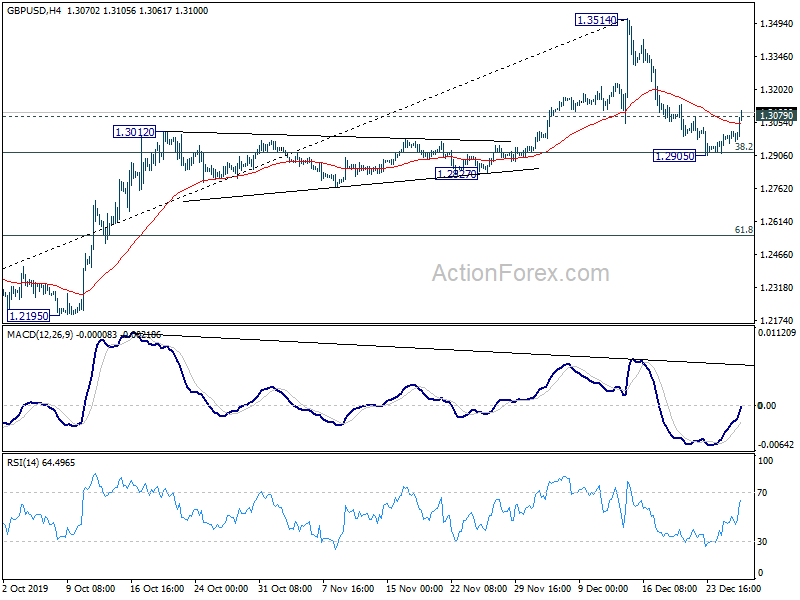

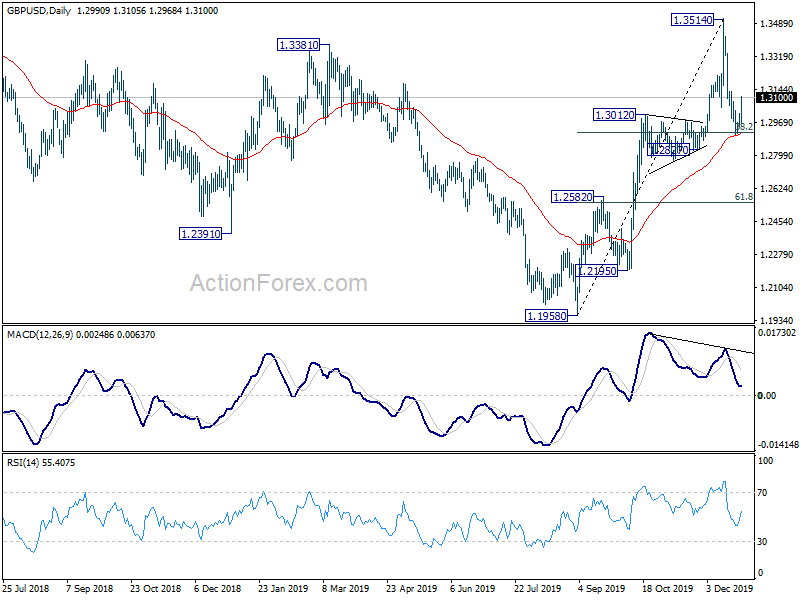

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2960; (P) 1.2988; (R1) 1.3024; More….

GBP/USD’s break of 1.3079 minor resistance suggests that corrective fall form 1.3514 has completed at 1.2905, after drawing support from 38.2% retracement of 1.1958 to 1.3514 at 1.2920. Intraday bias is turned back to the upside for retesting 1.3514 high. On the downside, sustained trading below 1.2920 will pave the way to 61.8% retracement at 1.2552.

In the bigger picture, rise from 1.1958 medium term bottom expected to extend higher to retest 1.4376 key resistance. Reactions from there would decide whether it’s in consolidation from 1.1946 (2016 low). Or, firm break of 1.4376 will indicate long term bullish reversal. In any case, for now, outlook will stay bullish as long as 1.2582 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Dec | 0.80% | 0.60% | 0.60% | |

| 23:30 | JPY | Unemployment Rate Nov | 2.20% | 2.40% | 2.40% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Nov P | -0.90% | -1.40% | -4.50% | |

| 23:50 | JPY | Retail Trade Y/Y Nov | -2.10% | -1.70% | -7.00% | |

| 09:00 | CHF | ZEW Survey – Expectations Dec | 12.5 | -8.5 | -3.9 | |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 15:30 | USD | Natural Gas Storage | -145B | -107B | ||

| 16:00 | USD | Crude Oil Inventories | -1.7M | -1.1M |