{kind=link}

Global stock markets are generally under pressure today. There is some lift from a WSJ report that US and China are laying the ground work for a delay in December 15 tranche of tariffs But the recovery in sentiment is so far limited. In the currency markets, Australian and New Zealand Dollars are so far the weakest one, together with Japanese Yen. Sterling and Swiss Franc are the strongest one. Overall picture could have a big change if more news regarding US-China trade negotiations surface.

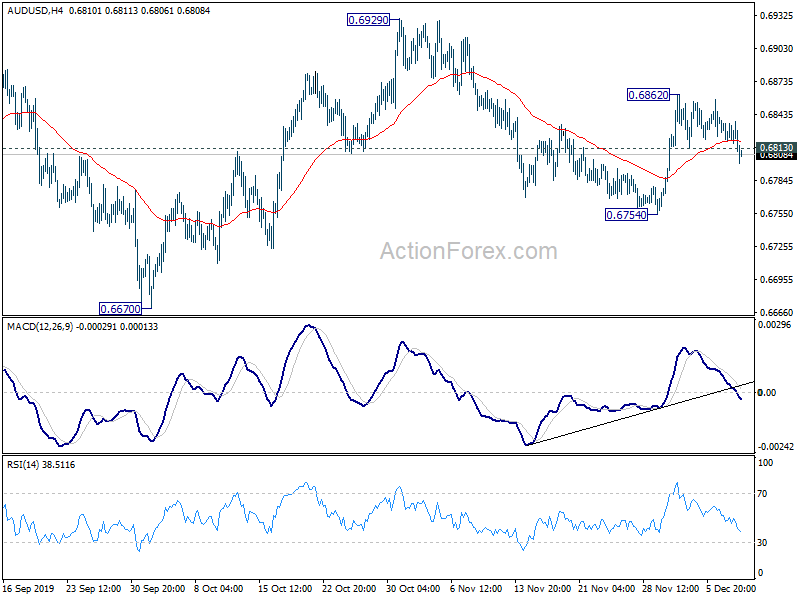

Technically, AUD/USD’s break of 0.6813 minor support argues that rebound from 0.6754 has completed at 0.6862. Deeper fall is now in favor to retest 0.6754 support first. The development put EUR/AUD’s focus back to 1.6323 resistance. Break there will resume the rebound from 1.5976. That would also add to sign of Aussie weakness. EUR/CHF’s fall from 1.0921 suggests resumption of fall from 1.1027 to 1.0863 support. USD/CHF is now pressing 0.9855 temporary low. Break will put 0.9841 key near term support in focus.

In Europe, FTSE is down -0.53%. DAX is down -0.63%. CAC is down -0.13%. Germany 10-year yield is up 0.005 at -0.300. Earlier in Asia, Nikkei dropped -0.09%. Hong Kong HSI dropped -0.22%. China Shanghai SSE rose 0.10%. Singapore Strait Times dropped -0.53%. Japan 10-year JGB yield dropped -0.0159 to -0.021.

US Ross: USMCA within millimeters of completion

US Commerce Secretary Wilbur Ross told Fox Business that the US, Mexico and Canada are “within inches, maybe millimeters” of completing the USMCA. The trilateral trade agreement is expected to create “north of 176,000 new jobs” and boost the auto industry by USD 34B.

Trade officials of the three countries are expected to meet in Mexico City today to pin down the details. A vote in the House would be needed this week to ensure passage of USMCA by year end. “Every day that it isn’t approved is a day delayed and the benefits to America,” Ross said.

Released from US, non-farm productivity dropped -0.2% in Q3. Unit labor costs rose 2.5%.

UK GDP shows no growth in October, dragged by manufacturing and construction

UK GDP grew 0.0% mom in October, below expectation of 0.1% mom. Rolling three-month GDP also showed no growth. An ONS Spokesperson said: “The UK economy saw no growth in the latest three months. There were increases across the services sector, offset by falls in manufacturing with factories continuing the weak performance seen since April. Construction also declined across the last three months with a notable drop in house building and infrastructure in October.”

Looking at some details, Index of Services rose 0.2% 3mo3m, below expectation of 0.5% 3mo3m. Services contributed 0.17% to the three month GDP growth Index of Production dropped -0.7% 3mo3m, contributed -0.1% to GDP. Construction dropped -0.3%, contributed -0.02% to GDP.

Also from UK, industrial production came in at 0.1% mom, -1.3% yoy in October, below expectation of 0.2% mom, -1.2% yoy. Manufacturing production was at 0.2% mom, -1.2% yoy, above expectation of 0.0% mom, -1.5% yoy. Goods trade deficit widened to GBP -14.5B, versus expectation of GBP -11.5B.

NIESR: UK GDP on track to grow 0.1% in Q4, 1.3% in 2019

NEISR said UK economy is on course to growth by 0.1% in Q4. And that would be consistent with growth of 1.3% in 2019, just down slightly from 1.4% in 2018.

Garry Young Director of Macroeconomic Modelling and Forecasting, said, “The latest data confirm that economic growth in the United Kingdom is petering out at the end of the year. GDP was flat in the three months to October, and the latest surveys point to further stagnation in November and December. The economy is being held back by weak productivity growth and low investment due to chronic levels of uncertainty. While some uncertainty could be resolved by the outcome of the general election, it is doubtful that this will provide businesses with the clarity needed to invest with confidence.”

German ZEW jumped to 10.7, but economy still fragile

German ZEW Economic Sentiment rose to 10.7 in December, up from -2.1, beat expectation of 1.1. It’s also the highest value since February 2018. Current Situation Index also rose to -19.9, up from -24.7, beat expectation of -22.0. Eurozone ZEW Economic Sentiment rose to 11.2, up from -1, beat expectation of 2.2. Current Situation Index rose 4.9 pts -14.7.

ZEW President Achim Wambach: “At first glance, the renewed substantial increase of the ZEW Indicator of Economic Sentiment may seem surprising. It rests on the hope that German exports and private consumption will develop better than previously thought. This hope results from a higher than expected German foreign trade surplus in October, alongside relatively robust economic growth in the EU in the third quarter and a stable German labour market. The rather unfavourable figures for industrial production and incoming orders for October, however, show that the economy is still quite fragile.”

Australia business conditions stabilized at low levels, ongoing GDP weakness continues

Australia NAB Business Confidence dropped to 0 in November, down from 2. Business Conditions was unchanged at 4. Looking at some details, Trading Conditions dropped from 7 to 6. Profitability Conditions rose from 0 to 3. Employment Conditions was unchanged at 4.

NAB said business conditions “appear to have stabilised at low levels, after declining significantly between mid-2018 and 2019”. But “the divergence between the goods related industries (the weakest) and the services sector (the strongest) widened.” The business survey is consistent with “ongoing weakness in GDP growth” with little improvement in Q4, risking slower employment growth.

Also from Australia, residential property prices 2.4% qoq in Q3, well above 0.5% qoq. That’s also the strongest quarterly growth since December quarter 2016. ABS Chief Economist Bruce Hockman said, “The increase in property prices is in line with housing market indicators, particularly in Sydney and Melbourne. New lending commitments to households, auction clearance rates and sales transactions all improved during the September quarter.”

China CPI jumped to 4.5% on fresh vegetable and pork

Headline CPI in China accelerated to +4.5% y/y in November, from +3.8% a month ago. The key contributor to strong inflation is fresh vegetable and pork prices. We expect headline CPI to stay strong in coming months. Although pork price has shown signs of moderation, fresh vegetables price has picked up again. Inflation, way above PBOC’s target of 3%, has limited the scope of the central bank to ease the monetary policy.

More in China’s CPI Soared to +4.5%; Exports Contracted More than Expected.

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6817; (P) 0.6829; (R1) 0.6838; More…

AUD/USD’s break of 0.6813 minor support suggests that rebound from 0.6754 has completed at 0.6862. Intraday bias is turned back to the downside for 0.6754 first. Break will resume the decline form 0.6929 to retest 0.6670 low. On the upside, above 0.6862 will turn bias back to the upside for 0.6929 resistance instead.

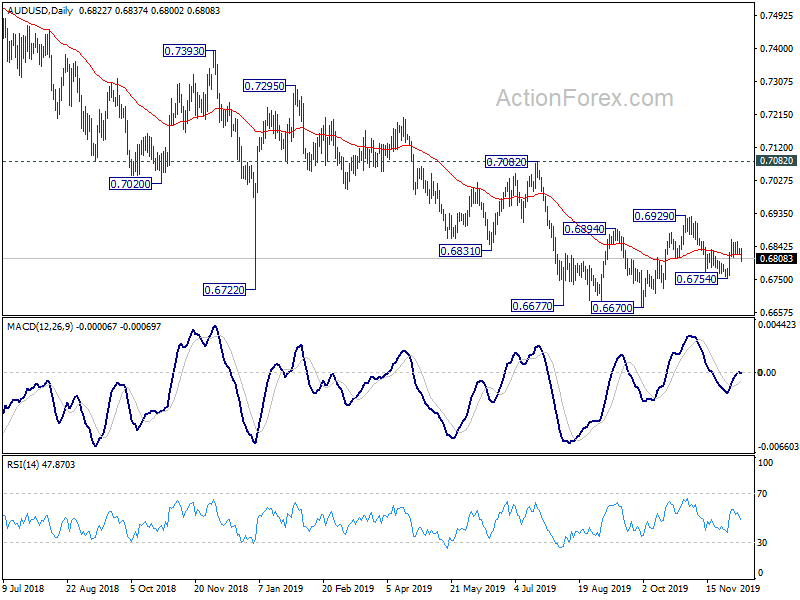

In the bigger picture, with 0.7082 resistance intact, there is no clear confirmation of trend reversal yet. That is, down trend from 0.8135 (2018 high) is still expect to continue to 0.6008 (2008 low). However, decisive break of 0.7082 will confirm medium term bottoming and bring stronger rally back to 55 month EMA (now at 0.7525).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | 2.80% | 2.50% | 2.50% | 2.40% |

| 00:30 | AUD | House Price Index Q/Q Q3 | 2.40% | 0.50% | -0.70% | |

| 00:30 | AUD | NAB Business Confidence Nov | 0 | 2 | ||

| 00:30 | AUD | NAB Business Conditions Nov | 4 | 3 | ||

| 01:30 | CNY | CPI Y/Y Nov | 4.50% | 4.50% | 3.80% | |

| 01:30 | CNY | PPI Y/Y Nov | -1.40% | -1.50% | -1.60% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | -37.90% | -37.40% | ||

| 07:45 | EUR | France Industrial Output M/M Oct | 0.40% | 0.20% | 0.30% | |

| 09:00 | EUR | Italy Industrial Output M/M Oct | -0.30% | -0.40% | ||

| 09:30 | GBP | GDP M/M Oct | 0.00% | 0.10% | -0.10% | |

| 09:30 | GBP | Index of Services 3M/3M Oct | 0.20% | 0.50% | 0.40% | |

| 09:30 | GBP | Industrial Production M/M Oct | 0.10% | 0.20% | -0.30% | |

| 09:30 | GBP | Industrial Production Y/Y Oct | -1.30% | -1.20% | -1.40% | |

| 09:30 | GBP | Manufacturing Production M/M Oct | 0.20% | 0.00% | -0.40% | |

| 09:30 | GBP | Manufacturing Production Y/Y Oct | -1.20% | -1.50% | -1.80% | |

| 09:30 | GBP | Goods Trade Balance (GBP) Oct | -14.5B | -11.5B | -12.5B | -11.5B |

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | 10.7 | 1.1 | -2.1 | |

| 10:00 | EUR | Germany ZEW Current Situation Dec | -19.9 | -22 | -24.7 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 11.2 | 2.2 | -1 | |

| 11:00 | USD | NFIB Business Optimism Index Nov | 104.7 | 102.8 | 102.4 | |

| 12:20 | GBP | NIESR GDP Estimate Nov | 0.00% | 0.10% | 0.00% | |

| 13:30 | USD | Nonfarm Productivity Q3 | -0.20% | -0.20% | -0.30% | |

| 13:30 | USD | Unit Labor Costs Q3 | 2.50% | 3.50% | 3.60% |