{kind=link}

Australian Dollar remains the strongest one for today as boosted by optimism over US-China trade deal. But the markets are relatively mixed elsewhere. Yen couldn’t decide what to do as risk appetite fades in European session, while US stocks also open mildly lower. European majors are generally soft on news regarding UK snap elections. Dollar is mildly firmer, and outshines Canadian. But the fates of USD/CAD won’t be decided before tomorrow’s BoC and FOMC rate decisions.

From US, S&P Case-Shiller 20 cities house price rose 2.0% yoy in August. Also released, UK M4 money supply rose 0.7% mom in September versus expectation of 0.3% mom. Mortgage approvals was unchanged at 66k in September. Nationwide house price rose 0.2% mom in October. From Japan, Tokyo CPI core was unchanged at 0.5% yoy in October, missed expectation of 0.7% yoy.

In Europe, currently, FTSE is down -0.58%. DAX is down -0.15%. CAC is up 0.06%. German 10-year yield is down -0.0107 at -0.341. Earlier in Asia, Nikkei rose 0.47%. Hong Kong HSI dropped -0.39%. China Shanghai SSE dropped -0.87%. Singapore Strait Times rose 0.36%. Japan 10-year JGB yield rose 0.0229 to -0.109.

UK Labour said conditions for election are met

As EU has confirmed Brexit extension till January 31, UK opposition Labour indicated that the conditions for supporting a snap election was met. Liberal Democrats and the Scottish National party have already offered support to Prime Minister Boris Johnson’s one-line bill to trigger early election in December. Though, the date was not confirmed yet. Based on current development, the bill will like be passed today. Johnson will refrain from pushing forward with his Brexit bill until a new parliament is formed.

Labour leader Jeremy Corbyn said in a statement,” I have consistently said that we are ready for an election and our support is subject to no-deal Brexit being off the table. We have now heard from the EU that the extension of article 50 to 31 January has been confirmed, so for the next three months, our condition of taking no deal off the table has now been met. We will now launch the most ambitious and radical campaign for real change our country has ever seen.

RBA Lowe: Extraordinarily unlikely to see negative interest rates in Australia

RBA Governor Philip Lowe said in a speech that the key to a return to more normal interest rates globally is to improve the “investment climate”. There are two central elements to do so. First is “reduction in some of the geopolitical and other concerns”. Second is “structural measures” that boost people’s “confidence about future economic growth”.

Domestically, Lowe said this year’s three interest rate cuts as “helping” the Australian economy and supporting the “gentle turning point” in growth. RBA is “prepared to ease” further if needed. But he emphasized it is “extraordinarily unlikely that we will see negative interest rates in Australia”. Though, it’s likely that “an extended period of low interest rates” is required.

RBNZ Hawkesby: Tactical rate cut demonstrate determination to meet inflation target

RBNZ Assistant Governor Christian Hawkesby said in a speech that the -50bps rate cut back in August was a “tactical decision”. A key part was that front-loading would “give inflation the best chance of meeting our policy objectives”. In particular, “it would demonstrate our ongoing determination to ensure inflation increases to the mid-point of the target”. Such commitment should ” support a lift in inflation expectations and an eventual lift in actual inflation.”

The “regret analysis” suggested ” it would be better to do too much too early, than do too little too late.” The alternative approach could risk “inflation remaining stubbornly below target,”. Inflation expectations could “drift lower” and create an “even more challenging task to achieve our objectives.”

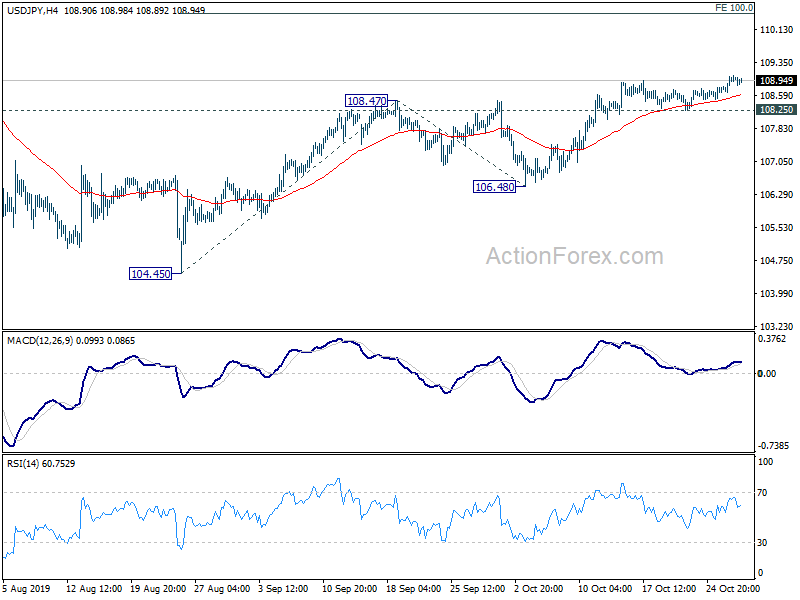

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.73; (P) 108.89; (R1) 109.11; More…

Intraday bias in USD/JPY remains on the upside for the moment. Rise from 104.45 in progress for 109.31 key resistance. Decisive break there will carry larger bullish implications next target will be 100% projection of 104.45 to 108.47 from 106.48 at 110.50. On the downside, however, break of 108.25 support will indicate short term topping and turn bias back to the downside for 106.48 support next.

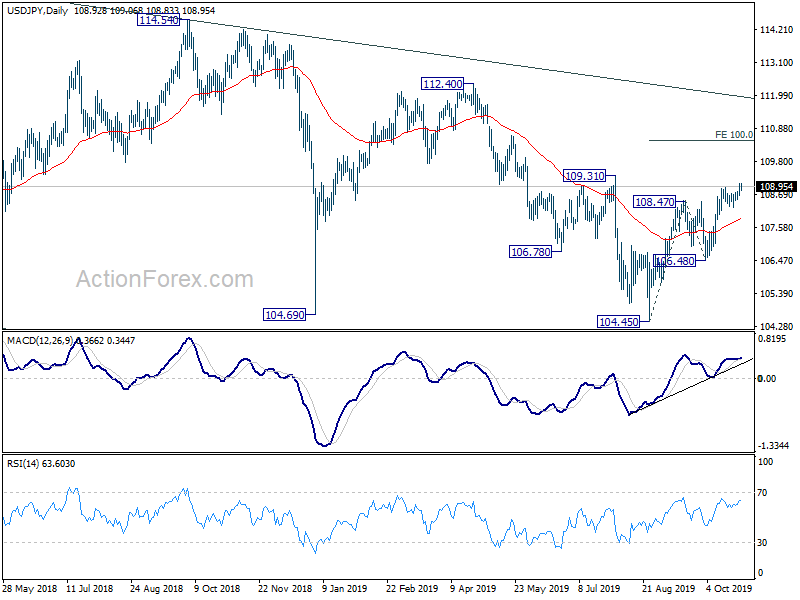

In the bigger picture, strong support was seen from 104.62 again. Yet, there is no confirmation of medium term reversal. Corrective decline from 118.65 (Dec. 2016) could still extend lower. But in that case, we’d expect strong support above 98.97 (2016 low) to contain downside to bring rebound. Meanwhile, on the upside, break of 112.40 key resistance will be a strong sign of start of medium term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Oct | 0.50% | 0.70% | 0.50% | |

| 07:00 | GBP | Nationwide Housing Prices M/M Oct | 0.20% | 0.00% | -0.20% | |

| 09:30 | GBP | Mortgage Approvals Sep | 66K | 65K | 66K | |

| 09:30 | GBP | M4 Money Supply M/M Sep | 0.70% | 0.30% | 0.40% | |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Aug | 2.00% | 2.10% | 2.00% | |

| 14:00 | USD | Consumer Confidence | 128.2 | 125.1 | ||

| 14:00 | USD | Pending Home Sales M/M Sep | 0.90% | 1.60% |