{kind=link}

Sterling is having a roller-coaster ride today. It’s firstly boosted by news that EU and UK has finally agreed to a new Brexit deal. However, the Pound was then quickly knocked down as Northern Ireland’s DUP expressed rejection to it. It seems Brexit drama is not going to end that easily. Sterling is indeed the weakest for today so far. Dollar follows as the second weakest after another string of weaker than expected data. On the other hand, Australian Dollar rides on better than expected job data and is trading as the strongest.

Technically, at this point, further rise is expected in Sterling as long as 1.2655 minor support in GBP/USD, 137.51 minor support in GBP/JPY and 0.8716 minor resistance in EUR/GBP hold. EUR/USD’s break of 1.1109 resistance is now taken as an early sign of medium term bullish reversal. Further rally is expected towards 1.1412 resistance. USD/CAD’s decline from 1.3347 resumes by taking out 1.3171 and should target 1.3133 support next. AUD/USD resumes the rebound from 0.6677, but we’d still expect upside to be limited by 0.6894 resistance to bring larger down trend resumption.

In other markets, currently DOW is up 0.15%. In Europe, FTSE is up 0.76%. DAX is up 0.31%. CAC is flat. German 10-year yield is down -0.0013 at -0.384. Earlier in Asia, Nikkei dropped -0.09%. Hong Kong HSI rose 0.69%. China Shanghai SSE dropped -0.05%. Singapore Strait Times dropped -0.27%. Japan 10-year JGB yield rose 0.0043 to -0.155.

Sterling jumped on Brexit deal, knocked down by DUP rejection

Sterling surged initially on news that a Brexit deal is finally clinched in Brussels today, after marathon discussions this week. The news also take stocks and commodity currencies higher. The agreement came just a few hours ahead of the EU summit. European Commission President Jean-Claude Juncker said in a letter that he would recommend EU27 leaders to approve the deal. And it’s a “high time” to complete the Brexit process.

UK Prime Minister Boris Johnson also said “we have a great new Brexit deal”. His spokesperson added that Johnson is confidence that the new Brexit deal will go forward for a vote in the parliament on Sunday. And, “The public would expect if the deal is passed, for MPs to do everything they can to pass it on time and yes we are confident that we can do that, referring to leaving EU on October 31.

However, the Pound pared pares back some of earlier gains after Northern Ireland’s DUP said it won’t support UK Prime Minister Boris Johnson’s new Brexit deal. In a statement, DUP said: “Following confirmation from the Prime Minister that he believes he has secured a ‘great new deal’ with the European Union the Democratic Unionist Party will be unable to support these proposals in Parliament.” It added: “these proposals are not, in our view, beneficial to the economic well-being of Northern Ireland and they undermine the integrity of the Union…. it is our view that these arrangements would not be in Northern Ireland’s long term interests.”

Released from UK, retail sales rose 0.0% mom, 3.1% yoy in September, versus expectation of 0.5% mom, 3.0% yoy. Ex-fuel sales rose 0.2% mom, 3.0% yoy, versus expectation of -0.3% mom, 2.6% yoy. From Swiss trade surplus widened to CHF 4.02B in September, above expectation of CHF 2.47B.

Philly Fed survey dropped to 5.6, price pressure moderated

Philadelphia Manufacturing Business Outlook Diffusion Index dropped -6 pts to 5.6, missed expectation of 7.1. The percentage of firms reporting increases (27%) this month narrowly exceeded the percentage reporting decreases (21%). Price paid index dropped -16 pts to 16.8, suggesting price pressures moderated.

Philly Fed noted: “Responses to the October Manufacturing Business Outlook Survey suggest growth in manufacturing activity this month. Although they remained positive, the indicators for general activity and shipments fell from their levels in September. The firms reported an improvement in both new orders and employment this month. The survey’s future indexes indicate that respondents continue to expect growth over the next six months.”

US initial jobless claims rose to 214k, above expectation of 212k

US initial jobless claims rose 4k to 214k in the week ending October 12, slightly above expectation of 212k. Four-week moving average of initial claims rose 1k to 214.75k. Continuing claims dropped -10k to 1.679m in the week ending October 5. Four-week moving average of continuing claims rose 3.5k to 1.670m.

Also released, housing starts dropped to 1.26m annualized rate in September. Building permits dropped to 1.39m. Industrial production dropped -0.4% mom in September, worse than expectation of -0.1% mom. From Canada, manufacturing shipments rose 0.8% mom in August, above expectation of 0.0% mom. Canada ADP employment rose 28.2k, missed expectation of 56.5k.

China MOFCOM: Final goal of trade talks is to end trade war and remove all tariffs

Chinese Ministry of Commerce spokesperson Gao Feng said today that the “final goal” of US-China trade negotiation is to “end the trade war and cancel all additional tariffs”. He added, “this would benefit China, the U.S. and the whole world. We hope that both sides will continue to work together, advance negotiations, and reach a phased agreement as soon as possible.”

Also, Gao admitted that “Since this year, under the effect of China-US trade frictions, trade and investment between the U.S. and China have fallen”. “This fully demonstrates that trade wars have no winners”, he added.

Australia unemployment rate dropped to 5.2%,

Australian dollar is lifted by decline in unemployment rate as data showed. While the improvement is welcomed by RBA, it’s far from being enough to confirm a pause in the easing cycle. The economy added 14.7k jobs in September, above expectation of 10.0k. Full-time employment grew 26.2k while part-time employment dropped -11.4k. Unemployment rate dropped -0.1% to 5.2% but participation rate also dropped -0.1% to 66.1%.

The seasonally adjusted unemployment rate increased by 0.2% in New South Wales (4.5%), and by 0.1 % in Queensland (6.5%). Decreases were recorded in South Australia (down 1.0% to 6.3%, following a cumulative increase of 1.3% over the previous two months), Victoria (down 0.2% to 4.7%) and Tasmania (down 0.2% to 6.2%), with Western Australia recording no change.

Australia NAB business confidence dropped to -2, conditions improved to 1

Australia quarterly NAB Business Confidence dropped from 5 to -2 in Q2. Current Business Confidence improved from 1 to 2. However, Business Confidence for the next 3 months dropped from 12 to 9. Business confidence for the next 12 months dropped from 23 to 20. Capex plans for the next 12 months also dropped from 24 to 21.

According to Alan Oster, NAB Group Chief Economist: “There are tentative signs that the trend decline in business conditions since mid-2108 has slowed, but conditions remain below average with only a small increase in Q3. Business confidence saw a sharp fall in Q3 more than reversing the surprising bounce in Q2. It appears that any post-election optimism has faded despite very low interest rates following the back to back interest rate cuts mid-year”.

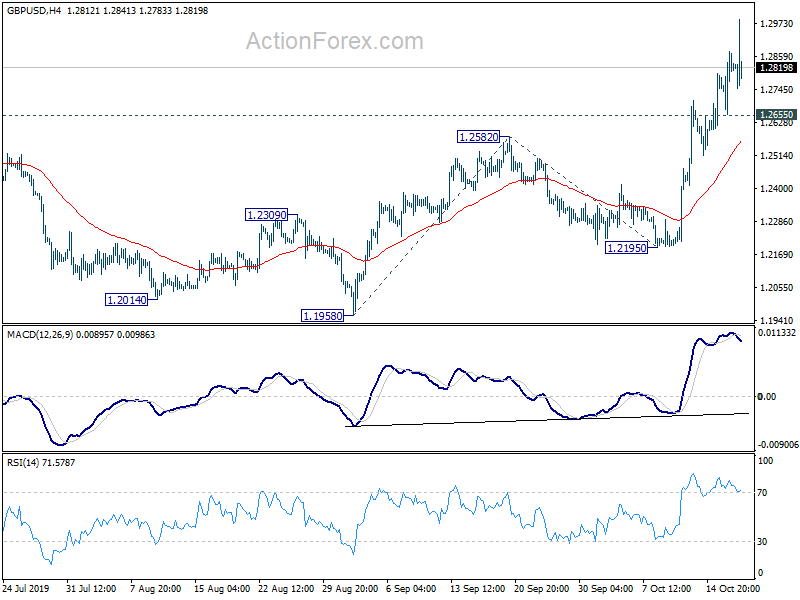

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2701; (P) 1.2786; (R1) 1.2913; More….

GBP/USD spiked higher to 1.2989 earlier today but quickly retreated. Nevertheless, as long as 1.2655 minor support holds, intraday bias remains on the upside. Current rise from 1.1958 should target 161.8% projection of 1.1958 to 1.2582 from 1.2195 at 1.3205 next. On the downside, below 1.2516 minor support will turn intraday bias neutral again. But retreat should be contained well above 1.2195 support for another rally.

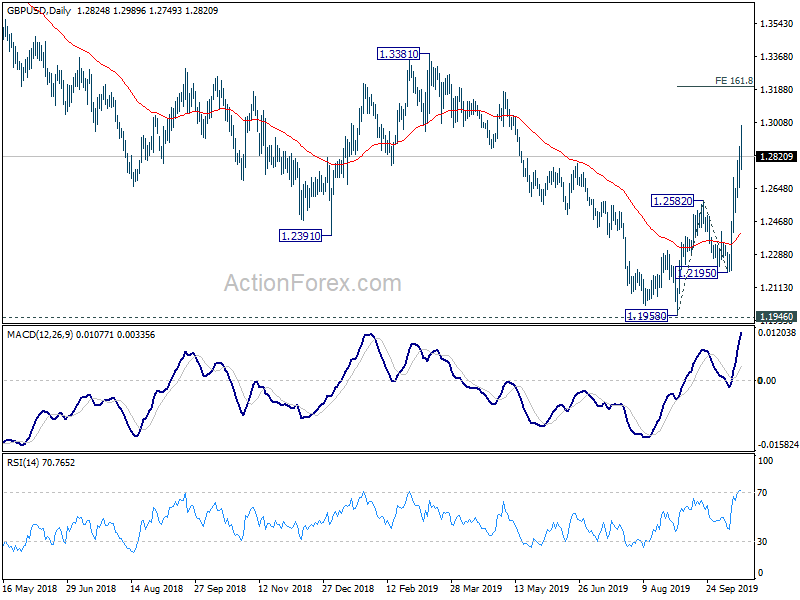

In the bigger picture, current development affirms the case of medium term bottoming at 1.1958, ahead of 1.1946 (2016 low). At this point, rise from 1.1958 is seen as the third leg of consolidation from 1.1946. Further rise would be seen back towards 1.4376 resistance. For now, this will remain the favored case as long as 1.2195 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q/Q Q3 | -2 | 6 | 5 | |

| 00:30 | AUD | Employment Change Sep | 14.7K | 10.0K | 34.7K | 37.9K |

| 00:30 | AUD | Unemployment Rate Sep | 5.20% | 5.30% | 5.30% | |

| 06:00 | CHF | Trade Balance (CHF) Sep | 4.02B | 2.47B | 1.59B | 1.72B |

| 08:30 | GBP | Retail Sales M/M Sep | 0.00% | 0.50% | -0.20% | -0.30% |

| 08:30 | GBP | Retail Sales Y/Y Sep | 3.10% | 3.00% | 2.70% | 2.60% |

| 08:30 | GBP | Retail Sales ex-Fuel M/M Sep | 0.20% | -0.30% | -0.30% | |

| 08:30 | GBP | Retail Sales ex-Fuel Y/Y Sep | 3.00% | 2.60% | 2.20% | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Oct | 5.6 | 7.1 | 12 | |

| 12:30 | USD | Building Permits Sep | 1.39M | 1.34M | 1.43M | |

| 12:30 | USD | Housing Starts Sep | 1.26M | 1.32M | 1.36M | 1.39M |

| 12:30 | USD | Initial Jobless Claims (Oct 11) | 214K | 212K | 210K | |

| 12:30 | CAD | Manufacturing Shipments M/M Aug | 0.80% | 0.00% | -1.30% | |

| 12:30 | CAD | ADP Employment Change Sep | 28.2K | 56.5K | 49.3K | 109.9K |

| 13:15 | USD | Industrial Production M/M Sep | -0.40% | -0.10% | 0.60% | 0.80% |

| 13:15 | USD | Capacity Utilization Sep | 77.50% | 77.80% | 77.90% | |

| 14:30 | USD | Natural Gas Storage | 100B | 98B | ||

| 15:00 | USD | Crude Oil Inventories | 2.7M | 2.9M |