{kind=link}

Overall, the forex markets remain generally quiet in very tight range. Australian dollar edged higher in Asian session as lifted by stronger than expected consumer inflation expectations. Yet, there was on follow through buying. Yen and Dollar are both softer as sentiments remain cautious. Traders are very skeptical on whether any progress could be made in US-China trade negotiations. yet, they’re guarding against any positive surprises for now.

Technically, USD/CAD failed to break through 1.3347 temporary top after yesterday’s rally attempt and more consolidations is likely. Similarly, EUR/AUD also failed to break through 1.6368 temporary top too and consolidations are set to continue. Selloff has clearly lost momentum. GBP/USD and GBP/JPY might be ready for a brief recovery.

In Asia, currently, Nikkei is up 0.26%. Hong Kong HSI is up 0.18%. China Shanghai SSE is up 0.19%. Singapore Strait Times is down -0.12%. Japan 10-year JGB yield is down -0.0006 at -0.206. Overnight, DOW rose 0.70%. S&P 500 rose 0.91%. NASDAQ rose 1.02%. 10-year yield rose 0.046 to 2.087, defended 2% handle well for now.

FOMC minutes: Some wants clarity on when recalibration of policy would end

Minutes of September FOMC meeting noted that “downside risks to the outlook for economic activity had increased somewhat” since July meeting, particularly those stemming from “trade policy uncertainty and conditions abroad.” And, the minutes warned that the developments “seemed more likely to move in directions that could have significant negative effects on the U.S. economy”.

Domestically, “softness in business investment and manufacturing so far this year was seen as pointing to the possibility of a more substantial slowing in economic growth than the staff projected.” And, “risks to the inflation projection were also viewed as having a downward skew, in part because of the downside risks to the forecast for economic activity”.

Yet, regarding the monetary policy path forward, a few participants judged that “expectations regarding the path of the federal funds rate implied by prices in financial markets were currently suggesting greater provision of accommodation at coming meetings than they saw as appropriate”. And, it might be come necessary to “seek a better alignment of market expectations regarding the policy rate path with policymakers’ own expectations for that path.”

Several participants urged to provide “more clarity about when the recalibration of the level of the policy rate in response to trade uncertainty would likely come to an end.”

Chinese Liu said to cut short trade talks in US, White House denied

The South China Morning Post in Hong Kong reported that no progress was made in deputy-level trade talks this week. And Chinese Vice Premier Liu He is set to cut short his trip to Washington. Originally planned to hold two days of meeting on Thursday and Friday, Liu might just leave on Thursday. Though, the rumor was quickly denied by the White House and the spokesman said “We are not aware of a change in the Vice Premier’s travel plans at this time”.

Separately, US Commerce Secretary Wilbur Ross said that “tariffs are finally forcing China to pay attention to our concerns”. Yet, he noted that “trade agreements historically have been very weak on enforcement”. And, “given the magnitude and the complexity of the changes we need, enforcement becomes an extremely critical component of any agreement that we make.”

On the data front

Japan bank lending rose 2.0% yoy in September, matched expectations. PPI dropped to -1.1% yoy, but beat expectation of -1.2% yoy. Machinery orders dropped -2.4% mom in August, above expectation of -2.5% yoy. From Australia, home loans rose 1.8% in August, missed expectation of 3.6%. But consumer inflation expectations accelerated to 3.6%, above expectation of 3.2%.

Looking ahead, Germany trade balance, France industrial output will be featured. But main focus will be on UK GDP and productions, as well as ECB minutes. Later in the day, US CPI will take center stage.

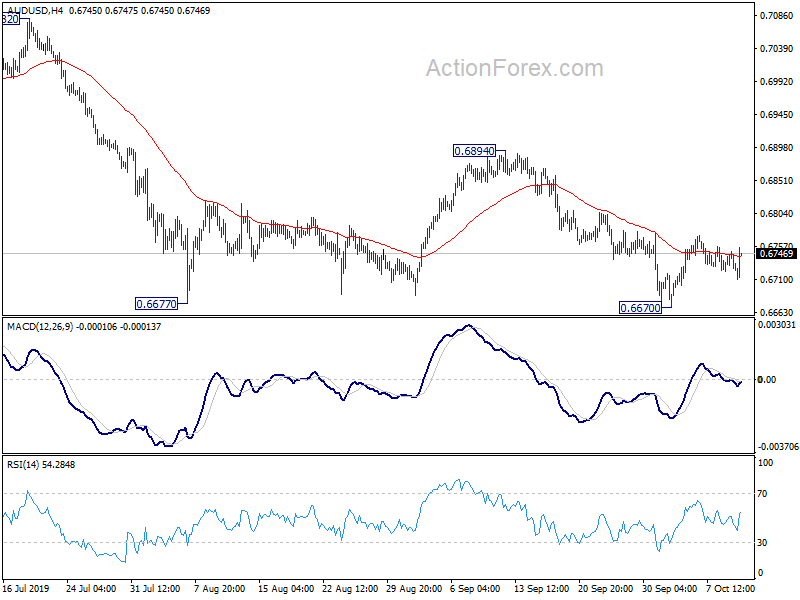

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.6715; (P) 0.6732; (R1) 0.6742; More…

AUD/USD is staying in consolidation from 0.6677 and intraday bias remains neutral first. Recovery might extend but upside upside should be limited by 0.6894 resistance. On the downside, firm break of 0.6670/7 will confirm larger down trend resumption.

In the bigger picture, decline from 0.8135 (2018 high) is seen as resuming the long term down trend from 1.1079 (2011 high). Next target is 0.6008 (2008 low). On the upside, break of 0.7082 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Food Price Index M/M Sep | 0.00% | -0.20% | 0.70% | |

| 23:01 | GBP | RICS Housing Price Balance Sep | -2% | -7% | -4% | |

| 23:50 | JPY | Bank Lending Y/Y Sep | 2.00% | 2.00% | 2.10% | |

| 23:50 | JPY | PPI M/M Sep | 0.00% | -0.10% | -0.30% | |

| 23:50 | JPY | PPI Y/Y Sep | -1.10% | -1.20% | -0.90% | |

| 23:50 | JPY | Machinery Orders M/M Aug | -2.40% | -2.50% | -6.60% | |

| 00:00 | AUD | Consumer Inflation Expectations Oct | 3.60% | 3.20% | 3.10% | |

| 00:30 | AUD | Home Loans Aug | 1.80% | 3.60% | 5.00% | 5.50% |

| 06:00 | EUR | Germany Trade Balance (EUR) Aug | 19.4B | 20.2B | ||

| 06:45 | EUR | France Industrial Output M/M Aug | 0.40% | 0.30% | ||

| 08:00 | EUR | Italy Industrial Output M/M Aug | -1.90% | -0.70% | ||

| 08:30 | GBP | Manufacturing Production M/M Aug | -0.10% | 0.30% | ||

| 08:30 | GBP | Manufacturing Production Y/Y Aug | -0.70% | -0.60% | ||

| 08:30 | GBP | Industrial Production M/M Aug | -0.10% | 0.10% | ||

| 08:30 | GBP | Industrial Production Y/Y Aug | -1.10% | -0.90% | ||

| 08:30 | GBP | Index of Services 3M/3M Aug | 0.10% | 0.20% | ||

| 08:30 | GBP | Goods Trade Balance (GBP) Aug | -10.0B | -9.1B | ||

| 08:30 | GBP | GDP M/M Aug | 0.00% | 0.30% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (Oct 4) | 217K | 219K | ||

| 12:30 | USD | CPI M/M Sep | 0.10% | 0.10% | ||

| 12:30 | USD | CPI Y/Y Sep | 1.80% | 1.70% | ||

| 12:30 | USD | CPI Core Y/Y Sep | 2.40% | 2.40% | ||

| 12:30 | USD | CPI Core M/M Sep | 0.20% | 0.30% | ||

| 12:30 | CAD | New Housing Price Index Y/Y Aug | 0.00% | -0.40% | ||

| 14:30 | USD | Natural Gas Storage | 112B |