{kind=link}

Sterling is back in focus today as UK is heading into constitutional with Prime Minister Boris Johnson’s move to suspend the government. Risk aversion return of risk aversion also keep commodity currencies generally soft. On the other hand,Yen is generally stronger following further decline in major global treasury yields. Though, that was shrugged off by the also strong Dollar.

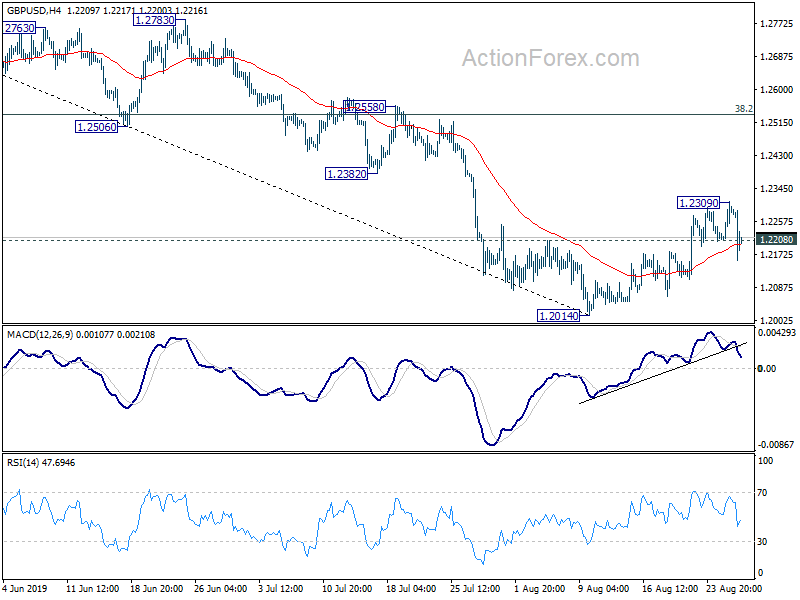

Technically, GBP/USD’s of 1.2208 minor support suggests that corrective recovery from 1.2014 has completed. Further decline would be seen back to retest this low. EUR/GBP drew support from 0.8891/9051 support zone and recovered. Focus is back on 0.9157 minor resistance. Break will indicate completion of fall from 0.9324 and bring retest of this high. GBP/JPY could retest 126.54 short term bottom ahead if Sterling’s selloff worse.

In Europe, currently FTSE is down -0.10%. DAX is down -0.91%. CAC is down -0.82%. German 10-year yield is down -0.0255 at -0.718. Earlier in Asia, Nikkei rose 0.11%. Hong Kong HSI dropped -0.19%. China Shanghai SSE dropped -0.29%. Singapore Strait Times dropped -0.36%. Japan 10-year JGB yield dropped -0.0047 to -0.271.

UK Johnson’s move to suspend government drew furious response from MPs

UK Prime Minister Boris Johnson confirmed that he has asked the Queen for permission to suspended the parliament from “the second sitting week in September”. MPs will then return on October 14, when there will also be a new Queen’s speech. Johnson insisted that MPs would still have “ample time” to debate Brexit, and there is a “bold and ambitious domestic legislative agenda for the renewal of our country after Brexit”. The net effect for the suspension will cut short the time for MPs to introduce legislations to block no-deal Brexit on October 31.

House Speaker John Bercow issued a strong statement, saying that Johnson’s move “represents a constitutional outrage”. He added, “however it is dressed up, it is blindingly obvious that the purpose of prorogation now would be to stop Parliament debating Brexit and performing its duty in shaping a course for the country”.

Labour leader Jeremy Corbyn said “I have protested in the strongest possible terms on behalf of my party and all the other opposition parties that are going to join in with this in saying that suspending parliament is not acceptable, It’s not on.”

Scotland’s First Minister, Nicola Sturgeon also complained that “it’s absolutely outrageous”. And, “shutting down parliament in order to force through a no-deal Brexit which will do untold and lasting damage to the country against the wishes of MPs is not democracy. It’s a dictatorship.”

Eurozone M3 rose 5.2%, solid growth in lending to households and businesses

Eurozone M3 money supply growth accelerated to 5.2% yoy in July, up from 4.5% yoy and beat expectation of 4.7% yoy. M3 growth averaged 4.8% in the three months to July.

Meanwhile, household lending growth accelerated to 3.4% yoy, up from 3.3% yoy, hitting a post-crisis high. Corporate lending growth was unchanged at 3.9% yoy, staying at the highest level this year.

The overall set of data is seen as indication of future activities. And, robust growth in money supply and lending argues that even though the economy is cooling, there is no imminent risk of recession yet.

German Gfk consumer confidence unchanged, but economic outlook suffered a significant decline

German Gfk Consumer Confidence for September was unchanged at 9.7, slightly above expectation of 9.6. The underlying picture was mixed though, with increase in propensity to buy, slight deterioration in income expectation. By contrast, the economic outlook suffered a significant decline.

Economic indicator dropped -8.3 pts to -12.0, hitting the lowest level in more than six years since January 2013. Gfk noted: “The global economic downturn, trade wars and the ongoing discussions surrounding Brexit are all putting increasing pressure on the economic outlook of consumers.”

RBNZ Orr: Lower interest rates offer greater certainty on the financial and investment front

RBNZ Governor Adrian Orr said in an article that “monetary policy (the domain of central banks) has its limitations and needs to be partnered with broader fiscal and structural economic policy (the domain of the government of the day)… Providing certainty in uncertain times is a great skill to have, and central bankers world-wide are working hard to do just that.”

He added that “lower interest rates do not remove the global political uncertainty.” But they “offer greater certainty on the financial and investment front”. And, “businesses and governments should be re-assessing their hurdle rates on their investment projects. Low and stable global interest rates mean that what was once costly may now be a sound investment for the future.”

Also from down under, Australia construction work done dropped -3.8% in Q2, worse than expectation of -1.0%.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2228; (P) 1.2269; (R1) 1.2329; More….

GBP/USD’s break of 1.2208 minor support suggests corrective recovery from 1.2014 has completed at 1.2309 already. Intraday bias is turned back to the downside for retesting 1.2014 first. Break will resume larger down trend to 1.1946 low. On the upside, above 1.2309 will extend the recovery. But upside should be limited by 38.2% retracement of 1.3381 to 1.2014 at 1.2536 to bring down trend resumption.

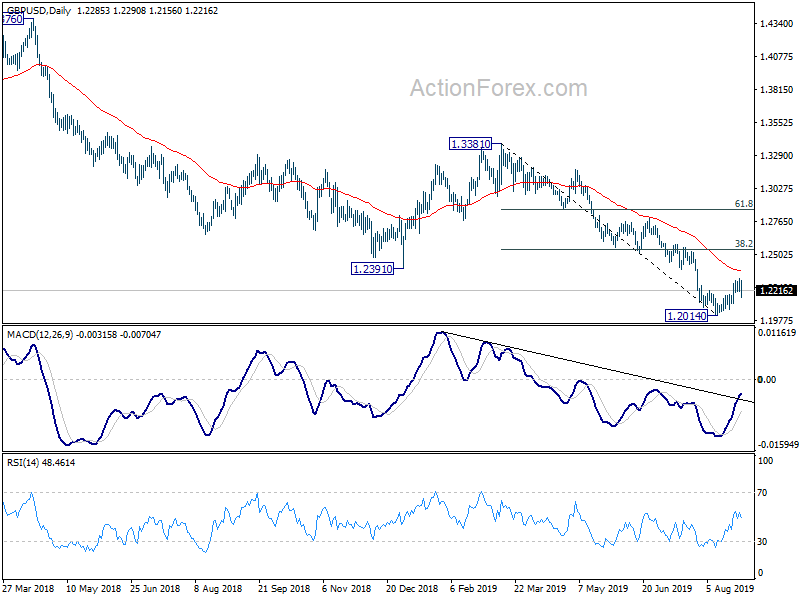

In the bigger picture, down trend from 1.4376 (2018 high) is extending towards 1.1946 low. We’d be cautious on bottoming there. But decisive break will resume down trend from 2.1161 (2007 high) to 61.8% projection of 1.7190 to 1.1946 from 1.4376 at 1.1135. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Aug | -0.40% | -0.10% | ||

| 1:30 | AUD | Construction Work Done Q2 | -3.80% | -1.00% | -1.90% | -2.20% |

| 6:00 | EUR | German Import Price Index M/M Jul | -0.20% | -0.10% | -1.40% | |

| 6:00 | EUR | German GfK Consumer Confidence Sep | 9.7 | 9.6 | 9.7 | |

| 8:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | 5.20% | 4.70% | 4.50% | |

| 14:30 | USD | Crude Oil Inventories | -2.7M |