{kind=link}

Yen strengthens broadly today again as the pull back lost momentum. After all the words and rhetorics, US-China trade war is still in progress for escalation. Yesterday’s early selloff in risk markets might be overdone. But current recovery doesn’t indicate any change in the down trend in stocks, nor major treasury yields. Risk-off could come back any time. For now, Yen is the strongest for today, followed by Canadian and Swiss Franc. Australian and New Zealand Dollars are the weakest.

Technically, USD/CAD is having a steep fall today as recent consolidation from 1.3345 extends. But near term outlook remains bullish as long as 1.3177 support holds. Another rise through 1.3345 is still expected at a later stage. USD/JPY is still on track for more decline with 106.73 minor resistance intact. Similarly, near term outlook is EUR/JPY stays bearish as long as 119.58 minor resistance holds too.

In Asia, currently, Nikkei is up 1.15%. Hong Kong HSI is up 0.10%. China Shanghai SSE is up 1.68%. Singapore Strait Times is up 0.20%. Japan 10-year JGB yield is up 0.02 at -0.255. Overnight, DOW rose 1.05%. S&P 500 rose 1.10%. NASDAQ rose 1.32%. 10-year yield rose 0.017 to 1.545.

Japan Aso to watch current market move with sense of urgency

At a regular press conference, Japanese Finance Minister Taro Aso emphasized that “currency stability is important”. He added that “we must closely watch the currency market move with a sense of urgency. Though, he didn’t give any comment of specific exchange rate levels. The comments came after Yen spiked higher yesterday in response to abrupt escalation of US-China trade war.

Aso also noted that recent market volatility won’t change the government stance on the planned sale tax hike. The government will still proceed with October’s sale take hike from 8% to 10%, unless there is serious shocks in the economy.

RBA Debelle: Exchange rate plays important role of external shock absorber

RBA Deputy Governor Guy Debelle warned that US-China trade war poses a “significant risk” to Australia and the rest of the world. He also defended the existing rules-based global trading system. He said, “despite some flaws, that system has delivered sizeable benefits for global growth and welfare”, and “Australia has clearly been a major beneficiary of that system.”

Nevertheless, Debelle also noted that Australia is “less vulnerable” to external shocks now. He said “if you look at the balance sheet of the country as a whole, Australia has a net foreign currency asset position”. “Hence when the exchange rate depreciates, the value of net foreign liabilities actually declines rather than increase. To reiterate, this allows the exchange rate to play the important role of shock absorber to external shocks”, he added.

RBNZ Orr: Global investment on hold for political uncertainty in many, many regions

In an interview by Australian Financial Review, RBNZ Governor Adrian Orr said the “single biggest” factor for -50bps rate cut was domestic. Inflation expectations were starting to decline and “we didn’t want to be behind the curve”. He added, “we want to keep inflation expectations positive – near the mid-point of the band.” But Orr also noted that “global interest rates had swung dramatically between our monetary policy statements.” And the large swing in forward interest rates suggested “a significant story behind that.”

Orr also noted “investments has really been on hold for a while” globally, “given political uncertainty across many, many regions”. ” US-China escalating trade challenge, and that’s real now… Likewise, other countries: the Italians without government, Brexit, Hong Kong… So that manifests itself from being a political uncertainty, to capital no longer being invested. So this is one of the rolling challenges that’s happening.”

ECB Kazimir: Credible policy action needs broad unity and agreement

ECB Governing Council member Peter Kazimir said yesterday that he was leaning toward “action, doing something” at the September meeting. Though, he also emphasized that “we need to take steps that are credible in the eyes of the market.” And, “credibility also means broad unity and agreement on the measures.”

Kazimir also noted that there are no limits on what ECB could pick from its toolbox. However, economic outlook differs across Eurozone. Thus, finding a consensus for the whole are is important. And he preferred “the broadest agreement”.

On the data front

Japan corporate service price index rose 0.5% yoy in July, below expectation of 0.6% yoy. German GDP and UK BBA mortgage approvals will be released in European session. House price indices and consumer confidence will be the main feature in US session.

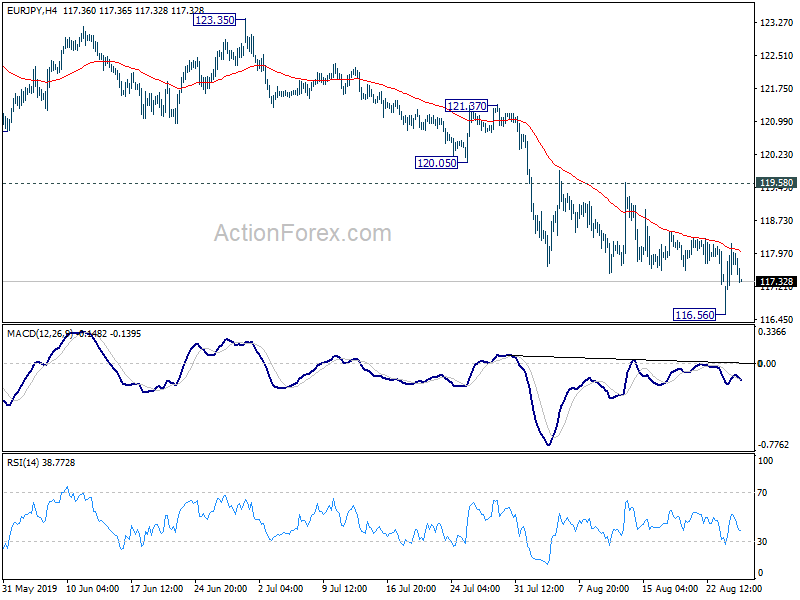

EUR/JPY Daily Outlook

Daily Pivots: (S1) 116.85; (P) 117.52; (R1) 118.46; More….

EUR/JPY recovered quickly after spiking lower to 116.56. Intraday bias is turned neutral for some consolidations first. Upside of recovery should be limited by 119.58 resistance to bring fall resumption. On the downside, break of 116.56 will resume larger down trend to 114.84 medium term support next. Though, break of 119.58 will indicate short term bottoming and bring stronger rebound.

In the bigger picture, down trend from 137.49 (2018 high) is still in progress. It’s seen as a falling leg of multi-year sideway pattern. Deeper fall could be seen to 109.48 (2016 low and below). On the upside, break of 123.35 resistance is needed to the first sign medium term reversal. Otherwise, outlook will remain bearish in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Y/Y Jul | 0.50% | 0.60% | 0.70% | |

| 6:00 | EUR | German GDP Q/Q Q2 F | -0.10% | -0.10% | ||

| 8:30 | GBP | BBA Mortgage Approvals Jul | 42854 | 42653 | ||

| 13:00 | USD | House Price Purchase Index Q/Q Q2 | 0.20% | 1.10% | ||

| 13:00 | USD | House Price Index M/M Jun | 0.20% | 0.10% | ||

| 13:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Jun | 2.40% | 2.39% | ||

| 14:00 | USD | Consumer Confidence Index Aug | 129 | 135.7 |