{kind=link}

Swiss Franc rises broadly today as risk aversion stays in the markets, even though Yen is firm but relatively unmoved. Sterling also recovers with help from stronger than expected wage growth. On the other hand, New Zealand and Canadian Dollars are the weakest while Australian is not too far away. Though, it should noted that Dollar is soft today despite stronger than expected inflation reading. It seems that pickup in inflation wouldn’t stop Fed for further easing should trade tensions escalate further.

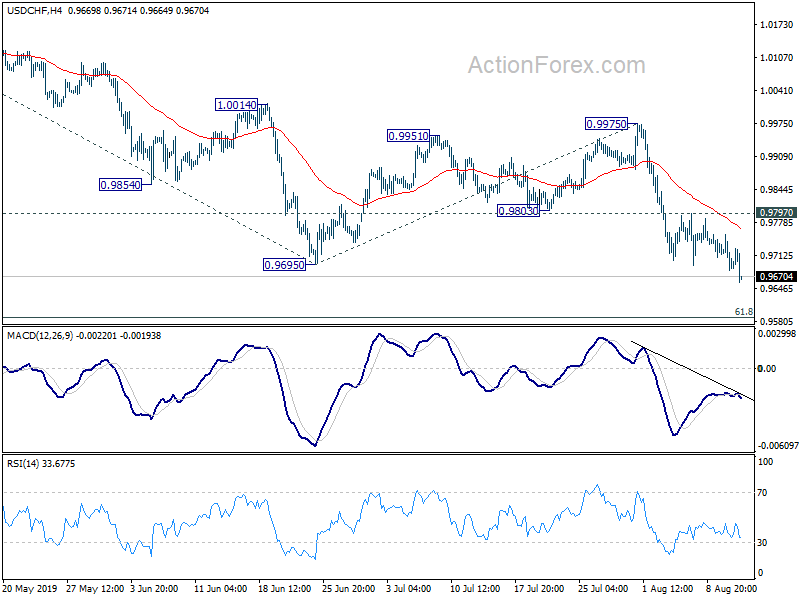

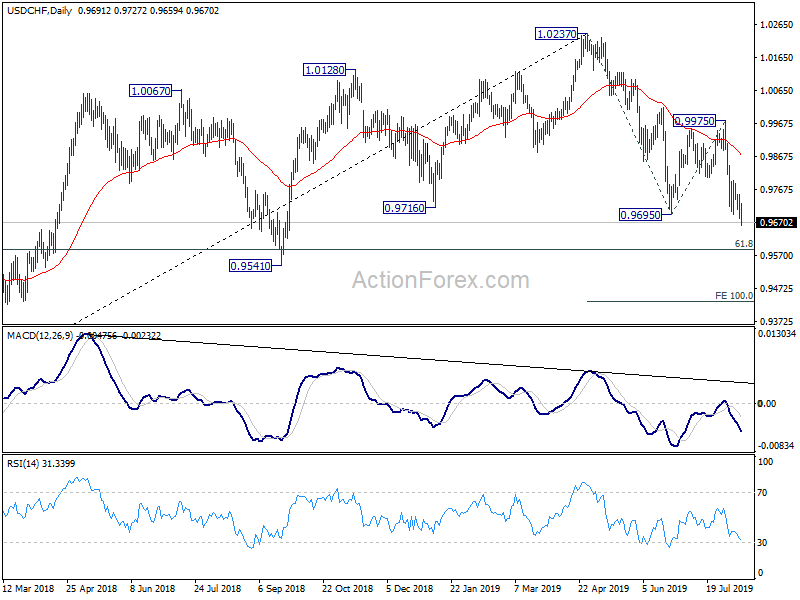

Technically, USD/CHF’s break of 0.9695 support should indicate resumption of fall from 1.0237 to 0.9587 fibonacci level. EUR/CHF also breaks 1.0863 support to resume recent down trend to 1.0645 projection level. Yen crosses would be the focus today, in particular with it’s correlation to treasury yields. Further decline in 10- and 30-year yields in US could drag Yen crosses lower, in particular USD/JPY.

In Europe, currently, FTSE is down -0.81%. DAX is down -1.16%. CAC is down -0.72%. German 10-year yield is down -0.0169%. German 10-year yield is down -0.0169 at -0.606.

Earlier in Asia, Nikkei dropped -1.11%. Hong Kong HSI dropped -2.10%. China Shanghai SSE dropped -0.63%. Singapore Strait Times dropped -0.70%. Japan 10-year JGB yield dropped -0.0147 to -0.234.

US CPI accelerated to 1.8%, core up to 2.2%

US CPI rose 0.3% mom in July, matched expectations. Core CPI rose 0.3% mom, above expectations. Annually, CPI accelerated to 1.8% yoy, up from 1.6% yoy, beat expectation of 1.7% yoy. Core CPI accelerated to 2.2% yoy, up from 2.1% yoy and beat expectation of 2.1% yoy.

Trump appears to be happy with the inflation reading as well as his tactics with China. He tweeted: “Through massive devaluation of their currency and pumping vast sums of money into their system, the tens of billions of dollars that the U.S. is receiving is a gift from China. Prices not up, no inflation. Farmers getting more than China would be spending.”

Trump said to request Japanese PM Abe to buy farm products

Japanese Kyodo news agency reported that Trump is urging Japanese Prime Minister Shinzo Abe to increase purchase of US agricultural products, worthing several hundred millions USD including transport costs.

The request came as US and Japan are crafting out a broad trade agreement, reportedly by September. Also, it came as China halted its own purchase of US farm goods as trade tensions escalated recently.

Kyodo also said that Trump has specifically asked Japan to by products such as soybeans and wheat. Yet, he preferred such purchases to be outside of the framework of the current trade talks. Japan government is said to be considering its own responses. And one proposal was to by such farm products as food support for Africa.

German ZEW dropped to -44.1, significant deterioration in outlook

German ZEW Economic Sentiment dropped to -44.1 in August, down from -24.5 and missed expectation of -28.0. That’s the lowest level sine December 2011, and well below long term average of 21.6. Current Situation Index dropped to -13.5, down from -1.1 and missed expectation of -5.9. Eurozone ZEW Economic Sentiment dropped to -43.6, down from -20.3, missed expectation of -21.7. Eurozone Current Situation dropped -3.9 pts to -14.5.

“The ZEW Indicator of Economic Sentiment points to a significant deterioration in the outlook for the German economy. The most recent escalation in the trade dispute between the US and China, the risk of competitive devaluations, and the increased likelihood of a no-deal Brexit place additional pressure on the already weak economic growth. This will most likely put a further strain on the development of German exports and industrial production,” comments ZEW President Professor Achim Wambach.

Also released, German CPI was finalized at 0.5% mom, 1.7% yoy in July.

UK unemployment rate rose to 3.9%, but wage growth accelerated

UK unemployment rate rose to 3.9% in the three months to June, up from 3.8%, above expectation of 3.8%. Unemployment rate came in at 4.1% for men and 3.6% for women, the latter being joint lowest since comparable records began in 1971. For the same period, an estimated 1.33m people were unemployment, 33k fewer than a year ago.

On wage growth, estimated annual growth in average weekly earnings for employees increased to 3.7% yoy for total pay (including bonuses), matched expectation and up from May’s 3.5% yoy. Excluding bonuses, weekly earnings rose 3.9% yoy, up from 3.6% yoy and beat expectation of 3.8% yoy.

Japan: South Korea fails to show how we fall short of export control measures

Japan criticized South Korea’s removal of the country from export whitelist today, as trade tension continued to intensify. South Korea announced to move Japan into a newly created export category, for the latter’s frequent violation of basic rules.

Japanese Industry Minister Hiroshige Seko said South Korea has failed to show how Japan had fallen short of international export control measures. He added, “from the start, it is totally unclear under what basis South Korea can say that Japan’s export control measures don’t meet the export control regime.”

On the other hand, South Korean President Moon Jae-in said today that “the Japanese government made a decision to exclude South Korea from white-listed countries, following export restrictions… It is disappointing and regrettable in light of the two countries’ shared efforts for friendship and cooperation.”

From Japan, machine tools orders dropped -33.0% yoy in July. Tertiary industry index dropped -0.1% mom in June. Domestic CGPI rose 0.0% mom in July.

Australia NAB business conditions dropped to 2, further RBA easing and fiscal support expected

Australian NAB Business Confidence rose from 2 to 4 in July. On the other hand, Business Conditions dropped from 4 to 2. In particular, Employment Conditions dropped sharply from 5 to 0.

Alan Oster, NAB Group Chief Economist said “the decline in business conditions since early 2018 has been broad-based and has continued to track at below average levels in recent months.” And, “this is concerning, because while conditions remain positive, it points to a significant loss in momentum in the business sector”.

Business confidence “ticked-up” but is “also below average”. While there were some positive signs with a post-election lift in confidence, this bounce now looks to have been short lived with confidence also tracking at below average levels in the two months since the election”

And, “with a significant loss of momentum in activity, and inflation indicators remaining weak, the survey points to the need to the need for further stimulus in the economy. Indeed, we expect a further easing in interest rates from the RBA and think that some greater fiscal support will be needed from the government to kickstart growth”.

Singapore slashes 2019 growth forecasts to 0.0-1.0%, uncertainties and risks increased

Singapore Ministry of Trade and Industry downgraded 2019 growth forecast to 0.0-1.0%, and expect growth to come in at around mid-point of the forecast range. That’s notably lower from prior estimate of 1.5-2.5%, after Q2 GDP contracted by -3.3%. The Ministry noted in the statement that “GDP growth in many of Singapore’s key final demand markets in the second half of 2019 is expected to slow from, or remain similar to, that recorded in the first half.”.

Also, “uncertainties and downside risks in the global economy have increased since three months ago”. The risks firstly include US new tariffs on USD 300B in Chinese imports. Secondly, a “a steeper-than-expected slowdown” of China, as precipitated by US tariffs, could lead to a “sharp fall” in Chinese import demands and “negatively affect the region’s growth”. Thirdly, risk of no-deal Brexit “has increased with the recent change in UK’s political leadership.” Fourthly, there are risks from uncertainties in Hong Kong, the trade dispute between Japan and South Korea, as well as geopolitical tensions in North Korea and the Strait of Hormuz.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9665; (P) 0.9709; (R1) 0.9737; More…

USD/CHF’s firm break of 0.9695 support now suggests resumption of fall from 1.0237. Intraday bias is back on the downside for 0.9587 fibonacci level first. Break will target 100% projection of 1.0237 to 0.9695 from 0.9975 at 0.9433. On the upside, break of 0.9797 minor resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, up trend from 0.9186 (2018 low) should have completed at 1.0237 already. Deeper decline would be seen to 61.8% retracement of 0.9186 to 1.0237 at 0.9587 and below. For now, USD/CHF is seen as in long term range pattern between 0.9186 and 1.0342. Hence, we’d pay attention to bottoming signal below 0.9587. Nevertheless, break of 0.9975 resistance is needed to indicate completion of the decline from 1.0237. Otherwise, risk will stay on the downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI M/M Jul | 0.00% | 0.10% | -0.50% | |

| 01:30 | AUD | NAB Business Conditions Jul | 2 | 1 | 3 | |

| 01:30 | AUD | NAB Business Confidence Jul | 4 | 3 | 2 | |

| 04:30 | JPY | Tertiary Industry Index M/M Jun | -0.10% | -0.10% | -0.20% | 0.00% |

| 06:00 | EUR | German CPI M/M Jul F | 0.50% | 0.50% | 0.50% | |

| 06:00 | EUR | German CPI Y/Y Jul F | 1.70% | 1.70% | 1.70% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Jul P | -33.00% | -37.90% | ||

| 08:30 | GBP | Jobless Claims Change Jul | 28.0K | 42.0K | 38.0K | 31.4K |

| 08:30 | GBP | Claimant Count Rate Jul | 3.20% | 3.20% | ||

| 08:30 | GBP | Average Weekly Earnings 3M/Y Jun | 3.70% | 3.70% | 3.40% | 3.50% |

| 08:30 | GBP | Weekly Earnings ex Bonus 3M/Y Jun | 3.90% | 3.80% | 3.60% | |

| 08:30 | GBP | ILO Unemployment Rate 3Mths Jun | 3.90% | 3.80% | 3.80% | |

| 09:00 | EUR | German ZEW Economic Sentiment Aug | -44.1 | -28 | -24.5 | |

| 09:00 | EUR | German ZEW Current Situation Aug | -13.5 | -5.9 | -1.1 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Aug | -43.6 | -21.7 | -20.3 | |

| 10:00 | USD | NFIB Small Business Optimism Jul | 104.7 | 104 | 103.3 | |

| 12:30 | USD | CPI M/M Jul | 0.30% | 0.30% | 0.10% | |

| 12:30 | USD | CPI Y/Y Jul | 1.80% | 1.70% | 1.60% | |

| 12:30 | USD | CPI Core M/M Jul | 0.30% | 0.20% | 0.30% | |

| 12:30 | USD | CPI Core Y/Y Jul | 2.20% | 2.10% | 2.10% |