{kind=link}

Dollar rises notably in early US session after stronger than expected US GDP data. The solid data rises further question on whether Fed would really cut interest rate next week. Even so, a -50bps cut is basically out of question. The greenback is followed by Yen and the Euro. On the other hand, Australian Dollar is the weakest one, followed by New Zealand Dollar., and the Sterling.

Technically, 0.9951 resistance in USD/CHF, 108.99 resistance in USD/JPY and 0.6910 support in AUD/USD will be watched for further Dollar strength. Though, the most important levels will be 1.1107 low in EUR/USD and 1.2391 low in GBP/USD. These two levels are the most important for the greenback to overcome.

In Europe, currently, FTSE is up 0.61%. DAX is up 0.21%. CAC is up 0.50%. German 10-year yield is down -0.010 at -0.371. Earlier in Asia, Nikkei dropped -0.45%. Hong Kong HSI dropped -0.69%. China Shanghai SSE rose 0.24%. Singapore Strait Times dropped -0.52%. Japan 10-year JGB yield rose 0.0008 to -0.149.

US GDP grew 2.1% in Q2, above expectation of 1.8%

US GDP grew 2.1% annualized in Q2, better than expectation of 1.8%. GDP price index rose 2.4% qoq, below expectation of 4.0% qoq.

There were contributions from GDP growth from personal consumption expenditures (PCE), federal government spending, and state and local government spending. They were partly offset by negative contributions from private inventory investment, exports, nonresidential fixed investment and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

Deceleration in growth reflected downturns in inventory investment, exports, and nonresidential fixed investment. These downturns were partly offset by accelerations in PCE and federal government spending.

ECB SPF: Inflation forecast from 2019 to 2021 revised down by -0.1%

According to Q3 ECB Survey of Professional Forecasters, average forecast for HICP inflation is 1.3% for 2019, 1.4% for 2020 and 1.5% for 2021. There were downward revisions of -0.1% for each of those years comparing with Q2 forecast. Average long-term inflation expectation was lowered from 1.8% to 1.7%.

Growth is projected to average 1.2% in 2019, 1.3% in 2020 and 1.4% in 2021. There was no change in expectation of 2019 and 2021. But 2020 figure was revised down by -0.1%. Average longer-term expectations for real GDP growth were unchanged at 1.4%.

Ireland Coveney: Johnson deliberately set UK on collision course with EU

UK Prime Minister Boris Johnson’s spokesman said Johnson spoke with French President Emmnauel Macron on Thursday night. Discussions moved on to Brexit that Johnson “will be setting out the same message which he delivered in the House of Commons”. That is, “the withdrawal agreement has been rejected three times by the House of Commons, it’s not going to pass, so that means reopening the withdrawal agreement and securing the abolition of the backstop.”

Referring to Johnson’s statements in House, Ireland’s Foreign Minister, Simon Coveney, said they are “very unhelpful” tot he Brexit process. Coveney said Johnson “seems to have made a deliberate decision to set Britain on a collision course with the European Union and with Ireland in relation to the Brexit negotiations.” And, “the approach that the British prime minister seems to now be taking is not going to be the basis of an agreement, and that’s worrying for everybody.”

French State Minister for European affairs Amelie de Montchalin said Macron will hold discussion with Johnson in the coming week and “What is still to negotiate is the future relationship… We have to create a working relationship and not get into games, gestures and provocations.”

Japan said to remove South Korea from trade whitelist

Kyodo news reported that, as trade frictions intensified, Japan is going to remove South Korea from the white list of countries that gives the latter preferential treatment in trade. The announcement could be made as soon as on August 2, and change could take effect after 21 days.

Japan is reported to have cited “significantly undermined” trust between the two countries and “certain issues” with South Korea’s export controls and regulations. After the move, products and technology that could be diverted to military use would need to obtain approval from Ministry of Economy before exporting to South Korea.

Asked about the plan, Chief Cabinet Secretary Yoshihide Suga told a news conference that nothing had been decided on the time frame. There are currently 27 countries on Japan’s white list including the United States, Britain, Germany, Australia, New Zealand and Argentina.

Suggested reading:

MOFCOM: Trade frictions cannot stop US enthusiasm for Chinese market

China’s Assistance Commerce Minister Ren Hongbin said that US companies are keen to participate in the second China International Import Expo (CIIE), to be held on Nov. 5-10 in Shanghai. He expects the number of US participants to exceed last year’s. He added, “for the United States, even through there are some bilateral trade frictions, it cannot stop U.S. firms from attaching importance to the Chinese market and their great enthusiasm for the Chinese market.”

Vice Commerce Minister Wang Bingnan also said China will further lower import tariffs and open up its market to foreign firms. He added, “the purpose of our holding of the import expo is not simply expanding imports, but putting more emphasis on improving import structures while keeping export growth steady.”

Separately, US trade delegation, led by Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin, will arrive in Shanghai next week, for the first face-to-face meeting since Trump-Xi summit in Japan.

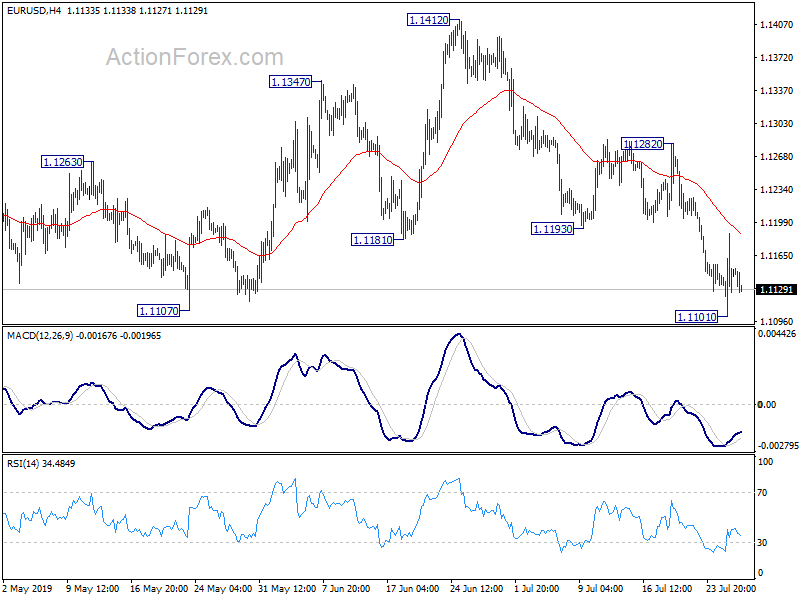

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1103; (P) 1.1145; (R1) 1.1190; More…

EUR/USD is staying in range above 1.1101 and intraday bias remains neutral first. As long as 1.1282 resistance holds, further decline is expected. Sustained break of 1.1107 low will resume larger down trend from 1.2555. Though, firm break of 1.1282 will bring stronger rise to 1.1412 resistance.

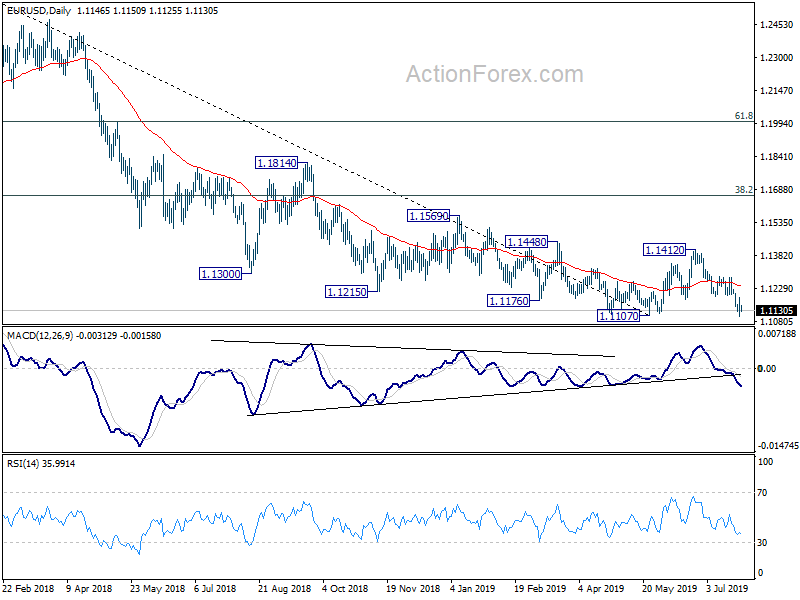

In the bigger picture, on the one hand, 1.1107 is seen as a medium term bottom on bullish convergence condition in weekly MACD. On the other hand, rejection by 55 week EMA retains medium term bearishness. Outlook stays neutral for now. On the downside, break of 1.1107 will resume the down trend from 1.2555 (2018 high) to 78.6% retracement of 1.0339 to 1.2555 at 1.0813. Meanwhile, break of 1.1412 will resume the rebound to 38.2% retracement of 1.2555 to 1.1107 at 1.1660.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Jul | 0.90% | 0.80% | 0.90% | |

| 06:00 | EUR | German Import Price Index M/M Jun | -1.40% | -0.80% | -0.10% | |

| 12:30 | USD | GDP Annualized Q2 A | 2.10% | 1.80% | 3.10% | |

| 12:30 | USD | GDP Price Index Q/Q Q2 | 2.40% | 4.00% | 0.90% |