{kind=link}

Dollar stabilizes in Asian session after steep decline overnight. Bets on Fed’s rate cut this month jumped after dovish comments from some key Fed officials. It seems that Fed might choose not to listen to the solid economic data released recently, but opt for the path of insurance. Treasury yield also tumbled notably. Gold rides on the greenback’s weakness and breaks 1440 handle.

Staying in the currency markets, Dollar is indeed not the worst performing one for the week so far. But Sterling is the weakest, followed by Euro and the Canadian. New Zealand Dollar is the strongest for the week, followed by Australian and the Yen. But the picture could still change before weekly close.

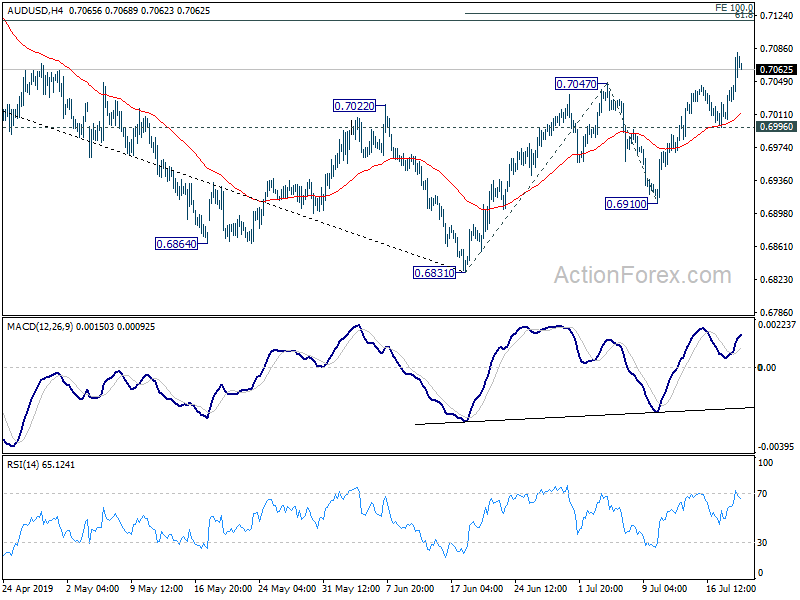

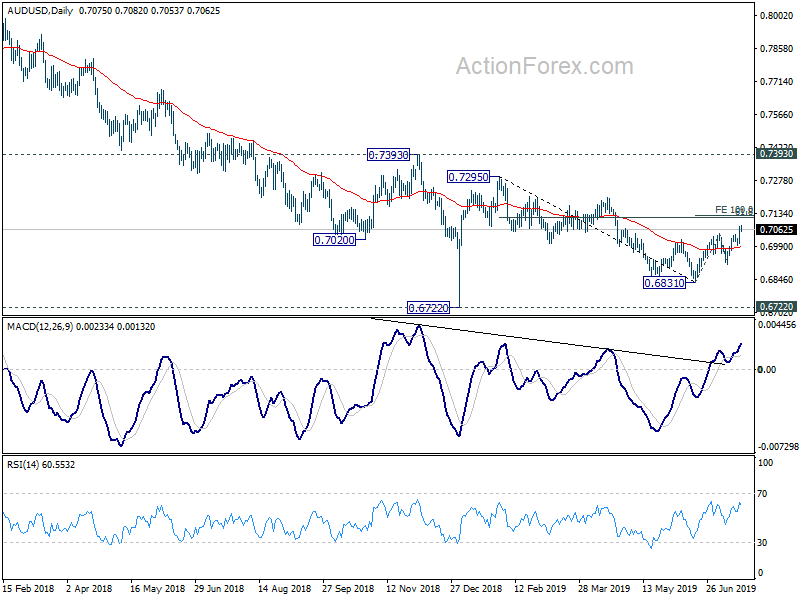

Technically, AUD/USD’s break of 0.7047 resistance confirmed resumption of rise from 0.6831 for 0.7118 fibonacci level next. USD/CAD breached 1.3018 temporary low but couldn’t sustain below 1.3052/68 cluster support yet, probably waiting for Canadian retail sales. EUR/USD is stuck in range of 1.1193/1285 despite yesterday’s rebound, keeping near term outlook neural. GBP/USD is also held below 1.2579 resistance so far, keeping near term outlook bearish.

In Asia, major stock markets surge on expectations of Fed cut. Nikkei is up 1.96%. Hong Kong HSI is up 1.07%. China Shanghai SSE is up 0.77%. Singapore Strait Times is up 0.38%. Japan 10-year JGB yield is up 0.0023 at -0.133. Overnight, DOW rose 0.01%. S&P 500 rose 0.36%. NASDAQ rose 0.27%. 10-year yield dropped -0.023 to 2.038.

Bet on 50bps Fed cut surged after New York Fed Williams’ comments

Dollar tumbled broadly as markets took New York Fed President John William’s speech as indication of aggressive rate cut in the upcoming FOMC meeting on July 31. Fed fund futures now indicate 46.2% chance of -50bps cut, comparing to 34.3% a day ago and 19.9% a week ago. Overall, markets are still pricing 100% chance of easing then.

Williams said in a speech “Living Life Near the ZLB” (Zero Lower Bound), that when interest rates are in the vicinity of the ZLB, policymakers shouldn’t “keep your powder dry”. That is, they should “move more quickly to add monetary stimulus” to “vaccinate against further ills”.

Also, he said “it’s better to take preventative measures than to wait for disaster to unfold”. And, “when you only have so much stimulus at your disposal, it pays to act quickly to lower rates at the first sign of economic distress.”

Later, in an unusual step, a New York Fed spokesperson “clarified” Williams’ comments. She said, “this was an academic speech on 20 years of research. It was not about potential policy actions at the upcoming FOMC meeting.”

Fed Clarida: Don’t wait until data turns decisively before cutting rates

Fed Vice Chair Richard Clarida also reinforced Williams’ dovish comments. Clarida told Fox Business Network that “you don’t need to wait until things get so bad to have a dramatic series of rate cuts.” And, “you don’t want to wait until data turns decisively if you can afford to.”

Clarida reiterated that the US economy is “in a good place”. But “we’ve had mixed data” and “disinflationary pressures, if anything, are more intense than I thought six weeks ago.” He added, “we need to make a decision based on where we think the economy may be heading and, importantly, where the risks to the economy are lined up.”

Fed Bullard: Trump moved trade uncertainty to front burner and thus an insurance cut is needed

In a CNN interview, St. Louis Fed President James Bullard said trade uncertainty used to be an issue that was on the “back burner”. However, “the president moved it to the front burner”. And now, “trade uncertainty is high and I don’t see that declining anytime soon”.

Bullard added that the economy is “slowing down” and warned “what if it slows more than we think, possibly because of a trade war?”. A rate cut would “provide a bit of insurance against that”.

Nevertheless, regarding a 50bps cut, Bullard said “I don’t think we need to go that far” adding that “the critical thing here is to get inflation and inflation expectations better centered.”

Japan CPI core slowed to 0.6%, lowest since July 2017

Japan CPI core (ex-fresh food) slowed to 0.6% yoy in June, down from 0.8% yoy and matched expectations. All items CPI was unchanged at 0.7% yoy, while CPI core-core (ex-fresh food and energy) was also unchanged at 0.5% yoy.

CPI core was the lowest reading since July 2017. No turnaround is expected in the near term. Instead, CPI core could be further dragged down by policy related factors, including mobile phone charges and education costs.

The dim inflation outlook highlights the pressure for BoJ to ramp up monetary stimulus. In particular, both Fed and ECB are expected to loosen up policy again later this week.

Looking ahead

Germany PPI, Eurozone current account and UK public sector net borrowing will be released in European session. Canada will release retail sales. US will release U of Michigan sentiment.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7029; (P) 0.7053; (R1) 0.7100; More…

AUD/USD’s rebound from 0.6831 resumed by taking out 0.7047 and reaches as high as 0.7082 so far. Intraday bias is back on the upside for 61.8% retracement of 0.7295 to 0.6831 at 0.7118, and possibly to 100% projection of 0.6831 to 0.7047 from 0.6910 at 0.7126. Sustained break there will indicate solid upside momentum for 0.7205 resistance next. ON the downside, break of 0.6996 will suggest that the rebound has completed and turn bias to the downside for 0.6910 support instead.

In the bigger picture, with 0.7393 key resistance intact, medium term outlook remains bearish. The decline from 0.8135 (2018 high) is seen as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Jun | 0.60% | 0.60% | 0.80% | |

| 4:30 | JPY | All Industry Activity Index M/M May | 0.30% | 0.30% | 0.90% | 0.80% |

| 6:00 | EUR | German PPI M/M Jun | -0.10% | -0.10% | ||

| 6:00 | EUR | German PPI Y/Y Jun | 1.50% | 1.90% | ||

| 8:00 | EUR | Eurozone Current Account (EUR) May | 21.2B | 20.9B | ||

| 8:30 | GBP | Public Sector Net Borrowing (GBP) Jun | 3.4B | 4.5B | ||

| 12:30 | CAD | Retail Sales M/M May | 0.30% | 0.10% | ||

| 12:30 | CAD | Retail Sales Ex Auto M/M May | 0.40% | 0.10% | ||

| 14:00 | USD | U. of Mich. Sentiment Jul P | 98.6 | 98.2 |