{kind=link}

Dollar rebound strongly in early US session, with support from strong retail sales data. Though, upside is somewhat capped by industrial production miss. Canadian Dollar is, instead, the strongest one. On the other hand, Sterling is the weakest one for today despite solid employment data. UK unemployment rate stayed at 45-year low while wage growth accelerated. But that’s overshadowed by renewing no-deal Brexit fear. Both runners Boris Johnson and Jeremy Hunt rejected Irish backstop in any part of Brexit deal. Such position will make Brexit negotiations very tough ahead. Euro is the second weakest as German ZEW Economic Sentiment deteriorated further in July.

Technically, GBP/USD’s break of 1.2439 temporary low suggests fall resumption for 1.2391 low. Break there will resume medium term decline. GBP/JPY also resumes recent decline from 148.87 for 131.51 low. EUR/GBP takes out 0.9010 resistance earlier today and should be heading to 0.9101 key resistance next. EUR/JPY break s121.31 minor support and is heading to 120.78 low for resuming larger decline from 127.50. A focus is now on 1.1193 support in EUR/USD and break will revive near term bearishness for 1.1107 low.

In other markets, major US indices open mildly lower while 10-year yield is up 0.0349 at 2.127. In Europe, currently, FTSE is up 0.45%. DAX is up 0.25%. CAC is up 0.53%. German 10-year yield is up 0.003 at -0.248. Earlier in Asia, Nikkei dropped -0.69%. Hong Kong HSI rose 0.23%. China Shanghai SSE dropped -0.16%. Singapore Strait Times rose 0.36%. Japan 10-year JGB yield dropped -0.0071 to -0.121.

US retail sales rose 0.4%, ex-auto sales rose 0.4%, far above expectations

US retail sales rose 0.4% mom in June, above expectation of 0.1%. Ex-auto sales also rose 0.4%, above expectation of 0.1%. Also from US, import price index dropped -0.9% mom in June, worse than expectation of -0.7% mom. Industrial production rose 0.0% mom in June, below expectation of 0.1% mom. Capacity utilization dropped to 77.9%, down from 78.1%.

ECB Villeroy: Should not rely too exclusively on market based inflation expectation measures

ECB Governing Council member Francois Villeroy de Galhau reiterated his stance that ECB rate decision should be “data dependent”. In the upcoming meeting, policymakers will “assess actual economic data and we will act accordingly if and when needed.”

He acknowledged that policymakers would “take account of market indications” but emphasized “must not be market dependent”. That is ECB should not rely “too exclusively for inflation expectations on market-based measures”.

Additionally, Villeroy also noted monetary policy is limited as it cannot repair the damage from protectionism, or replace structural reforms or more selective fiscal policies. And, “monetary policies cannot do everything and cannot perform miracles.”

German ZEW dropped to -24.5, a lasting containment of factors are causing uncertainty

German ZEW Economic Sentiment dropped to -24.5 in July, down from -21.1 and missed expectation of -22. Current Situation Index dropped to -1.1, down from 7.8 and missed expectation of 5. Eurozone ZEW economic sentiment dropped slightly to -20.3, down from -20.3 and beat expectation of -20.9. Eurozone Current Situation index dropped -6.9 to -10.6.

ZEW President Achim Wambach said: “Continued negative trend in incoming orders in the German industry is likely to have reinforced the financial market experts’ pessimistic sentiment. A lasting containment of the factors that are causing uncertainty in the export-oriented sectors of the German economy is currently not in sight. The Iran conflict seems to be intensifying and the ongoing trade dispute between the USA and China is a burden not only to Chinese economic development. Furthermore, no discernible progress has been made in the negotiations as to what Brexit will look like.”

Also released, Eurozone trade surplus widened to EUR 20.2B in May, above expectation of EUR 16.4B.

UK unemployment rate stayed at 45-yr low, wage growth picked up

UK unemployment rate was unchanged at 3.8% in the three months to May, matched expectations. It was the lowest level since December 1974. Average weekly earnings including bonus grew 3.4% 3moy, much higher than expectation of 3.1% 3moy. Average weekly earnings excluding bonus also grew 3.6% 3moy, above expectation of 3.5% 3moy. In June, jobless claims rose 38.0k, above expectation of 18.9k.Claimant count rate rose 0.1% to 3.2%.

New Zealand CPI rose 0.6% qoq, more RBNZ easing still needed

New Zealand CPI rose 0.6% qoq 1.7% yoy in Q2, matched expectations. The annual rate accelerated from 1.5% yoy in Q1. However, the rise in headline inflation was largely due to the 5.8% quarter increase in petrol price, which contributed 0.25% to the 0.6% qoq figure. That suggests the pick-up could be temporary only, not to mention that annual CPI remains firmly below 2% mid-point of RBNZ’s 1-3% target range.

Stronger monetary stimulus and economic growth is required to lift inflation sustainably back to the 2% target. Yet, domestic and global headwinds remain. Thus, more OCR cuts are still expected for RBNZ. August could be the month to deliver even though it’s not totally certain yet.

RBA minutes indicate easing bias, but wait-and-see first

In the minutes of July 2 RBA rate meetings, it’s noted that “the Board would continue to monitor developments in the labour market closely and adjust monetary policy if needed to support sustainable growth in the economy and the achievement of the inflation target over time.” The conclusion indicates that RBA is still adopting an easing bias after cutting interest rate in both June and July meeting. However, the next move will come “if needed”, as the central will first “monitor developments” to see how the economy reacts to the prior rate cuts.

Suggested readings on RBA:

- RBA’s July Minutes – Cutting Rate to Weaken Aussie and Lower Unemployment Rate

- RBA Board Minutes Signal a Pause in the Easing Cycle

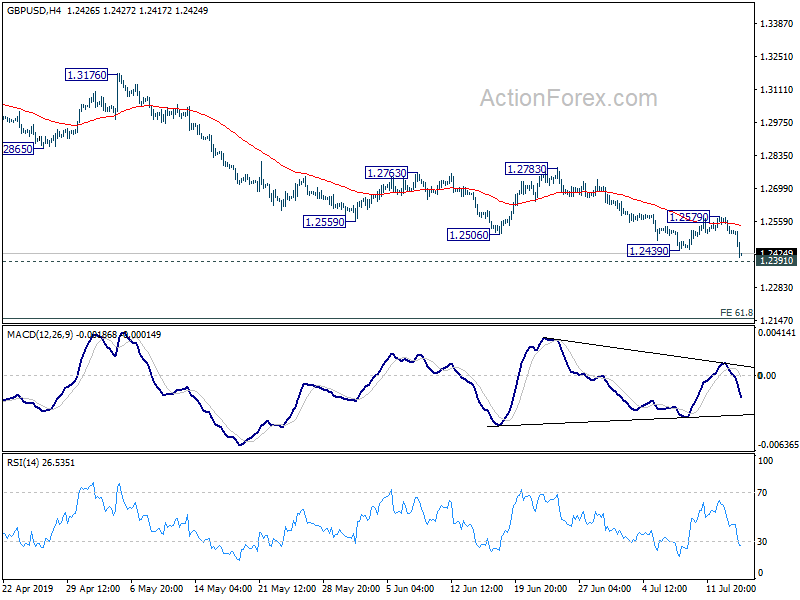

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2491; (P) 1.2535; (R1) 1.2559; More….

GBP/USD drops to as low as 1.2408 so far today as fall from 1.3381 resumes. Intraday is back on the downside for retesting 1.2391 low. Firm break will resume larger down trend for 61.8% projection of 1.4376 to 1.2391 from 1.3381 at 1.2154 next. On the upside, break of 1.2579 resistance is needed to indicate short term bottoming. Otherwise, outlook remains bearish in case of recovery.

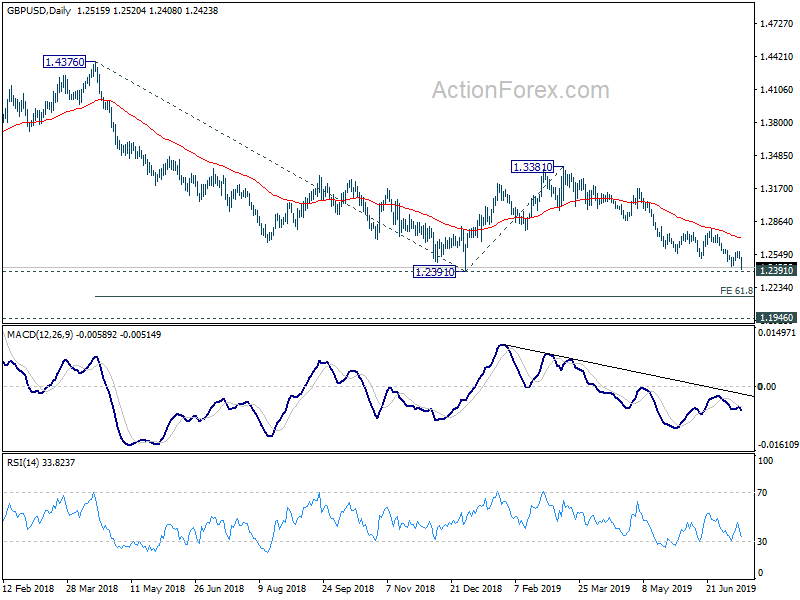

In the bigger picture, down trend from 1.4376 (2018 high) is still in progress. Break of 1.2391 would target a test on 1.1946 long term bottom (2016 low). For now, we don’t expect a firm break there yet. Hence, focus will be on bottoming signal as it approaches 1.1946. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q2 | 0.60% | 0.60% | 0.10% | |

| 22:45 | NZD | CPI Y/Y Q2 | 1.70% | 1.70% | 1.50% | |

| 01:30 | AUD | RBA Minutes Jul | ||||

| 08:30 | GBP | Claimant Count Rate Jun | 3.20% | 3.10% | ||

| 08:30 | GBP | Jobless Claims Change Jun | 38.0K | 18.9K | 23.2k | 24.5K |

| 08:30 | GBP | Average Weekly Earnings 3M/Y May | 3.40% | 3.10% | 3.10% | 3.20% |

| 08:30 | GBP | Weekly Earnings ex Bonus 3M/Y May | 3.60% | 3.50% | 3.40% | |

| 08:30 | GBP | ILO Unemployment Rate 3Mths May | 3.80% | 3.80% | 3.80% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | 20.2B | 16.4B | 15.3B | |

| 09:00 | EUR | German ZEW Economic Sentiment Jul | -24.5 | -22 | -21.1 | |

| 09:00 | EUR | German ZEW Current Situation Jul | -1.1 | 5 | 7.8 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | -20.3 | -20.9 | -20.2 | |

| 12:30 | CAD | International Securities Transactions (CAD) May | 10.20B | 5.02B | -12.80B | |

| 12:30 | USD | Import Price Index M/M Jun | -0.90% | -0.70% | -0.30% | |

| 12:30 | USD | Retail Sales Advance M/M Jun | 0.40% | 0.10% | 0.50% | 0.40% |

| 12:30 | USD | Retail Sales Ex Auto M/M Jun | 0.40% | 0.10% | 0.50% | 0.40% |

| 13:15 | USD | Industrial Production M/M Jun | 0.00% | 0.10% | 0.40% | |

| 13:15 | USD | Capacity Utilization Jun | 77.90% | 78.10% | 78.10% | |

| 14:00 | USD | NAHB Housing Market Index Jul | 64 | 64 | ||

| 14:00 | USD | Business Inventories May | 0.40% | 0.50% |