{kind=link}

Dollar remains the strongest one for the week even though upside momentum is diminishing today. The single most important factor for Dollar’s next move is whether Fed would cut interest rate at this month’s meeting. A 50bps cut is basically priced out by the markets, but futures still indicate 100% chance of a 25bps cut. Hopefully, markets would finally get a clue from Fed Chair Jerome Powell’s semi-annual Congressional testimony. The greenback could be given a strong boost should Powell suggest that a July cut is far from certain.

Staying in the currency markets, Canadian Dollar is also firm today as markets await BoC rate decision. No change is expected and with some solid economic data recently, BoC is given some room to turn more “neutral”. Sterling is among the weakest together with Australian Dollar. The Pound could be under much pressure should GDP and production data disappoint.

In Asia, Nikkei is currently down -0.03%. Hong Kong HSI is up 0.42%. China Shanghai SSE is down -0.02%. Singapore Strait Times is up 0.61%. Japan 10-year JGB yield is up 0.009 at -0.131. Overnight, DOW dropped -0.08%. S&P 500 rose 0.12%. NASDAQ rose 0.54%. 10-year yield rose 0.020 to 2.054.

Fed Harker: No immediate need to move interest rate in either direction

Philadelphia Fed President Patrick Harker told WSJ yesterday that “there’s no immediate need to move rates in either direction at this point in my view”. He noted that the economy “continues to be strong” with “very strong labor market”. If the economy was “weakening substantially”, he would support a rate cut. But “at this point, I do not see that”.

Harker acknowledged that inflation below 2% target is a concern. But he added, “it’s one that I don’t see as an imminent crisis”. Also, he believed “we can give it some time to move back up to 2%.

Additional, he didn’t se December rate hike as a “particularly bad move” as it was not significant at that point. For now he thought the “prudent path” was to “hold steady and see how the economy evolves”.

US & China trade teams held constructive call, but no miracles yet

Leaders of both US and China trade teams held “constructive” telephone conversations yesterday, as negotiations continued. US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin joined the talks. On the Chinese side, there were Vice Premier Liu He and Minister of Commerce Zhong Shan. The call was also confirmed by Chinese Commerce Minister in a brief statement today.

White House economic adviser Larry Kudlow said the talks “went well” and were constructive, but “there are no miracles here”. He added, “there was headway last winter and spring, then it stopped. Hopefully we can pick up where we left off, but I don’t know that yet.”

Kudlow also said yesterday that “President Xi is expected, we hope in return for our accommodations, to move immediately, quickly, while the talks are going on, on the agriculture (purchases).” However, it’s also reported by Hong Kong South China Morning Post that Xi had made no specific commitment regarding the purchases during the meeting with Trump at G20 in Osaka. So far, no significant increase in purchase is noted yet.

Australia consumer confidence dropped sharply despite RBA rate cuts

Australia Westpac Consumer Confidence dropped sharply by -4.1% to 96.5 in July, hitting a two year low. The deterioration came as a surprise as confidence was not supported by recent positive developments, including RBA’s rate cuts and easing US-China trade tensions.

Deepening concerns over Australian economic outlook were the main drivers in decreasing confidence. Expectations in economic conditions for the next 12 months dropped -12.3 to 87.1. That’s the lowest level in four years. For the next 5 years, expectations index dropped -6.7 to 91.6.

After two rate cuts in June and July, Westpac expects RBA to stand pat at next meeting on August 6. Updated economic projections to be released then would give the best guide to how the RBA sees the case for further policy action. Westpac expects a further 25bps cut most likely coinciding with a downgrade to the Bank’s growth and inflation forecasts in November. Though, it said “the timing of this next move remains highly uncertain”.

Also released, Japan domestic CGPI dropped -0.1% yoy in June versus expectation of 0.4% yoy. China CPI was unchanged at 2.7% yoy in June. PPI slowed to 0.0% yoy.

Looking ahead

UK data will take center stage in European session, with GDP, productions and trade balance featured. BoC is widely expected to keep interest rate unchanged at 1.75%. Fed Chair Jerome Powell’s semi annual Congressional testimony and FOMC minutes will be closely watched.

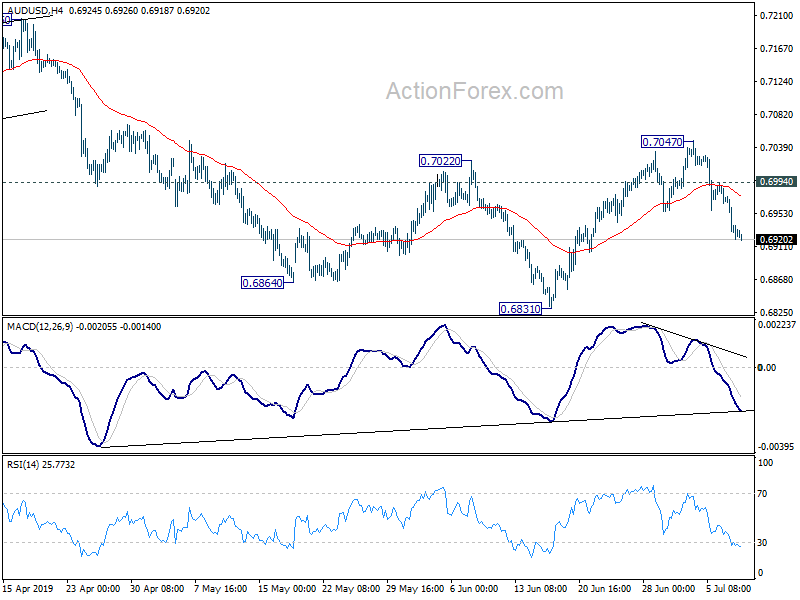

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.6906; (P) 0.6945; (R1) 0.6968; More…

AUD/USD’s strong break of 0.6956 minor support confirmed completion of corrective rebound from 0.6831 at 0.7047. Intraday bias is now on the downside for retesting 0.6831 low next. Break will resume the decline from 0.7295 to 0.6722 low. On the upside, though, break of 0.6994 minor resistance will turn focus back to 0.7047 resistance instead.

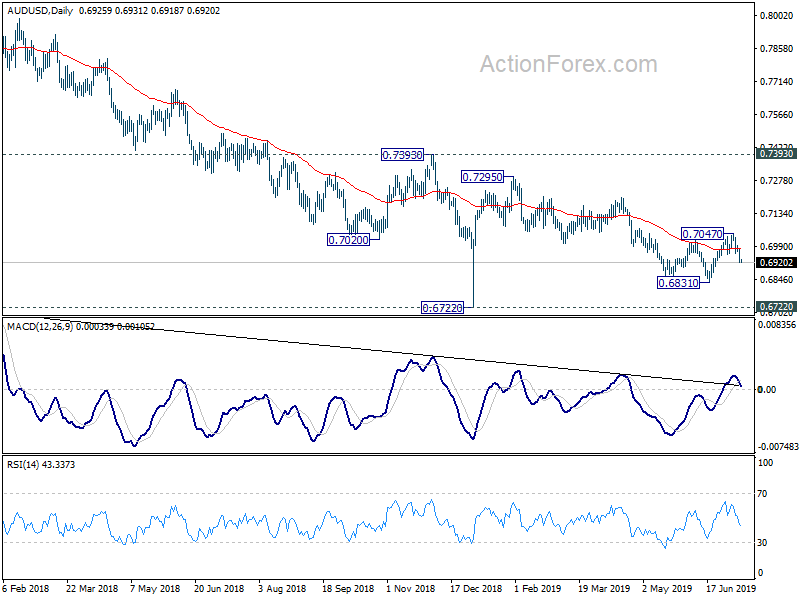

In the bigger picture, with 0.7393 key resistance intact, medium term outlook remains bearish. The decline from 0.8135 (2018 high) is seen as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Jun | -0.10% | 0.40% | 0.70% | 0.60% |

| 0:30 | AUD | Westpac Consumer Confidence Jul | -4.10% | -0.60% | ||

| 1:30 | CNY | CPI Y/Y Jun | 2.70% | 2.70% | 2.70% | |

| 1:30 | CNY | PPI Y/Y Jun | 0.00% | 0.30% | 0.60% | |

| 8:30 | GBP | Monthly GDP M/M May | 0.30% | -0.40% | ||

| 8:30 | GBP | Industrial Production M/M May | 1.50% | -2.70% | ||

| 8:30 | GBP | Industrial Production Y/Y May | 1.20% | -1.00% | ||

| 8:30 | GBP | Manufacturing Production M/M May | 2.20% | -3.90% | ||

| 8:30 | GBP | Manufacturing Production Y/Y May | 1.10% | -0.80% | ||

| 8:30 | GBP | Construction Output M/M May | 0.40% | -0.40% | ||

| 8:30 | GBP | Index of Services 3M/3M May | 0.10% | 0.20% | ||

| 8:30 | GBP | Visible Trade Balance (GBP) May | -12.5B | -12.1B | ||

| 14:00 | CAD | BoC Rate Decision | 1.75% | 1.75% | ||

| 14:00 | USD | Fed Chair Powell Testimony | ||||

| 14:00 | USD | Wholesale Inventories M/M May F | 0.40% | 0.40% | ||

| 14:30 | USD | Crude Oil Inventories | -1.1M | |||

| 18:00 | USD | FOMC Meeting Minutes Jun |