{kind=link}

Dollar continues to trade as the strongest one, riding on US-China agreement to put trade war escalation on hold. US stocks also follow global markets sharply higher, with DOW trading up over 1% at initial trading. Canadian Dollar follows closely as second strongest, with help from WTO oil’s rally. Oil price is firstly lifted by the trade news. Secondly, OPEC and Russia agreed to extend production cut by nine months. Euro is the third strongest as unemployment rate dropped to record low of 7.5% in May. On the other hand, Yen and Swiss Franc are among the weakest on risk appetite. Australian Dollar ignore stocks’ rally and is the second weakest, awaiting RBA rate cut tomorrow.

Technically, for now, no important resistance level in Dollar is taken out firmly yet. And there is no confirmation of bullish reversal in the greenback despite today’s rebound. As noted before, 1.1317 minor support in EUR/USD, 1.2642 support in GBP/USD, 0.9854 resistance in USD/CHF and 108.80 resistance in USD/JPY need to be taken out firmly, better together, to confirm Dollar strength.

In Europe, currently, FTSE is up 1.27%. DAX is up 1.34%. CAC is up 0.81%. German 10-year yield is down -0.186 at -0.343. Earlier in Asia, Nikkei rose 2.13%. China Shanghai SSE rose 2.22%. Hong Kong HSI was on holiday. Singapore Strait Times rose 1.52%. Japan 10-year JGB yield rose 0.153 to -0.146.

Fed Clarida: Baseline outlook positive, with growth at or slightly above trend

Fed Vice Chair Richard Clarida maintained his view that the US economy is “in a good place in terms of lower unemployment rate and the inflation rate a little bit below our 2% objective”. Also, the baseline outlook “continues to be a positive one”. That is, the committee “sees growth at or slightly above trend, sees the unemployment rate remaining low and the inflation rate rising gradually toward 2%.”

Though, he also noted that with the Beige Book survey, “we are hearing increasing references and mentions of uncertainty about policy, and particularly uncertainty about the outlook for trade negotiations, having a potential impact on business investments”.

Clarida also noted uncertainties from trade, global growth and business investments. Also, his fellow central banks saw stronger case for policy easing relative to just two months again. He reiterated Fed’s stance that “we will certainly act as appropriate to put in place policies that sustain the economic expansion, and the strong labor market and price stability.”

UK PMI manufacturing dropped to 48.0, lowest since Feb 2013

UK PMI Manufacturing dropped to 48.0 in June, down from 49.4 and missed expectation of 49.5. That’s also the lowest level since February 2013. Looking at some details, manufacturing production contracted at fastest pace since October 2012. New export orders dropped for the third straight month. Business optimism dropped to third lowest level on record. Employment fell for the third straight month.

Rob Dobson, Director at IHS Markit, said “the downturn in UK manufacturing deepened during June, as the impact of firms unwinding stockpiles built before the original Brexit date continued to reverberate through the sector and exacerbate weak demand… There will need to be a substantial improvement in economic conditions at home and overseas, alongside reductions in both Brexit and domestic political uncertainties, if manufacturing is to see a sustained revival in the coming quarters.”

Also from UK, mortgage approvals dropped to 65.4k May, below expectation of 65.5k. M4 money supply dropped -0.1% mom in May, well below expectation of 0.4% mom.

Eurozone PMI manufacturing finalized at 47.6, remained stuck firmly in a steep downturn

Eurozone PMI Manufacturing was finalized at 47.6 in June, revised down from 47.8, versus May’s 47.7. Among the member states, Germany reading was revised down to 45.0, but that was a 4-month high. Austria dropped to 55-month low at 47.5. Spain dropped to 74-month low at 47.9. Italy dropped to 3-month also at 48.4. Ireland dropped to 72-month low at 49.8. All these readings are contractionary. Expansionary reading including Netherlands at 50.7, but that’s still at 73-month low. France was revised down from 52.0 to 51.9, a high month high. Greece dropped to 19-month low at 52.4.

Chris Williamson, Chief Business Economist at IHS Markit said,”Eurozone manufacturing remained stuck firmly in a steep downturn in June, continuing to contract at one of the steepest rates seen for over six years. The disappointing survey rounds off a second quarter in which the average PMI reading was the lowest since the opening months of 2013, consistent with the official measure of output falling at a quarterly rate of approximately 0.7% and acting as a major drag on GDP.”

Eurozone unemployment rate dropped to record low

Eurozone unemployment rate dropped -0.1% to 7.5% in May, beat expectation of 7.6%. That’s also the lowest level since July 2008. EU 28 unemployment rate also dropped -0.1% to 6.3%. Among the Member States, the lowest unemployment rates in May 2019 were recorded in Czechia (2.2%), Germany (3.1%) and the Netherlands (3.3%). The highest unemployment rates were observed in Greece (18.1% in March 2019), Spain (13.6%) and Italy (9.9%).

Also from Eurozone, M3 money supply rose 4.8% yoy in May, above expectation of 4.6%. PMI manufacturing was finalized at 47.6 in June, revised down from 47.8. From Germany, unemployment dropped -1k in June versus expectation of 0.0%. Unemployment rate was unchanged at 5.0% in June, matched expectations.

ECB Lane: Current policy toolkit effective, further easing case be added if required

ECB chief economist Philip Lane said current monetary policy package has been “effective”. And, “the effectiveness of the policy toolkit means that we can add further monetary accommodation.” He added “further easing can be provided if required to deliver our mandate.” He also noted “especially when inflation deviates from its objective for an extended period, central banks ‒ including the ECB ‒ should adopt clear communication strategies that leave no doubt about their absolute commitment to meeting the inflation objective over the medium term.”

ECB Governing Council member Olli Rehn, a potential successor to chairman Mario Draghi, said the central bank stands ready to use all its tools to lift inflation. Rehn said in a conference in Helsinki, “the Governing Council stands ready to adjust all of its instruments, as appropriate, so that inflation continues to converge towards our inflation aim in a sustained manner.” However, he also noted that “the ECB – much like other central banks – operates in a new environment where long-run trends, such as population aging, lower long-term interest rates and climate change have become key policy issues.” Those make case for a policy review that requires a deeper assessment.

China Caixin PMI manufacturing dropped to 49.4, second lowest since Jun 2016

China Caixin PMI Manufacturing dropped to 49.4 in June, down from 50.2, and missed expectation of 50.1. It’s also the second lowest since June 2016, and below neutral 50-mark dividing expansion from contraction again. It’s noted that output and new work intakes declined for first time since January. There was renewed reduction in export sales while goods producers cutback input purchasing and payroll numbers

Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said: “Overall, China’s economy came under further pressure in June. Domestic demand shrank notably, foreign demand was still underpinned by front-loading exports, and business confidence fell sharply. It’s crucial for policymakers to step up countercyclical policies. New types of infrastructure, high-tech manufacturing and consumption are likely to be the main policy focuses.”

Also released over the weekend, the official China PMI Manufacturing was unchanged at 49.4 in June, below expectation of 49.5. Official PMI Non-Manufacturing dropped to 54.2, down from 54.3, matched expectations.

Australia AiG PMI manufacturing dropped to 49.4, lowest since Aug 2016

Australia AiG Performance of Manufacturing Index dropped -3.3 pts to 49.4 (seasonally adjusted) in June, below 50-points threshold and was the lowest level since August 2016. In trend terms, PMI dropped -0.4 to 51.9. Three of the six sectors are in deep contraction including metal products, TCF paper & printing, and machinery and equipment. Though, food & beverages, building materials and chemicals are holding first.

Employment data are mixed. average wage index rebounded by 4.2 points to 59.7, indicating a faster rate of wage increases (seasonally adjusted). However, employment index fell by -5.5 points to be broadly stable at 50.1.

Japan Tankan large manufacturing index dropped to near three year low

Japan Q2 Tankan survey showed large manufacturing index deteriorated to the worst level in nearly three years. But, improvements was seen in the non-manufacturing sector. Capital expenditure also held up well. Overall, the set of data argues that while the economy is stagnating, it’s not falling off the cliff. And, BoJ will likely maintain its baseline of moderate expansion.

Large Manufacturing Index dropped to 7, down from 12 and missed expectation of 9, lowest since September 2016. Large Manufacturers Outlook dropped to 7, down from 8, but beat expectation of 6. Large Non-Manufacturing Index rose to 23, up from 21, beat expectation of 20. Large Non-Manufacturing Outlook dropped to 17, down from 20, missed expectation of 19. All industry capex rose 7.4%, up from 1.2% but missed expectation of 8.1%.

Also from Japan, PMI manufacturing was finalized at 49.3, revised down from 49.5, below the 50 no-change threshold for the second consecutive month. Consumer confidence dropped to 38.7 in June, down from 39.4 and missed expectation of 39.2.

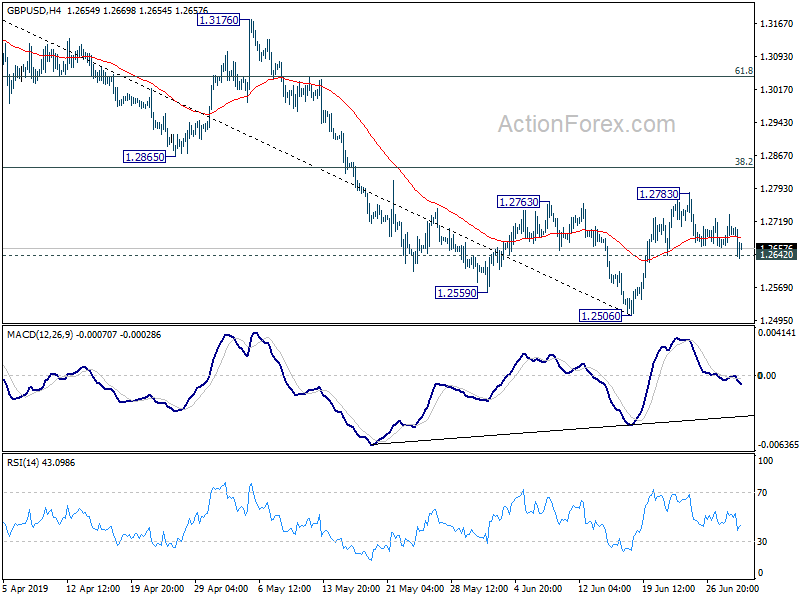

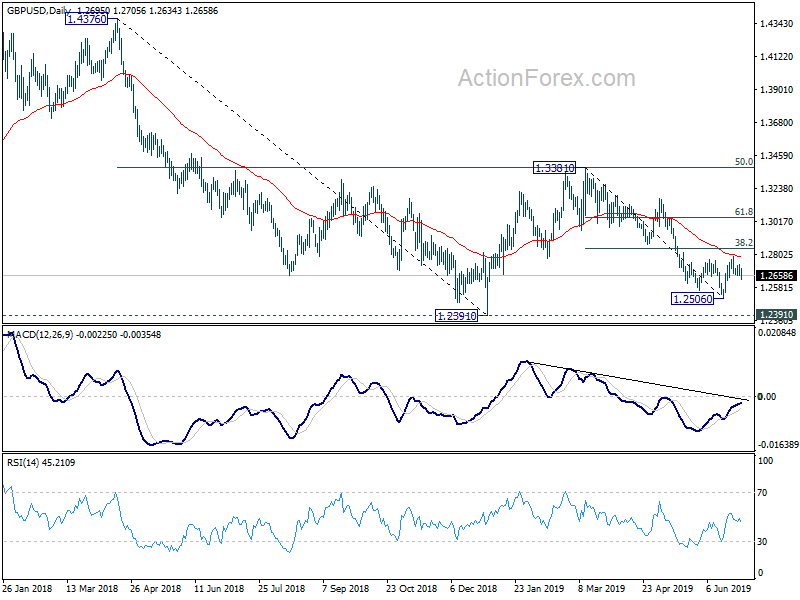

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2662; (P) 1.2699; (R1) 1.2733; More….

GBP/USD breached 1.2642 minor support but quickly recovered. Intraday bias stays neutral first. On the downside, firm break of 1.2642 will confirm completion of corrective rebound from 1.2506. Intraday bias will be turned back to the downside for retesting 1.2506 low. In case of another rise, upside should be limited by 38.2% retracement of 1.3381 to 1.2506 at 1.2840 to complete the corrective rise from 1.2506. However, sustained break of 1.2840 will bring stronger rise to 61.8% retracement at 1.3047 next.

In the bigger picture, down trend from 1.4376 (2018 high) is still in progress. Break of 1.2391 would target a test on 1.1946 long term bottom (2016 low). For now, we don’t expect a firm break there yet. Hence, focus will be on bottoming signal as it approaches 1.1946. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index Jun | 49.4 | 52.7 | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | 7 | 9 | 12 | |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q2 | 7 | 6 | 8 | |

| 23:50 | JPY | Tankan Large Non-Manufacturing Index Q2 | 23 | 20 | 21 | |

| 23:50 | JPY | Tankan Large Non-Manufacturing Outlook Q2 | 17 | 19 | 20 | |

| 23:50 | JPY | Tankan Small Manufacturing Index Q2 | -1 | 2 | 6 | |

| 23:50 | JPY | Tankan Small Manufacturing Outlook Q2 | -5 | -2 | -2 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Index Q2 | 10 | 10 | 12 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Outlook Q2 | 3 | 6 | 5 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 7.40% | 8.10% | 1.20% | |

| 0:30 | JPY | PMI Manufacturing Jun F | 49.3 | 49.5 | ||

| 1:00 | AUD | TD Securities Inflation M/M Jun | 0.00% | 0.00% | ||

| 1:45 | CNY | Caixin PMI Manufacturing Jun | 49.4 | 50.1 | 50.2 | |

| 5:00 | JPY | Consumer Confidence Index Jun | 38.7 | 39.2 | 39.4 | |

| 6:30 | CHF | Retail Sales Real Y/Y May | -1.70% | 0.60% | -0.70% | |

| 7:30 | CHF | PMI Manufacturing Jun | 47.7 | 49 | 48.6 | |

| 7:45 | EUR | Italy Manufacturing PMI Jun | 48.4 | 48.7 | 49.7 | |

| 7:50 | EUR | France Manufacturing PMI Jun F | 51.9 | 52 | 52 | |

| 7:55 | EUR | Germany Manufacturing PMI Jun F | 45 | 45.4 | 45.4 | |

| 7:55 | EUR | German Unemployment Change (000’s) Jun | -1k | 0.0k | 60.0k | |

| 7:55 | EUR | German Unemployment Claims Rate Jun | 5.00% | 5.00% | 5.00% | |

| 8:00 | EUR | Eurozone Manufacturing PMI Jun F | 47.6 | 47.8 | 47.8 | |

| 8:00 | EUR | Eurozone M3 Money Supply Y/Y May | 4.80% | 4.60% | 4.70% | |

| 8:30 | GBP | Mortgage Approvals May | 65.4k | 65.5k | 66.3k | 66.0k |

| 8:30 | GBP | Money Supply M4 M/M May | -0.10% | 0.40% | 0.90% | 0.50% |

| 8:30 | GBP | PMI Manufacturing Jun | 48 | 49.5 | 49.4 | |

| 9:00 | EUR | Eurozone Unemployment Rate May | 7.50% | 7.60% | 7.60% | |

| 13:45 | USD | Manufacturing PMI Jun F | 50.1 | 50.1 | ||

| 14:00 | USD | ISM Manufacturing Jun | 51 | 52.1 | ||

| 14:00 | USD | ISM Prices Paid Jun | 53 | 53.2 | ||

| 14:00 | USD | ISM Employment Jun | 53.7 | |||

| 14:00 | USD | Construction Spending M/M May | 0.10% | 0.00% |