{kind=link}

Risk appetite firms up mildly today as lifted by US Treasury Secretary Steven Mnuchin’s upbeat comments regarding trade negotiation with China. There are also reports that US would delay new tariffs without deadline, to bring China back to negotiation table. However, the positive lift is capped after Trump reiterates his tariff threats to China. Overall, the markets remain cautiously optimistic on the results of the Trump-Xi meeting in Osaka later this week, but also stay on guard.

In the currency markets, New Zealand Dollar remains the strongest one for today, followed by Australian and then Canadian Dollar. Yen and Swiss Franc are the weakest ones on mild risk appetite. Dollar and Euro are mixed. As Dollar recovered since yesterday, after Fed officials dismissed aggressive rate cut in July, Gold is also in retreat, back below 1410.

Technically, USD/CAD is trying to resume recent decline by breaking 1.3151 temporary, as WTI oil is also resuming recent rise. USD/CAD should be targeting 1.3068 support next. EUR/GBP is still pressing 0.8974 resistance and break will resume recent rally for 0.9101 key resistance. While Dollar recovered, it’s still holding below near term resistance against Euro, Sterling, Swiss Franc, Yen and Aussie. More downside remains mildly in favor in the greenback.

In Europe, FTSE is currently up 0.10%. DAX is up 0.37%. CAC is up 0.06%. German 10-year yield is up 0.0088 at -0.32. Earlier in Asia, Nikkei dropped -0.51%. Hong Kong HSI rose 0.13%. China Shanghai SSE dropped -0.19%. Singapore Strait Times dropped -0.09%. Japan 10-year JGB yield rose 0.0062 at -0.145.

Mnuchin hopeful to complete China trade deal year end, but Trump reiterates tariff threats

US Treasury Secretary Steven Mnuchin told CNBC that US-China trade agreement is 90% done. And he’s hopeful to move forward with a plan to complete the deal by the end of the year.

He said “we were about 90% of the way there (with a deal) and I think there’s a path to complete this”. And, “the message we want to hear is that they want to come back to the table and continue because I think there is a good outcome for their economy and the U.S. economy to get balanced trade and to continue to build on this relationship.”

Mnuchin also said “I’m hopeful that we can move forward with a plan … President Trump and President Xi have a very close working relationship. We had a productive meeting at the last G-20.” He’s hopeful a deal could be struck by the end of the year but said “there needs to be the right efforts in place.”

Additionally, Bloomberg reported, quoting unnamed source, that US is preparing to delay imposition of new tariffs, in exchange for China’s agreement to return to negotiation take. And, some advisers went further to push Trump to refrain from setting a hard deadline, to avoid a situation similar to last December’s Trump-Xi summit.

However, Trump insisted that “I would do additional tariffs, very substantial additional tariffs, if that doesn’t work, if we don’t make a deal.” He added “my Plan B with China is to take in billions and billions of dollars a month and we’ll do less and less business with them.”

Also, Commerce Secretary Wilbur Ross said US is “not looking for victory” on trade negotiations. And, the country just want “a sensible deal that addresses the legitimate issues that we have.” Ross pointed out again that “there are some inappropriate activities underway by the Chinese” and warned “they must cease”. He added, “if they do, if we make some redressing of the trade imbalance, then that’s a reasonable deal for both parties.”

US trade deficit widened to USD -74.5B, durable goods orders dropped -1.3%

US advance goods trade deficit widened 5.1% to USD -74.5B in May, up from USD -70.9B. That’s also larger than expectation of USD -71.8B. Exports rose USD 4.1B to USD 1402.B. Meanwhile, imports rose USD 7.8B to USD 214.7B. Durable goods orders dropped -1.3% in May, worse than expectation of -0.1%. But ex-transport orders rose 0.3%, above expectation of 0.1%. Ex-defense order dropped -0.6%.

BoE Saunders: Series of rolling Brexit deadlines have greater adverse affect on growth

BoE Governor Mark Carney noted both PM candidate, former foreign minister Boris Johnson and the current incumbent Jeremy Hunt had indicated that they wanted to reach a deal with EU on Brexit. Carney reiterated that BoE it would not factor in no-deal Brexit into its economic forecasts, unless the government changes its policy. He told the parliament that “in the event that the policy of the government were to switch, the forecast of the Bank of England would switch accordingly. Also, he noted again policy response to no-deal Brexit is not automatic. Nevertheless, it’s more likely for BoE to provide additional monetary accommodation in case of no-deal Brexit, then to tighten.

MPC member Michael Saunders warned that “a series of rolling deadlines would probably imply a heightened uncertainty and have a greater adverse affect on growth.” And, “now that is not a reason to do the things that business fear…, but the outlook for the economy would be very different if you knew now that there was going to be a smooth Brexit compared to one where you have a rolling series of deadlines and at each point there is the risk of a no-deal Brexit.”

German Gfk consumer sentiment dropped to 9.8, economic expectation halted downward spiral

Germany Gfk consumer sentiment for July dropped to 9.8, down from 10.1 and missed expectation of 10.0. On the positive side, Economic Expectation rose from 1.7 to 2.4. Gfk noted that “the downward spiral that economic expectation began at the start of 2018 halted in June, at least for the moment.” Still, “the global economic cooling off, on-going discussions around Brexit, and the trade war with the USA are putting a strain on the economic indicator”.

On the other hand, Income Expectations, which dropped from 57.7 to 45.5, was a major drag. Gfk noted: “the voices heralding the end of the employment boom are growing. As a result, fears concerning job losses have increased at a number of employers”.

RBNZ hints on Aug rate cut, But NZD rebounds on positive references in statement

RBNZ left Official Cash Rate unchanged at 1.50% as widely expected. It also adopted an easing bias by repeatedly saying ” a lower OCR may be needed”. It’s taken by a strong signal that another rate cut is underway in August. However, on the brighter side, RBNZ noted that “GDP growth had held up more than projected” in Q1. And “some of the factors supporting growth in the quarter would continue.” Also, while risks are “tilted to the downside”, resolution of trade tensions “could see uncertainty ease”. New Zealand Dollar spiked lower after the release by quickly rebounded on the positive references.

Some suggested readings:

- RBNZ Review – Stand Pat and Stay Cautions

- Review Of The RBNZ’s June OCR Review: Hinting Strongly

- RBNZ Holds But Keeps Door Open For A Cut In August | GBP/NZD, EUR/NZD

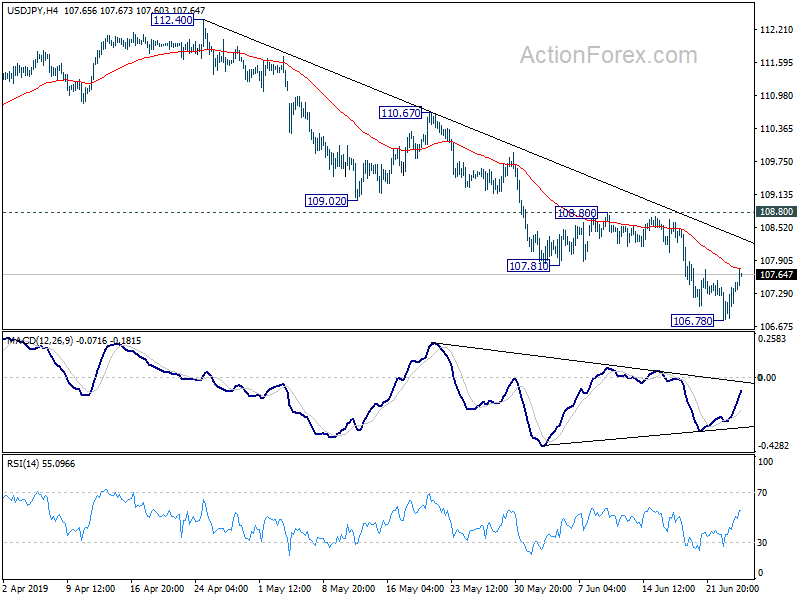

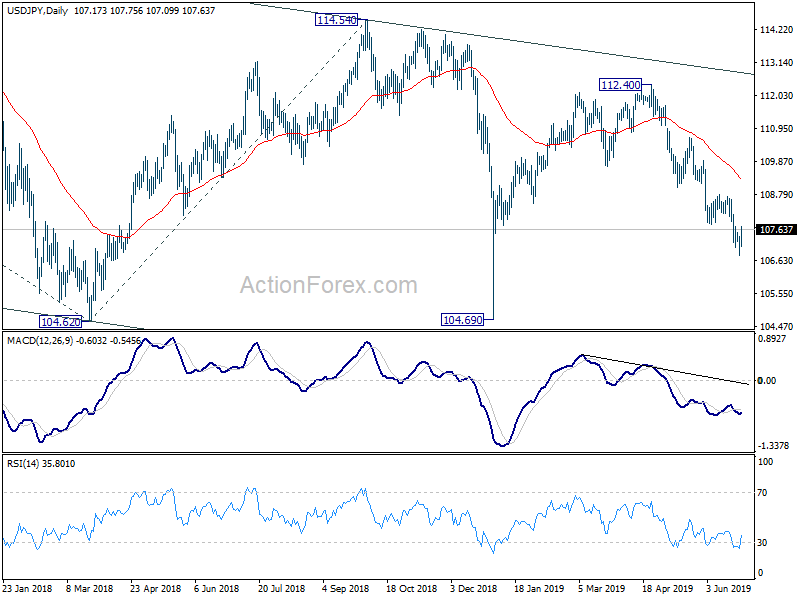

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.82; (P) 107.12; (R1) 107.45; More…

USD/JPY recovers further today but stays well below 108.80 resistance. Intraday bias remains neutral and further decline is still expected. On the downside, break of 106.78 temporary low will resume the fall from 112.40 to retest 104.69 low.

In the bigger picture, decline from 118.65 (Dec 2016) is still in progress, with the pair staying inside long term falling channel. Break of 104.62 will target 100% projection of 118.65 to 104.62 from 114.54 at 100.51. For now, we’d expect strong support above 98.97 (2016 low) to contain downside to bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | NZD | RBNZ Official Cash Rate | 1.50% | 1.50% | 1.50% | |

| 06:00 | EUR | German GfK Consumer Confidence (JUL) | 9.8 | 10 | 10.1 | |

| 08:30 | GBP | BBA Mortgage Approvals May | 42.4K | 43.2K | 43.0K | 42.9K |

| 12:30 | USD | Durable Goods Orders May P | -1.30% | -0.10% | -2.10% | |

| 12:30 | USD | Durables Ex Transportation May P | 0.30% | 0.10% | 0.00% | |

| 12:30 | USD | Advance Goods Trade Balance (USD) May | -74.5B | -71.8B | -72.1B | -70.9B |

| 12:30 | USD | Wholesale Inventories M/M May P | 0.40% | 0.50% | 0.80% | |

| 14:30 | USD | Crude Oil Inventories | -2.7M | -3.1M |