{kind=link}

Surprisingly dovish comments from ECB President Mario Draghi sent Euro sharply lower, and German 10-year yield to new record low today. There are some speculations that ECB could eventually cut interest rates, with a tiered system”, alongside released of new economic projections in July. The comments also send German and French stocks sharply higher. Trump blames in a tweet that Draghi makes it “unfairly easier for them to compete against the USA”. But at the same time, Trump doesn’t comment on positive lift to US stocks, with DOW futures up 150 pts at the time of writing.

Staying in the currency markets, Australian Dollar and Sterling ties for second weakest. Aussie is sold off after RBA minutes confirm that more rate cuts are underway. Sterling is pressured as markets raise their bets on no-deal Brexit on Boris Johnson’s lead in Conservative leadership race. On the other hand, Yen is the strongest one following free fall in major treasury yields. Kiwi and Swiss Franc are the next strongest for now.

Technically, while EUR/USD extends the fall from 1.1347 today, it’s kept well above 1.1107 low. There is no disaster in the pair yet as traders are probably holding their bets before tomorrow’s FOMC rate decision. EUR/GBP is holding above 0.8871 minor support while EUR/AUD is kept above 1.6298 minor support. That is, both crosses remain near term bullish. EUR/JPY is more likely the focus for today and it’s set to take on 120.78 support and break will confirm resumption of recent fall towards 118.62 low.

In Europe, currently, FTSE is up 1.17%. DAX is up 1.48%. CAC is up 1.75%. German 10-year yield is down -0.0796 at -0.322, close to record low at -0.323 (still making new ones). Earlier in Asia, Nikkei dropped -0.72%. Hong Kong HSI rose 1.00%. China Shanghai SSE rose 0.09%. Singapore Strait Times rose 0.96%. Japan 10-year yield dropped -0.0032 to -0.129.

ECB Draghi: Additional stimulus required in absence of improvement in downside risks

ECB President Mario Draghi emphasized in a speech that “monetary policy remains committed to its objective and does not resign itself to too-low inflation… forever or even for now.” Also, he reiterated monetary policy is “patient, persistent and prudent”.

He added: “Patient, because faced with repeated negative shocks we have had to extend the policy horizon. Persistent, because monetary policy will remain sufficiently accommodative to ensure the sustained convergence of inflation to our aim. And prudent, because we will pay close attention to underlying inflation dynamics and to risks and will adjust policy appropriately.”

Draghi also reiterated risks remains “tilted to the downside” and indicators point to “lingering softness”. And he warned, “in the absence of improvement, such that the sustained return of inflation to our aim is threatened, additional stimulus will be required.” The options on further measures were “raised and discussed” at ECB’s last meting.

The measures including enhancing the forward guidance on bias and conditionality. Also, “Further cuts in policy interest rates and mitigating measures to contain any side effects remain part of our tools”. And, “the APP (asset purchase program) still has considerable headroom.”

German ZEW dropped -21.1, substantially worsened German data and increased global uncertainty

German ZEW Economic Sentiment dropped sharply to -21.1 in June, down from -2.1 and missed expectation of -5.8. That’s also the lowest reading since November. Current Situation gauge dropped to 7.8, down from 8.2, beat expectation of 6.1. Eurozone ZEW Economic Sentiment dropped to -20.2, down from -1.6 and missed expectation of -3.6. Eurozone Current Situation gauge rose 3.3 pts to -3.7.

ZEW President Professor Achim Wambach said: “The sharp drop in the ZEW Indicator of Economic Sentiment coincides with an increased uncertainty regarding the future development of the global economy and substantially worsened figures for the German economy at the beginning of the second quarter. The intensification of the conflict between the USA and China, the increased risk of a military conflict in the Middle East and the higher probability of a no-deal Brexit are all casting a shade on the global economic outlook. On top of this, German industry has been reporting worse than expected figures for production, exports and retail sales for April.”

Ifo affirms 2019 Germany growth forecasts, downgrades 2020

Ifo institute maintains 2019 German growth forecast at 0.6%, but revised down 2020 growth forecasts by -0.1% to 1.7%. Private consumer pending is expected to drive the economy, rise 1.4% in 2019 and 1.3% in 2020. Investments are expected to growth 3.0% and 2.8% respectively,d riven by construction. Export is expected to grow just 1.3% in 2019 and normalizes to 3.8% in 2020.

Timo Wollmershaeuser, Head of ifo Economic Forecasts, said “there are increasing signs that industrial weakness is gradually spreading to the domestic economy via the labor market and deep value chains.” And, “that means the German economy will enter the coming year without any momentum.” Wollmershaeuser also warned, “economic policies that attempt to change the globalized economic order through isolation, sanctions, and threats have increased uncertainty worldwide, cooled industrial activity, and caused world trade to collapse.”

Eurozone CPI finalized at 1.2%, core CPI at 0.8% in May

Eurozone CPI was finalized at 1.2% yoy in May, down from April’s 1.7% yoy. CPI core was finalized at 0.8% yoy, unchanged from April’s figure. EU28 CPI was finalized at 1.6% yoy in May, down from April’s 1.9% yoy.

The lowest annual rates were registered in Cyprus (0.2%), Portugal (0.3%) and Greece (0.6%). The highest annual rates were recorded in Romania (4.4%), Hungary (4.0%) and Latvia (3.5%). Compared with April 2019, annual inflation fell in sixteen Member States, remained stable in five and rose in six. The highest contribution to the annual euro area inflation rate came from services (0.47%), followed by energy (0.38%), food, alcohol & tobacco (0.29%) and non-energy industrial goods (0.08%).

Also released, Eurozone trade surplus narrowed to EUR 15.3B in April, below expectation of EUR 16.4B.

RBA Minutes: Further rate cut is more likely than not

RBA cut cash rate by -25bps to 1.25% at the June 4 meeting. Minutes of the meeting noted “members agreed that it was more likely than not that a further easing in monetary policy would be appropriate in the period ahead.”

Policymakers acknowledged that inflation has been below 2-3% target range for three years and even deteriorated to 1.5% in Q1. Unemployment rate had not declined any further in the last six months despite ongoing job growth. It has eve edged up in the most recent two months. Thus, “a lower level of interest rates would support growth in the economy, thereby reducing unemployment and contributing to inflation rising to a level consistent with the target.”

Also, lower interests could support the economy through lower exchange rate, reduced borrowing rates for businesses, and lower interest payments for households. And give the extent of spare capacity in the economy and the subdued inflationary pressures, there was “a low likelihood of a decline in interest rates resulting in an unexpectedly strong pick-up in inflation.”

Instead, lowest interest rates would ” stimulate activity and thereby improve the resilience of the Australian economy to any future adverse shocks.”

Australia house prices dropped -3% in Q1, decline in all capital cities

Australia house price index dropped -3.0% qoq in Q1, much worse than expectation of -2.6%. There’s also deterioration from Q4’s -2.4% qoq. House prices also declined in all capital cities: Sydney (-3.9%), Melbourne (-3.8%), Adelaide (-0.2%) and Hobart (-0.4%), Brisbane (-1.5%), Perth (-1.1%), Canberra (-0.9%) and Darwin (-1.8%).

ABS Chief Economist, Bruce Hockman said: “These results are in line with soft housing market indicators, with sales transactions and auction clearance rates lower than one year ago, and days on market trending higher. A continuation of tight credit supply and reduced demand from investors and owner occupiers has contributed to weakness in property prices in all capital cities this quarter.”

From New Zealand, Westpac consumer confidence dropped -0.3 to 103.5 in Q2.

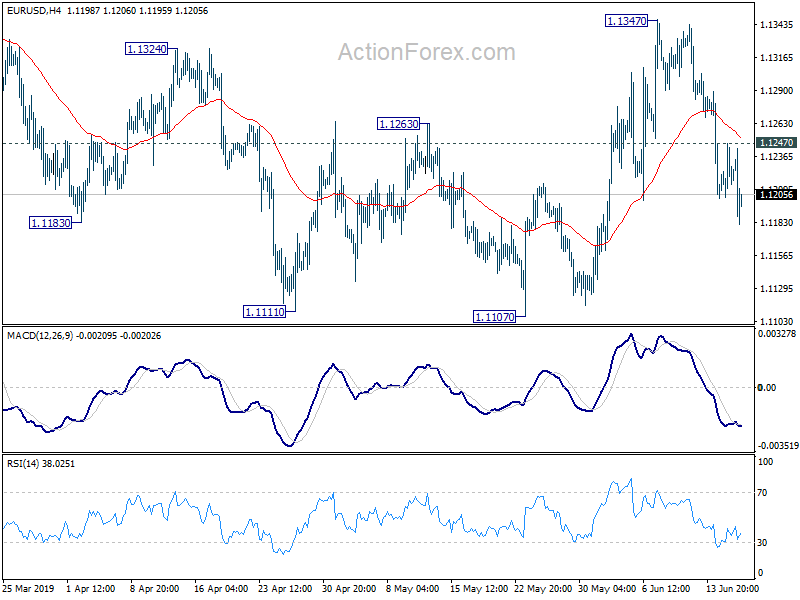

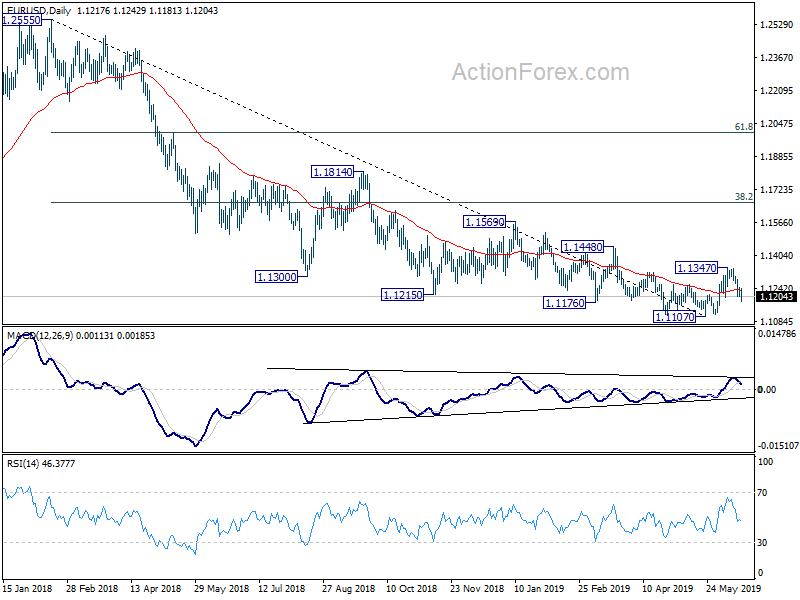

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1198; (P) 1.1222; (R1) 1.1242; More……

EUR/USD’s fall from 1.1347 extends to as low as 1.1181 so far today. Intraday bias remains on the downside for 1.1107 low. Though, we’d stay cautious on strong support from 1.1107 low to bring rebound. On the upside, above 1.1247 minor resistance will turn bias back to the upside for 1.1347 again.

In the bigger picture, considering bullish convergence condition in daily and weekly MACD, a medium term bottom could be in place at 1.1107 after hitting 61.8% retracement of 1.0339 (2016 low) to 1.2555 (2018 high) at 1.1186. Hence, for now, risk will stay on the upside as long as 1.1107 low holds. Break of 1.12347 will extend the rebound towards 38.2% retracement of 1.2555 to 1.1107 at 1.1660. However, sustained break of 1.1107 will confirm resumption of down trend from 1.2555.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | Westpac Consumer Confidence Q2 | 103.5 | 103.8 | ||

| 01:30 | AUD | House Price Index Q/Q Q1 | -3.00% | -2.60% | -2.40% | |

| 01:30 | AUD | RBA Minutes Jun | ||||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | 15.3B | 16.4B | 17.9B | |

| 09:00 | EUR | Eurozone CPI M/M May F | 0.10% | 0.20% | 0.70% | |

| 09:00 | EUR | Eurozone CPI Y/Y May F | 1.20% | 1.20% | 1.70% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 0.80% | 0.80% | 0.80% | |

| 09:00 | EUR | German ZEW Economic Sentimen Jun | -21.1 | -5.8 | -2.1 | |

| 09:00 | EUR | German ZEW Current Situation Jun | 7.8 | 6.1 | 8.2 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jun | -20.2 | -3.6 | -1.6 | |

| 12:30 | CAD | Manufacturing Sales M/M Apr | -0.60% | 0.40% | 2.10% | 2.60% |

| 12:30 | USD | Housing Starts May | 1.27M | 1.24M | 1.24M | 1.28M |

| 12:30 | USD | Building Permits May | 1.29M | 1.30M | 1.29M | 1.29M |