{kind=link}

Sterling recovers broadly today as lifted by stronger than expected wage growth. A key BoE official also noted that interest rate might have to rise more quickly than market expected. Though, upside of the Pound is capped so far, by Brexit uncertainty and worries over slowdown if such uncertainty is not resolved soon. Euro is also firm as second strongest, shrugging off poor Sentix Investor confidence which indicates Eurozone is on the verge of recession. On the other hand, New Zealand Dollar is the weakest one for today. Yen and Swiss Franc are pressured by return of risk appetite.

In other markets, DOW open higher again and is currently up 0.48%. 10-year yield is up 0.012 at 2.155. In Europe, FTSE is up 0.55%. DAX is up 1.43%. CAC is up 0.86%. German 10-year yield is down -0.0159 at -0.232. Earlier in Asia, Nikkei rose 0.33%. Hong Kong HSI rose 0.76%. China Shanghai SSE rose 2.58%. Singapore Strait Times rose 0.67%. Japan 10-year JGB yield rose 0.0109 to -0.11.

Released in US, PPI rose 0.1% mom 1.8% yoy in May, versus expectation of 0.1% mom, 1.9% yoy. PPI core rose 0.2% mom, 2.3% yoy versus expectation of 0.2% mom, 2.3% yoy.

UK unemployment rate stayed at 44-year low, wage growth accelerates

UK unemployment rate remained unchanged at 3.8% in the three months to April. It’s the lowest reading since December 1974. Average weekly earnings, including bonus, rose 3.1% yoy, slowed from 3.3% yoy but beat expectation of 3.0% yoy. Average weekly earnings, excluding bonus, rose 3.4% yoy, accelerated from 3.3% yoy and beat expectation of 3.1% yoy.

BoE Broadbent: Interest rates could have to rise a little more than markets expect

BoE Deputy Governor Ben Broadbent reiterated that Brexit is the major risk to growth in inflation outlook in a Treasury Select Committee hearing. He noted: “The outlook for both growth and inflation will depend significantly on the nature and timing of EU withdrawal, in particular: the new trading arrangements between the EU and the UK; whether the transition to them is abrupt or smooth; how households, businesses and financial markets respond; and the balance of these effects on demand, supply and the exchange rate.”

Broadbent also pointed out the May Inflation Report was conditioned to market path of Bank Rate rising only 25bps over the three-year forecast horizon. But “were the economy to develop in line with our projection, and taking as given other asset prices in the forecast, interest rates would probably have to rise by a little more than what was in the curve at the time of the forecast.”

Policymaker Michael Saunders warned “no-deal Brexit would probably have a significant adverse effect on the UK’s long term growth prospects, because of reduced openness to international trade in both goods and services, and the resultant deterioration in the attractiveness of the UK as a global business location.”

Saunders also noted “The major external risk is that the ongoing trade tensions could escalate further, with successive rounds of retaliation, hence undermining business confidence and growth on a wide scale. The UK, as a highly globalized economy, would suffer through various channels including effects on exports, investment and asset prices.”

EU reiterates no Brexit renegotiation even with new UK PM

European Commission reiterates its stance that there will be renegotiation of the Brexit deal even with a new UK Prime Minister. The Commission’s spokesman said today, “Everybody knows what is on the table. What is on the table has been approved by all member states and the election of a new prime minister will not change the parameters.”

The stance is echoed by both Germany and France. France’s state secretary for European affairs Amélie de Montchalin said “We consider it is up to Britain to decide how it wants to proceed. The exit agreement was not negotiated against the British; negotiators on both sides tried, painstakingly, to find the best solution for all concerned.” Also, without a “new political line” in the UK or a second referendum, Britain must expect to leave the bloc on 31 October.

Germany’s Europe Minister Michael Roth said “I see no willingness to restart negotiations from the beginning. The candidates would do well to bear that in mind in the course of their internal party campaigns.”

Sentix: Eurozone on threshold of recession, Trump shoots himself in the knee

Eurozone Sentix Investor Confidence dropped to -3.3 in June, down from 5.3 and missed expectation of 2.5. Current Situation Index dropped from 11.0 to 6.0. Expectations index dropped from -0.3 to -12.3.

Sentix noted that “renewed escalation in the US-China trade dispute is also having a considerable impact on the Euro zone economy”. Also, it warned “the Euroland economy is once again on the threshold of recession”. Sentix also complained that “more than ever, the economic forecast becomes a short-winded Twitter analysis.”

The Overall Investor Confidence Index for Germany tumbled from 7.9 to -0.7, lowest since March 2010. Current situation Index dropped from 18.3 to 13.5. Expectations Index dropped from -2.0 to -14.0. Germany’s key industry, the automotive industry, is still “in a crisis of its own making”. And the “current government coalition’s inability to act does not contribute to stabilization.”

For US, Overall Investor Confidence Index dropped from 17.7 to 6.5, lowest since February 2016. Current Situation Index dropped from 43.3 to 31.8, lowest since October 2016. Expectations Index dropped from -5.3 to -16.0. Sentix warned that Trump could “underestimate how much he is currently threatening to shoot himself in the knee with his trade rhetoric”. The US economy is “currently experiencing a real emergency stop.”

ECB Rehn: Should developments require ECB would use forward guidance, cut rates or even relaunch QE

ECB Governing Council member Olli Rehn said “in case of a further weakening of economic activity and a materialization of adverse contingencies, the Governing Council is determined to act and stands ready to adjust all of its instruments, as appropriate”.

To be more specific, “the Governing Council may, should economic developments so require, strengthen its forward guidance and its linkage to the achievement of the price stability objective, lower the monetary policy rates and introduce possible mitigating measures, and/or relaunch net purchases under the securities purchase program.

Australia business condition dropped as private sectors continue to lose momentum

Australian NAB Business Condition dropped again in May to 1, down from 3. Private sector continues to lose momentum. Goods distribution industries remain particularly weak, and manufacturing is not far behind. Business Confidence jumped from 0 to 7, in a post-election spike, as well as on RBA rate cut expectations. However, forward looking indicators suggest more weakness lies ahead.

Alan Oster, NAB Group Chief Economist noted “business confidence saw a sharp increase in the month following the Federal election and a confirmation from the RBA that rates would be cut in June. We think this will be a short-term spike given other forward-looking indicators saw further deterioration in the month. Forward orders declined further and in addition to being well below average are negative. Capacity utilisation has also pulled back in 2019 to date and is now a touch below average”.

“While confidence, at least at face value was a positive outcome, business conditions deteriorated further. Trading conditions and profits are particularly weak. The employment index which we are watching closely, partially reversed some of its decline last month, but is only around average”.

China refuses to confirm Trump-Xi summit at G20

China’s Foreign Ministry spokesman Geng Shuang refused to confirm if there will be a Trump-Xi meeting at G20 in Osaka later this month. Instead, he just reiterated that stance that “China does not want to fight a trade war, but we are not afraid of fighting a trade war”. Also, “if the United States only wants to escalate trade frictions, we will resolutely respond and fight to the end.”

Yesterday, Trump said he and Chinese President Xi are “scheduled to have a meeting” at the G20 summit in Osaka. He then threatened, “We’re expected to meet and if we do that’s fine, and if we don’t — look, from our standpoint the best deal we can have is 25% on $600 billion.”

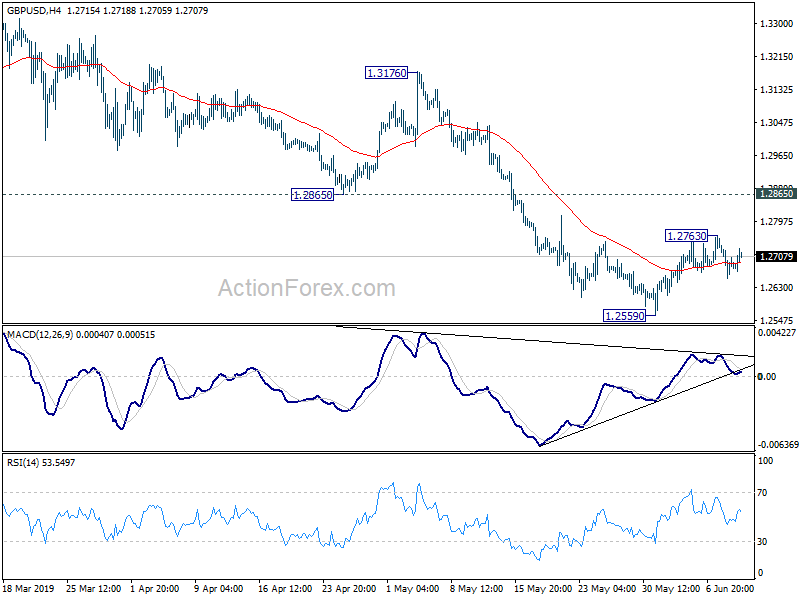

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2639; (P) 1.2699; (R1) 1.2746; More….

Intraday bias in GBP/USD is turned neutral again with today’s recovery. Break of 1.2763 will extend the corrective rise fro 1.2559. But in that case, upside should be limited by by 1.2865 support turned resistance to bring fall resumption eventually. On the downside, break of 1.2559 low will extend the decline from 1.3381 for 1.2391 low first.

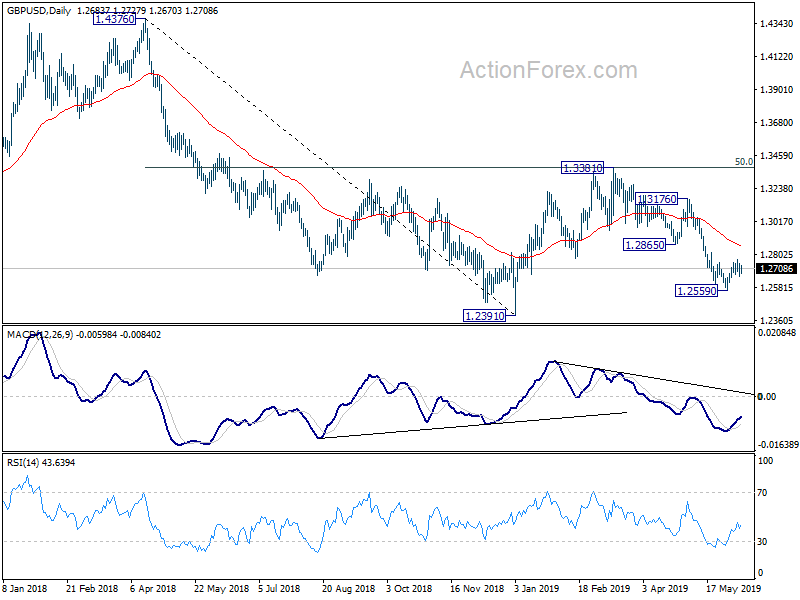

In the bigger picture, medium term decline from 1.4376 (2018 high) is possibly ready to resume. Decisive break of 1.2391 would target a test on 1.1946 long term bottom (2016 low). For now, we don’t expect a firm break there yet. Hence focus will be on bottoming signal as it approaches 1.1946. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | NAB Business Conditions May | 1 | 3 | ||

| 01:30 | AUD | NAB Business Confidence May | 7 | 0 | ||

| 06:00 | JPY | Machine Tool Orders Y/Y May P | -27.30% | -33.40% | ||

| 08:30 | GBP | Jobless Claims Change May | 23.2K | 12.3K | 24.7K | 19.1K |

| 08:30 | GBP | Claimant Count Rate May | 3.10% | 3.00% | ||

| 08:30 | GBP | Average Weekly Earnings 3M Y/Y Apr | 3.10% | 3.00% | 3.20% | 3.30% |

| 08:30 | GBP | Weekly Earnings ex Bonus 3M Y/Y Apr | 3.40% | 3.10% | 3.30% | |

| 08:30 | GBP | ILO Unemployment Rate 3Mths Apr | 3.80% | 3.80% | 3.80% | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jun | -3.3 | 2.5 | 5.3 | |

| 10:00 | USD | NFIB Small Business Optimism May | 105 | 101.9 | 103.5 | |

| 12:30 | USD | PPI M/M May | 0.10% | 0.10% | 0.20% | |

| 12:30 | USD | PPI Y/Y May | 1.80% | 1.90% | 2.20% | |

| 12:30 | USD | PPI Core M/M May | 0.20% | 0.20% | 0.10% | |

| 12:30 | USD | PPI Core Y/Y May | 2.30% | 2.30% | 2.40% |