{kind=link}

Global markets are back is heavy risk-off mode today as US-China tensions keep on escalating. Words from both sides suggest that neither one is going to back down from the current stance and there is no chance of returning to the table any time soon. More importantly, it’s seems that neither US or China is worried about the escalations.

On the Chines side, Commerce Ministry spokesman Gao Feng warned: “If the United States wants to continue trade talks, they should show sincerity and correct their wrong actions. Negotiations can only continue on the basis of equality and mutual respect… We will closely monitor relevant developments and prepare necessary responses.” Foreign Ministry spokesman Lu Kang said “relevant U.S. actions obviously do not create a good atmosphere or environment for consultations.

On the US side, Secretary of State Mike Pompeo said he’s been “explaining the risks” regarding Huawei about national security as he travels around the world. And he criticized that “for them (Huawei) to say that they don’t work with the Chinese government is false.” He added, “If you’re a state-directed business and you take on subsidies direct from the Chinese government, there’s no doubt you can make real hay.”

Additionally, sentiments are weighed down by poor economic data from Eurozone. Most importantly, both German Ifo Business Climate and PMIs suggested that slowdown in German manufacturing factor is quickly spreading over to services. Meanwhile, risks of no-deal Brexit is increasing. There are rumors flying around regarding the exit date of UK Prime Minister Theresa May. While she may stay till Trump’s visit in early June, her position won’t last long.

In the currency markets, Yen and Swiss Franc remain the strongest one on risk aversion, followed by Dollar. Canadian Dollar is the weakest one for today, followed oil prices lower. Euro is the second weakest on it’s down economy challenges.

Technically, with today’s decline, EUR/JPY is eyeing 122.08 temporary low. EUR/USD is accelerating and could take out 1.1111 bottom to resume larger down trend soon. Given the weak sentiments, AUD/USD will likely follow through 0.6864 temporary low too.

In Europe, currently, FTSE is down -1.34%. DAX is down -1.58%. CAC is down -1.63%. German 10-year yield is down -0.019 at -0.103, back below -0.1 handle. Earlier in Asia, Nikkei dropped -0.62%. Hong Kong HSI dropped -1.58%. China Shanghai SSE dropped -1.36%. Singapore Strait Times dropped -0.70%. Japan 10-year JGB yield dropped -0.0104 at -0.061.

IMF: New US-China tariffs will subtract about 0.3% of global GDP in short term

In blog post published today, IMF noted that US-China trade tensions have “negatively affected consumers as well as many producers in both countries.” It pointed out while tariffs have reduced trade between the two countries, “bilateral trade deficit remains broadly unchanged”. It also warned that “latest escalation could significantly dent business and financial market sentiment, disrupt global supply chains, and jeopardize the projected recovery in global growth in 2019.”

In the global level, recently announced measures and envisaged new US-China tariffs will “subtract about 0.3 percent of global GDP in the short term, with half stemming from business and market confidence effects.” Furthermore, ” failure to resolve trade differences and further escalation in other areas, such as the auto industry, which would cover several countries, could further dent business and financial market sentiment, negatively impact emerging market bond spreads and currencies, and slow investment and trade.”

In addition, “higher trade barriers would disrupt global supply chains and slow the spread of new technologies, ultimately lowering global productivity and welfare. More import restrictions would also make tradable consumer goods less affordable, harming low-income households disproportionately.”

US initial jobless claims dropped slightly to 211k, below expectations

US initial jobless claims dropped -1k to 211k in the week ending May 18, below expectation of 215k. Four-week moving average of initial claims dropped -4.75k to 220.25k. Continuing claims rose 12k to 1.676M in the week ending May 11. Four-week moving average of continuing claims rose 5.5k to 1.674M.

ECB minutes: Less confidence in baseline growth scenario, range of possibilities widened

Minutes of ECB’s April 9-10 meeting showed that policy makers were getting less confident on Eurozone recovery. The minutes noted “it was acknowledged that some recent data had turned out even weaker than expected”. And, “there was now somewhat less confidence in the baseline scenario and that the range of other possible outcomes had widened.”

Also, “the global outlook remained subject to the continued risk of an escalation of trade conflicts and the uncertainty surrounding the withdrawal of the United Kingdom from the EU.”

Regarding the new TLTROs, “some arguments were put forward in favor of pricing the new operations so they would primarily serve as a backstop, providing insurance in times of elevated uncertainty.” Also, “other arguments supported the view that the TLTRO-III operations should be seen as a potential tool for adjusting the monetary policy stance.”

German Ifo Business climate dropped to 97.9, deterioration spreading to services

In May, Germany Ifo Business Climate dropped to 97.9, down from 99.2 and missed expectation of 99.1. Current Assessment index dropped to 100.6, down from 103.3 and missed expectation of 103.5. Expectations Index rose to 95.3, up from 95.2 and beat expectation of 95.0.

Ifo President Clemens Fuest said “the German economy is still lacking in momentum.” Manufacturing index dropped “slightly” but expectations rose for the first time since September 2018. However, Also, “in the services, the business climate took a substantial hit. Not since April 2013 has the indicator of current sentiment fallen as far as it did this month. Optimism with regard to the coming months also declined.”

Eurozone PMIs suggests just 0.2% GDP growth in Q2, renewed deterioration in optimism

In May, Eurozone PMI manufacturing dropped to 47.7, down from 47.9 and missed expectation of 48.1. PMI services dropped to 52.5, down from 52.8 and missed expectation of 53.0. PMI Composite rose to 51.6, slightly up from 51.5. Markit noted that “the weak reading puts growth in the second quarter so far on a par with the lacklustre gain seen in the first quarter and is among the lowest recorded since mid-2013.”

Chris Williamson, Chief Business Economist at IHS Markit said: “The eurozone economy remained becalmed in the doldrums in May, adding to signs that only modest growth will be achieved in the second quarter. At current levels the PMI is so far indicating GDP growth of only 0.2% in the second quarter.”

Also, “A renewed deterioration in optimism about the year ahead suggests that the business situation could deteriorate further in coming months. Worries reflected concerns over lower economic growth forecasts, signs of weaker sales and rising geopolitical uncertainty, with escalating trade wars and auto sector woes commonly cited as specific causes for concern…

“While some encouragement can be gained from the manufacturing sector showing signs of its downturn having bottomed out in March, the concern is that the slowdown is spreading to the service sector, where new business growth has slipped to one of the weakest seen since 2014.”

Germany PMI manufacturing dropped to 44.3, down from 44.4 and missed expectation of 44.8. It’s the second weakest reading in nearly seven years. PMI services dropped to 55.0, down from 55.7 and missed expectation of 55.4. PMI Composite rose to 52.4, up from 52.2. Germany GDP was finalized at 0.4% qoq in Q1, unrevised

France PMI manufacturing rose to 50.6, up from 50.0, and beat expectation of 50.0. That’s also a 3-month high. PMI services rose to 51.7, up from 50.0, beat expectation of 50.8. it’s a 6-month high. PMI composite rose to 51.3, up from 50.1, a 6-month high.

Japan PMI manufacturing dropped to 49.6, re-escalation of US-China trade frictions heightened concern

Japan PMI manufacturing dropped to 49.6 in May, down from 50.2 and missed expectation of 50.5. The reading is also back in contraction territory. Markit noted that output and new orders decrease for fifth successive month. Businesses cast pessimistic outlook towards the coming year for the first time in six-and-a-half year.

Joe Hayes, Economist at IHS Markit, said: “Following some tentative signs that the downturn in Japan’s manufacturing sector had softened in April, flash data for May revealed these were short-lived, as output and export orders fell at stronger rates. The re-escalation of US-China trade frictions has heightened concern among Japanese goods producers.

” Underlying growth weakness across much of Asia led to struggling exports, which fell at the sharpest rate in four months. Difficulties on the international front merely add to uncertainties domestically, with upcoming upper house elections in July, and the impending sales tax hike later this year. Subsequently, sentiment turned negative in May for the first time in six-and-a-half years.”

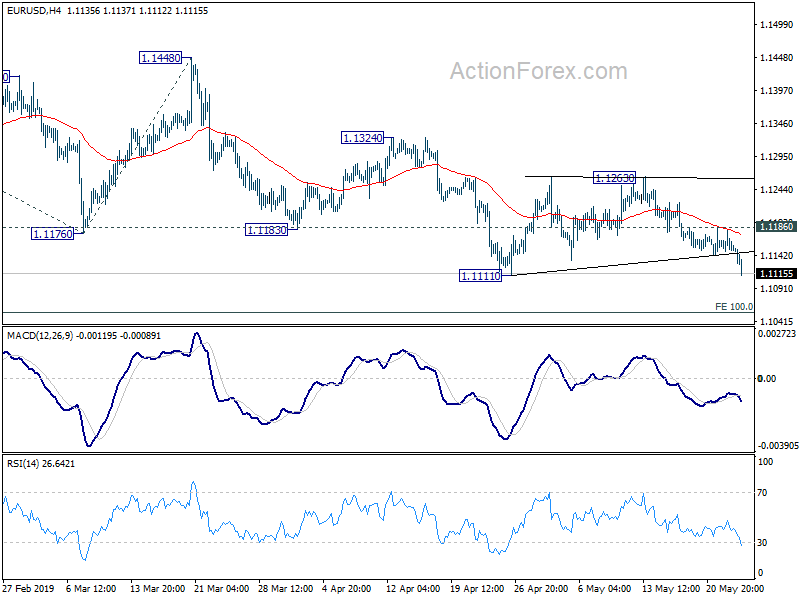

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1138; (P) 1.1159; (R1) 1.1171; More…..

EUR/USD’s selloff gathers momentum again today and focus is immediately on 1.1111 low. Decisive break there will resume larger down trend from 1.2555. Next target will be 100% projection of 1.1448 to 1.1183 from 1.1324 at 1.1059. Nevertheless, on the upside, above 1.1186 minor resistance will delay the bearish case and bring another recovery to extend the consolidation from 1.1111 first.

In the bigger picture, down trend from 1.2555 (2018 high) is still in progress. Such decline would target 78.6% retracement of 1.0339 (2016 low) to 1.2555 (2018 high) at 1.0813 next. Sustained break there will pave the way to retest 1.0339. On the upside, break of 1.1448 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | PMI Manufacturing May P | 49.6 | 50.5 | 50.2 | |

| 06:00 | EUR | German GDP Q/Q Q1 F | 0.40% | 0.40% | 0.40% | |

| 07:15 | EUR | France Manufacturing PMI May P | 50.6 | 50 | 50 | |

| 07:15 | EUR | France Services PMI May P | 51.7 | 50.8 | 50.5 | |

| 07:30 | EUR | Germany Manufacturing PMI May P | 44.3 | 44.8 | 44.4 | |

| 07:30 | EUR | Germany Services PMI May P | 55 | 55.4 | 55.7 | |

| 08:00 | EUR | Eurozone Manufacturing PMI May P | 47.7 | 48.1 | 47.9 | |

| 08:00 | EUR | Eurozone Services PMI May P | 52.5 | 53 | 52.8 | |

| 08:00 | EUR | German IFO Business Climate May | 97.9 | 99.1 | 99.2 | |

| 08:00 | EUR | German IFO Expectations May | 95.3 | 95 | 95.2 | |

| 08:00 | EUR | German IFO Current Assessment May | 100.6 | 103.5 | 103.3 | |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | CAD | Wholesale Trade Sales M/M Mar | 1.40% | 0.80% | 0.30% | 0.20% |

| 12:30 | USD | Initial Jobless Claims (MAY 18) | 211K | 215K | 212K | |

| 13:45 | USD | Manufacturing PMI May P | 52.7 | 52.6 | ||

| 13:45 | USD | Services PMI May P | 53.5 | 53 | ||

| 14:00 | USD | New Home Sales Apr | 678K | 692K | ||

| 14:00 | USD | New Home Sales M/M Apr | -2.50% | 4.50% | ||

| 14:30 | USD | Natural Gas Storage | 106B |