{kind=link}

Direction isn’t very clear in the financial markets today as they’re generally in consolidative mode. Sterling was lifted briefly overnight by UK Prime Minister Theresa May’s new Brexit plan. But it was quickly back to square one after the plan was overwhelmingly rejected by MPs. For now, Canadian Dollar is so far the strongest one for the week but it has yet to break out from recent range against Dollar. Australia Dollar had a roller-coaster ride but stays above 0.6864 temporary low against Dollar. Yen pulled back mildly this week but there is no follow through selling, except versus Dollar. Though, the greenback also struggles to extend gains against Euro.

Stocks are also in consolidation mode on trade war concerns. The move to suspend Huawei ban gave sentiments a brief lift only. After all, there is no sign of a breakthrough in trade talks and we’re not expecting Trump nor Xi to back down on their stance. Despite yesterday’s near 200pts recovery, DOW is staying below 55 day EMA while keep risks on the downside. China Shanghai SSE is also flip-flopping around 2900 handle.

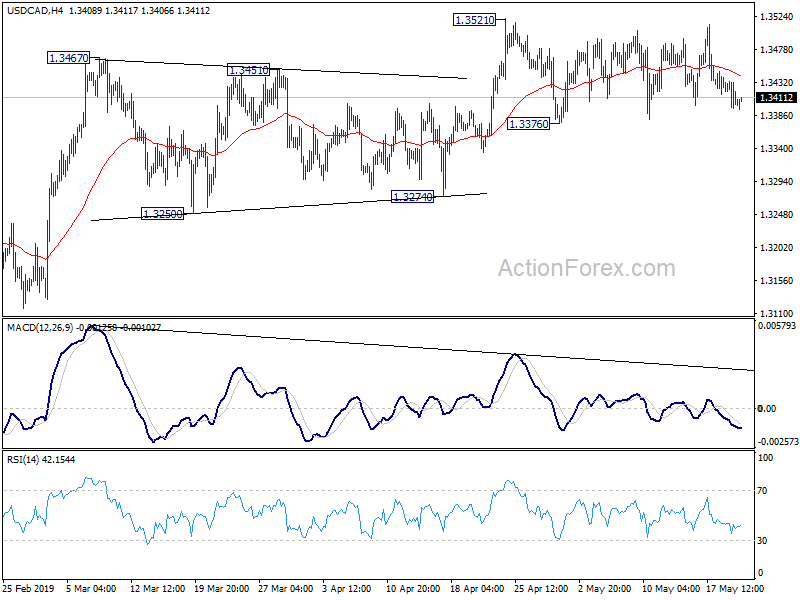

Technically, after yesterday’s brief spike, focus is back on 1.2685 temporary low in GBP/USD and 0.8789 temporary top in EUR/GBP. Break will resume recent selloff in Sterling. AUD/USD is still eyeing 0.6864 temporary low for decline resumption. A focus today is on whether Canadian retail sales can push USD/CAD outlook of range of 1.3376/3521.

In Asia, currently, Nikkei is up 0.12%. Hong Kong HSI is up 0.17%. China Shanghai SSE is down -0.43%. Singapore Strait Times is up 0.22%. Japan 10-year JGB yield is down -0.0053 at -0.05. Overnight, DOW rose 0.77%. S&P 500 rose 0.85%. NASDAQ rose 1.08%. 10-year yield rose 0.010 to 2.426.

40% US manufacturers moving out of China on trade war, only 6% back to US

American Chamber of Commerce in Shanghai and China carried a joint survey on the impact of US-China tariffs. Results showed that the negative impact of tariffs is clear and hurting the competitiveness of American companies in China. 74.9% os respondents said the tariffs hikes are having a negative impact to their business. Among them, manufacturers suffered most with 81.5% for US tariffs and 85.2% for Chinese tariffs. Impacts include lower demand (52.1%), higher manufacturing costs (42.4%) and higher sales prices (38.2%).

Also, companies are increasingly adopting an “In China, for China” strategy (35.3%), or delaying and canceling investment decisions (33.2%). However, 40.7% are considering or have relocated manufacturing facilities outside China. For those moving, Southeast Asia (24.7%) and Mexico (10.5%) are the top destinations. Only 6% said they’re relocating back to the US.

On non-tariff measures, 20.1% said there were “increased inspections” in China, and “slower customs clearance (19.7%). 14.2% said there was ” slower license approvals and 14.2% said there were increased regulatory scrutiny. But 53.1% said there was no increase in non-tariff retaliatory measures by the Chinese government.

Fed Rosengren: No clear need to alter slightly accommodative interest rates

Boston Fed President Eric Rosengren said in a speech that “today, the two elements of the Fed’s mandate are sending opposing signals for monetary policy”. That is, low unemployment suggests “a bit tighter policy” while low inflation “the opposite”. But there is “no clarion call” to alter current policy in near term. He viewed current policy as “slightly accommodative” consistent with lifting inflation back to target over time. He added “the Fed can afford to wait to see if that forecast does indeed materialize.”

On the economy, Rosengren is relatively optimistic and he expects unemployment rate to fall further. He noted that the significant decline in equity markets in Q4 has largely recovered. Worries over Brexit and China slowdown “appear to have subsided since the beginning of the year”. Also, Q1 growth in US was “stronger than many forecasters expected”.

On trade, he said “I am optimistically assuming that both sides in the trade negotiations will work to reach an agreement”. And, “I am also assuming that while the uncertainty is not helpful, it will be transitory, and thus have only a modest effect on the forecast for the U.S. economy overall.”

May’s new Brexit plan received terrible responses

Sterling was lifted briefly by UK Prime Minister Theresa May’s “new” Brexit plan. But recovery in Pound quickly faded as the plan was terribly received by MPs across the House. In short, under the new 10-point plan, the most important part is guaranteeing a vote on whether to call a second referendum on the Brexit deal. However, the pre-condition for the vote on referendum is the passage of the Brexit deal itself in the Commons.

Labour leader Jeremy Corbyn was quick to reject the proposal as “largely a rehash” and pledged “we won’t back a repackaged version of the same old deal”. Former foreign minister Boris Johnson and ex Brexit minister Dominic Raab said they’d oppose the deal. Pro-Brexit Cabinet ministers including Michael Gove, Andrea Leadsom and Chris Grayling opposed the idea of a “free vote”. Northern Ireland’s Democratic Unionist Party was concerned that “fatal flaws” of the original Brexit deal remained, which could split Northern Ireland with the rest of UK.

Despite the desperate final gamble, there is still practically no chance for May to get her Brexit deal through Commons in the June. A fourth humiliating defeat is more likely than not.

BoJ Harada: If weak economy deteriorates, should strengthen easing without delay

BoJ dove Yutaka Harada said today that “the economy has been weak recently, and the same can be said about prices”. Also, “there’s a risk the current sluggishness observed in prices will spill over to inflation expectations, further delaying a pick-up in inflation.” In addition, “the impact of the consumption tax hike scheduled for October this year also is a concern.”

Harada warned “if the economy deteriorates to the extent that achieving our price target in the long-term becomes difficult, it’s necessary to strengthen monetary easing without delay.” He also dismiss claims that the ultra-loose monetary policy hurts banks’ profits. He said “the deterioration of banks’ profitability is actually caused by a structural problem, which is that they are accumulating deposits despite a lack of borrowers.”

Released from Japan, trade surplus narrowed to JPY 60.4B in April. Exports dropped -2.4% yoy while imports rose 6.4% yoy. In seasonally adjusted terms, trade deficit narrowed to JPY -110.9B.Exports rose 0.6% while imports dropped -0.1%. Machine orders rose 3.8% mom in March, above expectation of 0.0% yoy.

Also released, New Zealand retail sales rose 0.7% qoq in Q1 versus expectation of 0.6% qoq. Core retail sales rose 0.7% qoq versus expectation of 0.9% qoq. Austalia Westpac leading index dropped -0.1% mom in April. Construction work done dropped sharply by -1.9% in Q1.

Looking ahead

UK inflation data will be the main focus in European session, with CPI, PPI and house price index featrued. Public sector net borrowing will also be be featured. Later in the day, Canada retail sales will be a focus and let’s see if it can trigger a range breakout in USD/CAD. FOMC minutes will also be a focus. Fed Chair Jerome Powell talked down the chance of a rate cut after last meeting. Recent comments from Fed officials also suggest that there is no case for a cut yet. The minutes will likely echo these views.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3385; (P) 1.3414; (R1) 1.3433; More…

USD/CAD is staying in consolidation from 1.3521 and intraday bias remains neutral first. Such consolidation could extend with deeper fall. But downside should be contained above 1.3274 support to bring rally resumption. On the upside, firm break of 1.3521 will resume the whole rise from 1.3068 to retest 1.3664 high. However, decisive break of 1.3274 support will indicate completion of rise from 1.3068 and turn outlook bearish.

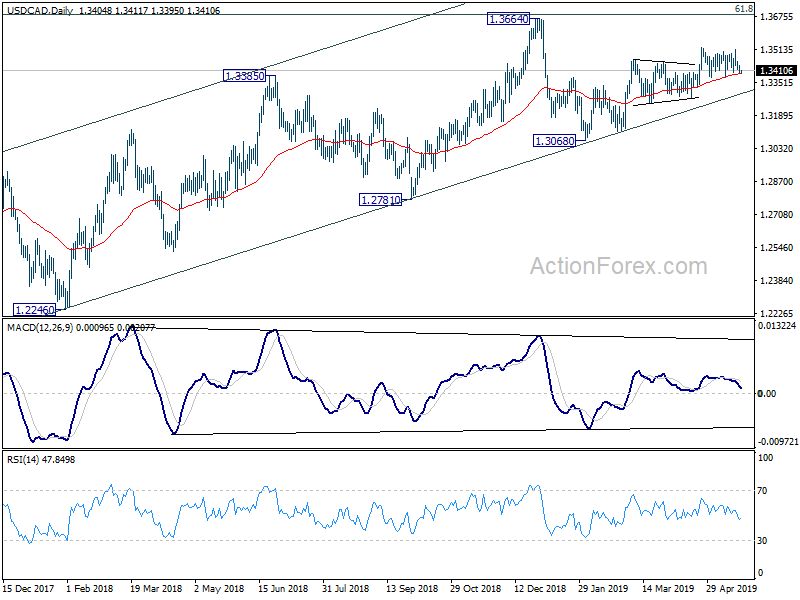

In the bigger picture, USD/CAD is staying well inside medium term rising channel (support at 1.3296). Thus, the up trend from 1.2061 (2017 low) should be in progress. On the upside, decisive break of 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 will pave the way to 78.6% retracement at 1.4127 next. This will remain the favored case as long as 1.3068 support holds. However, sustained break the channel support will be the first sign of medium term reversal. Firm break of 1.3068 would confirm.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Ex Inflation Q/Q Q1 | 0.70% | 0.60% | 1.70% | |

| 22:45 | NZD | Retail Sales Core Q/Q Q1 | 0.70% | 0.90% | 2.00% | |

| 23:50 | JPY | Trade Balance (JPY) Apr | -0.11T | -0.12T | -0.18T | |

| 23:50 | JPY | Machine Orders M/M Mar | 3.80% | 0.00% | 1.80% | |

| 00:30 | AUD | Westpac Leading Index M/M Apr | -0.10% | 0.20% | 0.30% | |

| 01:30 | AUD | Construction Work Done Q1 | -1.90% | 0.00% | -3.10% | -2.10% |

| 08:30 | GBP | CPI M/M Apr | 0.70% | 0.20% | ||

| 08:30 | GBP | CPI Y/Y Apr | 2.20% | 1.90% | ||

| 08:30 | GBP | Core CPI Y/Y Apr | 1.90% | 1.80% | ||

| 08:30 | GBP | RPI M/M Apr | 0.90% | 0.00% | ||

| 08:30 | GBP | RPI Y/Y Apr | 2.80% | 2.40% | ||

| 08:30 | GBP | PPI Input M/M Apr | 1.20% | -0.20% | ||

| 08:30 | GBP | PPI Input Y/Y Apr | 4.40% | 3.70% | ||

| 08:30 | GBP | PPI Output M/M Apr | 0.30% | 0.30% | ||

| 08:30 | GBP | PPI Output Y/Y Apr | 2.30% | 2.40% | ||

| 08:30 | GBP | PPI Output Core M/M Apr | 0.20% | 0.00% | ||

| 08:30 | GBP | PPI Output Core Y/Y Apr | 2.20% | 2.20% | ||

| 08:30 | GBP | House Price Index Y/Y Mar | 1.00% | 0.60% | ||

| 08:30 | GBP | Public Sector Net Borrowing (GBP) Apr | 5.1b | 0.8b | ||

| 12:30 | CAD | Retail Sales M/M Mar | 1.00% | 0.80% | ||

| 12:30 | CAD | Retail Sales Ex Auto M/M Mar | 0.80% | 0.60% | ||

| 14:30 | USD | Crude Oil Inventories | 5.4M | |||

| 18:00 | USD | FOMC Minutes May |