{kind=link}

Worries over Italy’s budget takes center stage today. Italy 10-year yield hit as high as 2.812. On the other hand, German 10-year yield dived to as low as -0.131. US 10-year yield is also dragged down to as low as 2.364 so far. These are clearly signs of risk aversion even though stock market losses are limited for the moment. In the back, poor Chinese data also indicates that slowdown is resuming after a brief seasonal rebound in March. Weaker than expected US retail sales add to the concerns of investors in general.

In the currency markets, Yen and Swiss Franc are back as the strongest ones for today, thanks to falling treasury yields in Germany and US. Dollar is following as third strongly, mainly thanks to weakness elsewhere. Sterling suffers renewed selling in early US session and is now the weakest one. Australian and New Zealand Dollar follow as next weakest.

Technically, EUR/JPY and GBP/JPY resumed recent decline today by taking out 122.48 and 141.20 temporary lows. More decline is expected head. USD/JPY is holding above 109.02 temporary low for now, but could easily be dragged down by other Yen crosses. AUD/USD is extending recent fall with focus on 0.6913 fibonacci projection level. Decisive break there, with downside acceleration, will solidify the case for larger down trend resumption. GBP/USD’s break of 1.2865 support should confirm near term reversal for 1.2391 low again. USD/CAD is staying in range as Canadian CPI was largely stable.

In Europe, currently, FTSE is up 0.04%. DAX is down -0.93%. CAC is down -0.66%. German 10-year yield is down -0.051 at -0.0118. Italian 10-year yield is up 0.024 at 2.758. Earlier in Asia, Nikkei rose 0.58%. Hong Kong HSI rose 0.52%. China Shanghai SSE rose 1.91%. Singapore Strait Times dropped -0.15%. Japan 10-year JGB yield rose 0.001 to -0.05.

German-Italian yield spread widens on renewed Italy concerns

German-Italian yield spread widens sharply again today on fear of expansionary budget again in Italy and renewed risk of showdown with EU. The trigger was Italian Deputy Prime Minister Matteo Salvini’s pledge yesterday, to be prepared to let budget deficit rise above EU limits if it were to boost employment.

Salvini doubled down today and said that “If there are European rules that are starving a continent, these rules must be changed”. On current market reactions to his comments, he said he’s “absolutely not worried”, because “Italians’ right to a job, life and health comes first.”

German GDP grew 0.4% in Q1 on domestic resilience, first ray of hope but uncertainty remains

Germany GDP grew 0.4% qoq in Q1, matched market expectation. That was also a significant improve over Q4’s 0.0% growth. The quarter-on-quarter comparison (price-, seasonally and calendar-adjusted) shows that positive contributions mainly came from domestic demand.

Fixed capital formation in construction and in machinery and equipment increased considerably. Household final consumption expenditure, too, increased substantially. However, government final consumption expenditure recorded a decline. And there were mixed signals regarding foreign trade; as both exports and imports increased.

Economy Minister Peter Altmaier said the growth figures were a “first ray of hope” following two quarters without expansion. However, he warned that ” international trade disputes are still unresolved”. He urged , “we must do everything possible to find acceptable solutions that enable free trade”.

Eurozone GDP grew 0.4% in Q1, employment grew 0.3%

Eurozone GDP grew 0.4% qoq in Q1, matched expectations. EU 28 GDP grew 0.5% qoq. Over the year, Eurozone GDP rose 1.2% yoy while EU28 GDP grew 1.5% yoy. Employment grew 0.3% qoq in Q1, above expectation of 0.2% qoq. EU 28 employment all grew 0.3% qoq.

US retail sales dropped -0.2%, ex-auto sales rose 0.1%, both missed expectations

In April, US headline retail sales dropped -0.2%, missed expectation of 0.2% mom rise. Ex-auto sales rose merely 0.1% mom, much lower than expectation of 0.7% mom. Industrial production dropped -0.4% versus expectation of 0.0%. Empires State manufacturing index rose to 17.8 in May, up from 10.1 and beat expectation 8.0.

Canada CPI climbed to 2.0%, matched market expectations

In April, Canada CPI accelerated to 2.0% yoy, up from 1.9%, matched expectations. CPI core commons was unchanged at 1.8%, matched expectations. CPI core median slowed to 1.9% yoy, missed expectation of 2.0% yoy. CPI core trim slowed to 2.0% yoy, missed expectation of 2.1% yoy.

China retail sales growth slowed to lowest since 2003, industrial production and fixed asset investment missed too

China industrial production growth slowed to 5.4% yoy in April, missed expectation of 6.5% yoy. That’s also sharp deterioration from 4-year high of 8.5% yoy in March. Fixed-asset investment growth slowed to 6.1% ytd yoy, down from 6.3% and missed expectation of 6.4%.

More seriously, retail sales growth slowed to 7.2% yoy, down from 8.7% yoy and missed expectation of 7.2% yoy. That’s also the lowest growth since May 2003. That dents hope of shifting the burden of the economy from exports to domestic demand growth. Unemployment rate, though, dropped to 5.2%.

More on China: China’s Slowdown Resumes as Seasonal Effects Faded

Aussie drops after wage price miss, consumer sentiment barely rose

Australia, Wage Price Index rose only 0.5% qoq in Q1, below expectation of 0.6% qoq. Westpac Consumer Sentiment rose 0.3% to 101.3 in May, up from 100.7.

Westpac also noted that easing bias was delivered by RBA at last week’s meeting, with growth and inflation forecasts lowered to “barely acceptable” levels. More importantly, such forecasts are based on market pricing for a full rate cut for. Westpac maintained that the tensions between strong labor market and weak GDP will be resolved over the next few months. And the case of August RBA cut would become clear.

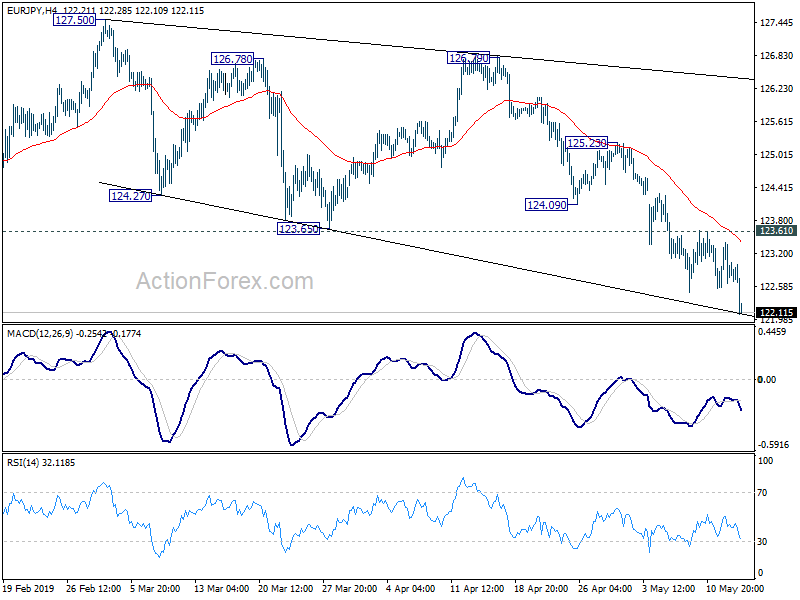

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 122.48; (P) 122.95; (R1) 123.32; More….

EUR/JPY’s decline resumed after brief consolidation and reaches as low as 122.08 so far. Intraday bias is back on the downside. Current fall from 127.50 should extend to retest 118.62 low. On the upside, break of 123.61 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, current development argues that rebound from 118.62 is merely a correction and has completed at 127.50. EUR/JPY is staying in long term falling channel from 137.49 (2018 high). Decisive break of 118.62 will confirm resumption of this medium term fall and target 109.20 low. For now, this will be the favored case as long as 125.23 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Apr | 2.60% | 2.30% | 2.40% | |

| 00:30 | AUD | Westpac Consumer Confidence May | 0.60% | 1.90% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q1 | 0.50% | 0.60% | 0.50% | |

| 02:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Apr | 6.10% | 6.40% | 6.30% | |

| 02:00 | CNY | Industrial Production Y/Y Apr | 5.40% | 6.50% | 8.50% | |

| 02:00 | CNY | Retail Sales Y/Y Apr | 7.20% | 8.60% | 8.70% | |

| 02:00 | CNY | Surveyed Jobless Rate Apr | 5.00% | 5.20% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Q1 Apr P | -33.40% | -28.50% | ||

| 06:00 | EUR | German GDP Q/Q Q1 P | 0.40% | 0.40% | 0.00% | |

| 09:00 | EUR | Eurozone Employment Q/Q Q1 P | 0.30% | 0.20% | 0.30% | |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.40% | 0.40% | 0.40% | |

| 12:30 | CAD | CPI M/M Apr | 0.40% | 0.40% | 0.70% | |

| 12:30 | CAD | CPI Y/Y Apr | 2.00% | 2.00% | 1.90% | |

| 12:30 | CAD | CPI Core – Common Y/Y Apr | 1.80% | 1.80% | 1.80% | |

| 12:30 | CAD | CPI Core – Median Y/Y Apr | 1.90% | 2.00% | 2.00% | |

| 12:30 | CAD | CPI Core – Trim Y/Y Apr | 2.00% | 2.10% | 2.10% | |

| 12:30 | USD | Empire State Manufacturing May | 17.8 | 8 | 10.1 | |

| 12:30 | USD | Retail Sales Advance M/M Apr | -0.20% | 0.20% | 1.60% | 1.70% |

| 12:30 | USD | Retail Sales Ex Auto M/M Apr | 0.10% | 0.70% | 1.20% | 1.30% |

| 13:15 | USD | Industrial Production M/M Apr | -0.50% | 0.00% | -0.10% | 0.20% |

| 13:15 | USD | Capacity Utilization Apr | 77.90% | 78.70% | 78.80% | 78.50% |

| 14:00 | USD | NAHB Housing Market Index May | 64 | 63 | ||

| 14:00 | USD | Business Inventories Mar | 0.00% | 0.30% | ||

| 14:30 | USD | Crude Oil Inventories | 0.0M | -4.0M |