{kind=link}

Imminent threat of full blown US-China trade war is the dominant theme in the global financial markets today. Chinese stocks were hardest hit, down the most in more than three years. Other Asian markets were generally down while Japan continued to enjoy its ultra-long 10-day holiday. European markets are also broadly pressured. Declines somewhat slowed after refrained response from China.

In the currency markets, Yen and Dollar remain the strongest one for today. At this point, Euro is the third strongest, with help from better than expected investor sentiment data and rebound in EUR/GBP. On the other hand, the Pound is the weakest one, paring some of last week strong gains. It’s strength was built on optimism of a Brexit deal between Conservative and Labour. But they’re have to deliver to solidify Sterling’s strength. New Zealand and Australian Dollars are the next weakest, awaiting possible rate cut by respective central banks later in the week.

Technically, for now, the rally in Yen and Dollar somewhat halted after initial response to trade war news. Yen crosses and commodity currencies are staying generally vulnerable. EUR/JPY is pressing 123.39 key support and sustained break will confirm near term bearish reversal. Break of 144.80 minor support in GBP/JPY will bring deeper fall to key support at 143.72, and break there will also confirm bearish reversal. AUD/USD resumed recent decline from 0.7295 and focus will turn to tomorrow’s RBA rate decision. A rate cut, or even a hints on rate cut, could send AUD/USD further lower.

In Europe, FTSE is on holiday. DAX is down -1.85%. CAC is down -1.93%. German 10-year yield is down -0.0162 at 0.012, staying positive. Earlier in Asia, Hong Kong HSI dropped -2.90%. China Shanghai SSE dropped -5.58%. Singapore Strait Times dropped -3.00%. Japan remains in 10-day holiday.

Trump blames China for USD 500B loss in trade every year, to escalate trade war

Trump continues his pressure on China with new tweet in the morning. He played victim again and said the US has been losing, “for many years”, USD 600 to 800B a year on Trade. And “with China we lose 500 Billion Dollars”. He added “sorry, we’re not going to be doing that anymore!”

Yesterday, Trump decided to escalate US-China trade war to full-blown level, instead of pushing for a long awaited agreement this week. In short, , Trump announced to raise the 10% tariffs on the USD 200B of “other goods” to 25%. Additionally, currently “untaxed” USD 325B will be tariffed at rate of 25%. That’s not a warning as White House Economic Adviser Larry Kudlow guessed, as there was not conditions attached. Trump’s tweet was simply an announcement.

Chinese trade delegation still preparing to travel to US, but no indication on timeline

In wake of Trump’s new tariff threats, Chinese Foreign Ministry spokesman Geng Shuang said a Chinese delegation was still preparing to travel to the US for another round of trade negotiations. However, there was no indication on the date of the trip, nor whether Vice Premier Liu He will lead the team.

Geng said in a press briefing that “we are now trying to get more information on the relevant situation.” And, “what I can tell you is that the Chinese team is preparing to travel to the U.S. for trade talks.”

“What is of vital importance is that we still hope the United States can work hard with China to meet each other half way, and strive to reach a mutually beneficial, win-win agreement on the basis of mutual respect,” Geng added.

Eurozone Sentix investor confidence rose to 5.3, recession risk averted

Eurozone Sentix Investor Confidence rose to 5.3 in May, up from -0.3 and beat expectation of 1.1. Current Situation index rose from 3.8 to 11.0. Expectations index rose from -4.3 to -0.3, highest since March 2018. Sentix noted that the danger o recession in Eurozone is “averted”. Global environment made a “significant contribution” to the positive development. Danger of unregulated Brexit has been averted until at least October. It also said the forthcoming elections in Europe will “take place in a relaxing economic environment”.

For Germany, Overall index rose to 7.9, up from 2.1, and hit the highest since November 2018. Current situation index rose from 10.5 to 18.3. Expectations index rose from -6.0 to -2.0, highest since February 2018. Sentix noted that the spark from the Chinese economy, which has recovered significantly since the start of the year, is “increasingly jumping over to the export-dependent German economy”.

Eurozone PMI composite finalized at 51.5, suggests around 0.2% GDP growth in Q2

Eurozone PMI services was finalized at 52.8 in April, up from March reading of 53.3. Eurozone PMI composite was revised up to 51.5, down from March reading at 51.6. Looking at the members states, Italy PMI composite dropped to 49.5, 3-month low. Improvements were seen in France and Germany, as PMI composites hit 50.1 and 52.2 respectively, both at 3 month high.

Chris Williamson, Chief Business Economist at IHS Markit said the final PMIs are ” indicative of the economy growing at a quarterly rate of approximately 0.2%, but manufacturing remained mired in its steepest downturn since 2013 and service sector growth slipped lower.”

Also released, retail sales rose 0.0% mom in March versus expectation of -0.1% mom. Australia TD Securities inflation rose 0.2% mom in April. China Caixin PMI services rose 0.1 to 54.5 in April, above expectation of 54.2.

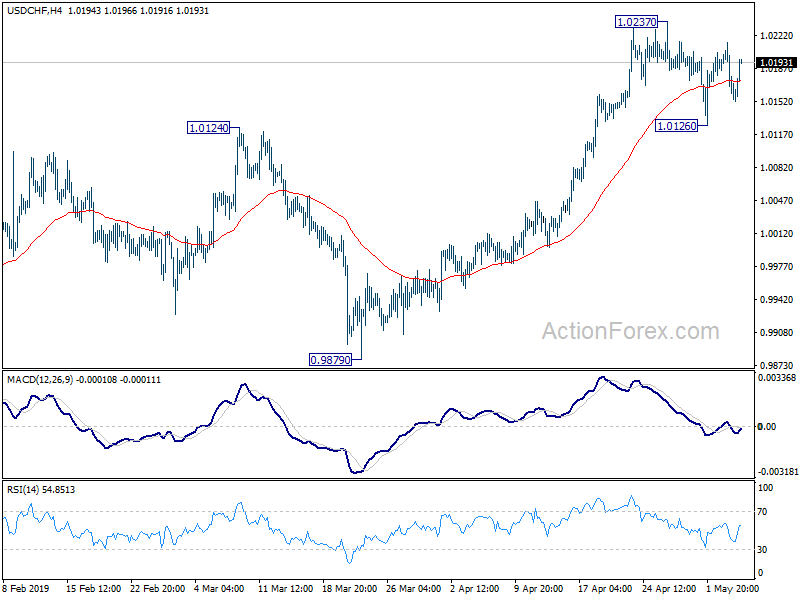

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0145; (P) 1.0180; (R1) 1.0200; More…..

USD/CHF rebounds notably today but stays in range below 1.0237. Intraday bias remains neutral first and more consolidation could still be see. On the upside, break of 1.0237 will resume larger rise from 0.9186 to 1.0342 key resistance. However, break of 1.0126 will turn bias to the downside for deeper decline to 55 day EMA (now at 1.0066).

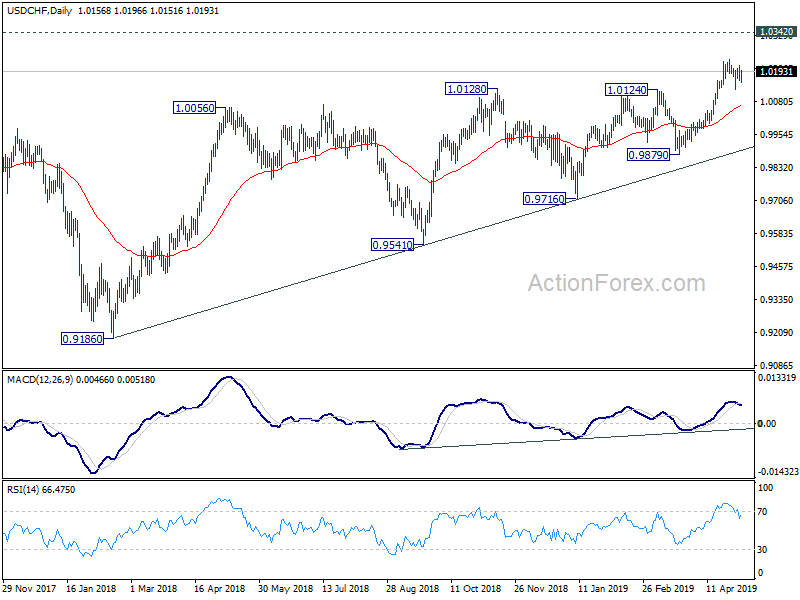

In the bigger picture, medium term up trend from 0.9186 is extending. Current rise should target 1.0342 resistance next. For now, we’d be cautious on strong resistance from there to limit upside, until we see medium term upside acceleration. On the downside, break of 0.9879 support is needed to indicate reversal. Otherwise, outlook will stay bullish in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:00 | AUD | TD Securities Inflation M/M Apr | 0.20% | 0.40% | ||

| 1:45 | CNY | Caixin China PMI Services Apr | 54.5 | 54.2 | 54.4 | |

| 7:45 | EUR | Italy Services PMI Apr | 50.4 | 54.4 | 53.1 | |

| 7:50 | EUR | France Services PMI Apr F | 50.5 | 50.5 | 50.5 | |

| 7:55 | EUR | Germany Services PMI Apr F | 55.7 | 55.6 | 55.6 | |

| 8:00 | EUR | Eurozone Services PMI Apr F | 52.8 | 52.5 | 52.5 | |

| 8:30 | EUR | Eurozone Sentix Investor Confidence May | 5.3 | 1.1 | -0.3 | |

| 9:00 | EUR | Eurozone Retail Sales M/M Mar | 0.00% | -0.10% | 0.40% | 0.50% |