{kind=link}

The forex markets are in slow motion today. Major pairs and crosses are bounded inside yesterday’s range, with no follow through movement yet. BoE Super Thursday is a high profile event, but triggers no sustainable price actions yet. It’s rather hard to react to BoE’s new economic projections. Growth forecasts were revised up but inflation forecasts were revised down. Most importantly, BoE painted a much slower rate path and a full 25bps hike in Q4 2021. Meanwhile, there is no follow through buying in Dollar after the short rally yesterday, as Fed Chair Jerome Powell indicated there is no urgency to shift interest rate in either direction.

Technically, 1.1175 minor support is a focus in EUR/USD and break will indicator completion of recent rebound. Dollar could ride on decline in EUR/USD and rally elsewhere. In particular, AUD/USD’s recovery from 0.6988 could have completed ahead of 0.7081 resistance. Break of 0.6988 will resumer larger decline from 0.7295. Sterling is lowing some upside momentum against Dollar, Euro and Yen, even though more upside is mildly in favor.

In Europe, FTSE is currently down -0.22%. DAX is up 0.11%. CAC is down -0.45%. German 10-year yield is down -0.005 at 0.011, staying positive. Earlier in Asia, Hong Kong HSI rose 0.83%. China Shanghai SSE rose 0.52%. Singapore Strait Times dropped -0.20%. Japan remained in ultra-long 10-day holiday.

US initial jobless claims unchanged at 230k, above expectations

US initial jobless claims was unchanged at 230k in the week ending April 27, above expectation of 220k. Four-week moving average of initial claims rose 6.5k to 212.5k. Continuing claims rose 17k to 1.671m in the week ending April 20. Four-week moving average of continuing claims dropped -13.75k to 1.674m.

Also released, non-farm productivity rose 3.6% in Q1, much higher than expectation of 1.2%. Unit labor cost dropped -0.9%, much lower than expectation of 2.1%.

BoE projects slower rate hike, faster growth, lower inflation

BoE left Bank Rate unchanged at 0.75% and kept asset purchase target at GBP 435B, on unanimous vote, as widely expected. New economic projections were released with the Quarterly Inflation Report too. One important point to note is that new forecasts are based on slower projected rate path. That is, Bank Rate is projected to rise to 0.9% in 2021 Q2, down from February’s projection of 1.1%. In 2022, Q2, Bank Rate is forecast at 1.0%.

Under the slower rate path, growth is projected to be faster from 2019 to 2011. Inflation is projected to be slower in both 2019 and 2020. On growth, BoE forecast annual GDP growth to be: 1.5% in 2019 (revised up from 1.2%); 1.6% in 2020 (revised up from 1.5%); 2.1% in 2011, (revised up from 1.9%). On Inflation, BoE forecast CPI to be at: 1.6% in Q4 2019 (revised down from 2.0%); 2.0% in Q4 2020 (revised down from 2.1%); 2.1% in Q4 2021 (unchanged).

Again, BoE reiterated: “The economic outlook will continue to depend significantly on the nature and timing of EU withdrawal, in particular: the new trading arrangements between the European Union and the United Kingdom; whether the transition to them is abrupt or smooth; and how households, businesses and financial markets respond. The appropriate path of monetary policy will depend on the balance of these effects on demand, supply and the exchange rate. The monetary policy response to Brexit, whatever form it takes, will not be automatic and could be in either direction.”

UK PMI construction rose to 50.5, return to growth

UK PMI construction rose to 50.5 in April, up from 49.7 and beat expectation of 50.5. Markit noted that construction output rises for the first time since January. Residential work expands at fastest pace for four months. However, civil engineering and commercial activity fall again.

Tim Moore, Associate Director at IHS Markit said: “A return to growth would normally be considered a positive month for the UK construction sector, but the weakness outside of house building gives more than a little pause for thought…. The forward-looking survey indicators remain subdued… A lack of new work has started to impact on staff recruitment, as signalled by a reduction in payroll numbers for the first time since July 2016. This provides another signal that construction firms are bracing for an extended period of soft demand ahead.”

Eurozone PMI manufacturing finalized at 47.9, remained deep in decline, downturn fiercest in Germany,

Eurozone PMI manufacturing was finalized at 47.9, revised up from 47.8. It was just a slight improvement from March’s six-year low of 47.5. Also, it’s in contraction region below 50 for three consecutive months. Markit noted there were further marked fall in new orders recorded. Also, Germany continues to lead downturn but Greece expands at fastest rate in nearly 19 years.

Looking at the member states, German’s reading was revised down to 44.4, a two month high but remained close to March’s 80-month low at 44.1. Italy and Austria stayed in contraction at 49.1 and 49.2 respectively. France reading was revised up to 50.0, indicating flat activity. Greece reading, though, rose to 226-mont high at 56.6.

Chris Williamson, Chief Business Economist at IHS Markit said: “The manufacturing sector remained deep in decline at the start of the second quarter…. The survey’s output index is indicative of factory production falling at a quarterly rate of approximately 1%… The downturn remains the fiercest in Germany, with Italy and Austria also in decline and France stagnating. Spain’s expansion remains only modest.”

Also released, German retail sales dropped -0.2% mom in March, versus expectation of -0.5% mom. Swiss retail sales dropped -0.7% yoy in March versus expectation of -0.4% yoy. Swiss PMI manufacturing dropped to 48.5 in April, down from 50.3 and missed expectation of 51.0.

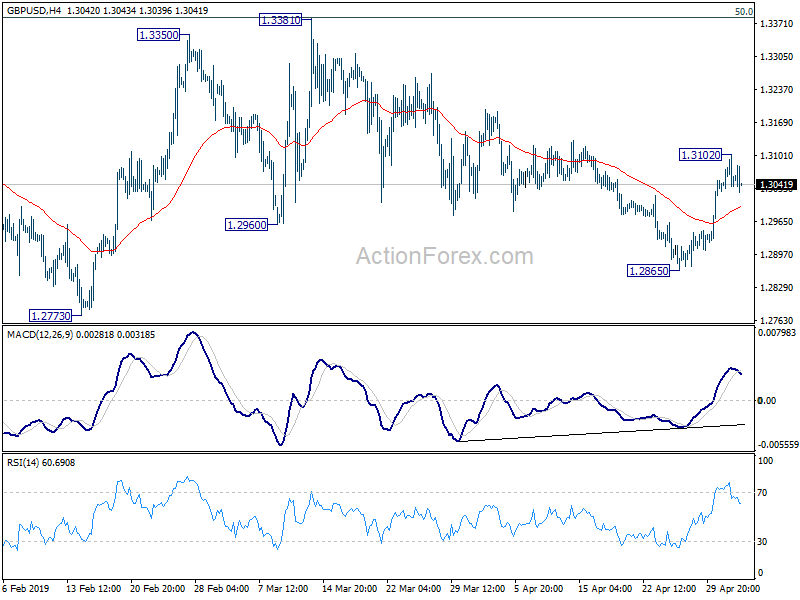

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3018; (P) 1.3060; (R1) 1.3093; More….

With 4 hour MACD crossed below signal line, a temporary top is in place at 1.3102 in GBP/USD and intraday bias is turned neutral first. Current development suggests that corrective pull back from 1.3381 has completed at 1.2865. Hence, another rise is mildly in favor. On the upside, above 1.3102 will target 1.3381 resistance first. Break will resume whole rebound from 1.2391. On the downside, though, break of 1.2865 will target 1.2773 key support instead.

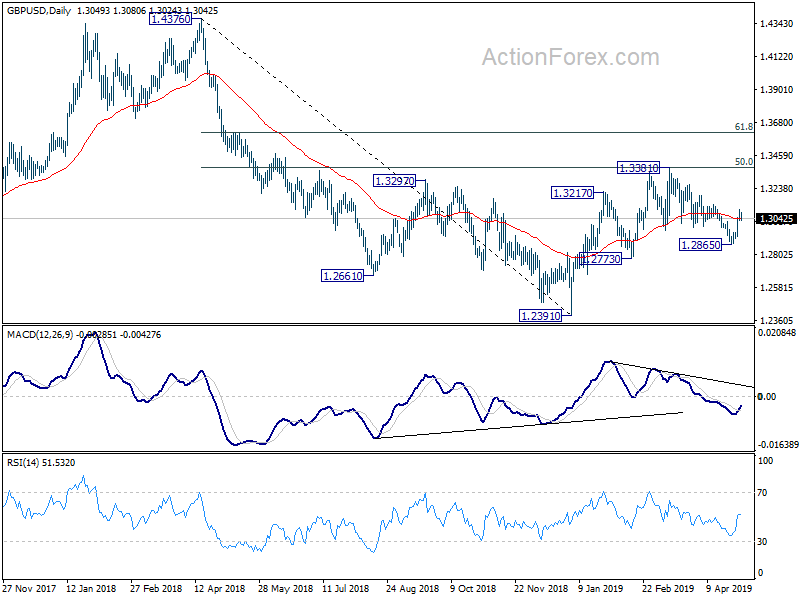

In the bigger picture, medium term decline from 1.4376 (2018 high) halted after hitting 1.2391. The structure of the rebound from 1.2391 suggests that it’s a corrective move. In case of another rise, strong resistance could be seen around 61.8% retracement of 1.4376 to 1.2391 at 1.3618 to limit upside. On the downside, break of 1.2773 support will suggests that such corrective rise is completed and bring retest of 1.2391 low first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Mar | -6.90% | 1.90% | 1.70% | |

| 06:00 | EUR | German Retail Sales M/M Mar | -0.20% | -0.50% | 0.90% | 0.50% |

| 06:30 | CHF | Retail Sales Real Y/Y Mar | -0.70% | -0.40% | -0.20% | |

| 07:30 | CHF | PMI Manufacturing Apr | 48.5 | 51 | 50.3 | |

| 07:45 | EUR | Italy Manufacturing PMI Apr | 49.1 | 47.7 | 47.4 | |

| 07:50 | EUR | France Manufacturing PMI Apr F | 50 | 49.6 | 49.6 | |

| 07:55 | EUR | Germany Manufacturing PMI Apr F | 44.4 | 44.5 | 44.5 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | 47.9 | 47.8 | 47.8 | |

| 08:30 | GBP | Construction PMI Apr | 50.5 | 50.3 | 49.7 | |

| 11:00 | GBP | BoE Rate Decision | 0.75% | 0.75% | 0.75% | |

| 11:00 | GBP | BoE Asset Purchase Target May | 435B | 435B | 435B | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | 10.90% | 0.40% | ||

| 12:30 | USD | Initial Jobless Claims (APR 27) | 230K | 220K | 230K | |

| 12:30 | USD | Nonfarm Productivity Q1 P | 3.60% | 1.20% | 1.90% | 1.30% |

| 12:30 | USD | Unit Labor Costs Q1 P | -0.90% | 2.10% | 2.00% | 2.50% |

| 14:00 | USD | Factory Orders Mar | 1.40% | -0.50% | ||

| 14:30 | USD | Natural Gas Storage | 107B | 92B |