{kind=link}

Fears of global recession intensify after shockingly poor German manufacturing data. Major European indices are all trading in red while DOW is down more than 100 pts at initial trading. More importantly, German 10-year bund yield turns negative for the first time since 2016. The most accurate indicator of US recession, 3-month to 10-year US yield curve, inverts, as 10-year yield drops through 2.5 handle. Risk aversion will likely be a major theme before weekly close.

In the currency markets, Euro is the weakest one today as selloff accelerates after German data. Canadian Dollar is the second weakest, suffering some pressure after poor retail sales data. Swiss Franc is the third weakest, as dragged down by Euro. Yen is the strongest one today so far on risk aversion naturally. Sterling is the second strongest for today, as supported by the two extra week of Brexit lifeline granted by EU. Dollar is the third strongest, mainly thanks to weakness elsewhere.

In Europe, FTSE is down -1.26%. DAX is down -0.81%. CAC is down -1.34%. German 10-year bund yield is down -0.050 at -0.006. It hit as high as 1.2 just earlier this week. Earlier in Asia, Nikkei rose 0.09%. Hong Kong HSI rose 0.14%. Singapore Strait Times dropped -0.05%. Japan 10-year JGB yield dropped -0.037 to -0.072.

Eurozone PMI manufacturing dropped to 47.6, 71-month low with sharp contraction in trade flows

In March, Eurozone PMI manufacturing dropped to 47.6, down from 49.3 and missed expectation of 49.5. That’s also the lowest level in 71 months. PMI services dropped slightly to 52.7, down from 52.8, matched expectations. PMI composite dropped to 51.3, down from 51.9.

Chris Williamson, Chief Business Economist at IHS Markit said: “The survey indicates that GDP likely rose by a modest 0.2% in the opening quarter, with a decline in manufacturing output in the region of 0.5% being offset by an expansion of service sector output of approximately 0.3%… Most worrying is the plight of the manufacturing sector, which is now in its deepest downturn since 2013 as trade flows contracted at the sharpest rate since the debt crisis-ridden days of 2012.

Also: “Forward-looking indicators such as business optimism and backlogs of work suggest that growth could be even weaker in the second quarter… Any such further loss of growth momentum in the second quarter compared to the 0.2% GDP rise signalled for the first three months of the year would raise doubts on the economy’s ability to grow by more than 1% in 2019.”

Germany PMI manufacturing dived to 44.7, entrenched downturn with steepest contraction since 2012

In March, Germany PMI manufacturing dropped sharply to 44.7, down from 47.6 and missed expectation of 48.0. That’s also the lowest level in 79 months. PMI services dropped to 54.9, down from 55.3 but beat expectation of 54.8. PMI composite dropped to 51.5, down from 52.8, hit a 69-month low.

Phil Smith, Principal Economist at IHS Markit said: “The downturn in Germany’s manufacturing sector has become more entrenched, with March’s flash data showing accelerated declines in output, new orders and exports. Uncertainty towards Brexit and US-China trade relations, a slowdown in the car industry and generally softer global demand all continue to weigh heavily on the performance of the manufacturing sector, which is now registering the steepest rate of contraction since 2012.

France PMIs: Contraction in both manufacturing and services

In March, France PMI manufacturing dropped to 49.8, down from 51.5 and missed expectation of 51.4. PMI services dropped to 48.7, down from 50.2 and missed expectation of 50.6. PMI composite dropped to 48.6, down from 50.4.

Eliot Kerr, Economist at IHS Markit said: “At the end of the first quarter, the French private sector was unable to continue the recovery seen in February, as both the manufacturing and service sectors registered contractions in business activity. Worryingly, new orders continued to tumble amid a slowdown in demand and downward momentum in new export business. New work from abroad fell at the fastest pace for nearly three years, with a broad-based decline across both sectors.”

EU approved short Brexit extension, cliff edge delayed to April 12

At the European Council meeting in Brussels yesterday, EU approved a short Brexit extension for UK to decide which way they’d choose to go. If not Brexit deal is approved by the House of commons, The extension will be until April 12, when UK has to indicate a way forward. If a Brexit deal is approved, the extension will be until May 22. The offer is accepted by UK Prime Minister Theresa May.

EU President Donald Tusk said “the cliff edge will be delayed”, adding that “I was really sad before our meeting, now I’m much more optimistic.” He also noted, until April 12, “all options will remain open” and “the UK government will still have a choice between a deal, no deal, a long extension or revoking Article 50 ”

May said after the summit that “what the decision today underlines is the importance of the House of Commons passing a Brexit deal next week so that we can bring an end to the uncertainty and leave in a smooth and orderly manner”. She added “tomorrow morning, I will be returning to the U.K. and working hard to build support for getting the deal through.”

Canadian retail sales dropped -0.3%, CPI ticked up to 1.5%

Canadian Dollar weakens after weaker than expected retail sales data. Headline sales dropped -0.3% mom in January, below expectation of 0.4% mom. Ex-auto sales rose 0.1% mom, matched consensus.

Headline CPI accelerated to 1.5% yoy, up from 1.4% yoy and beat expectation of 1.4% yoy. CPI core-common slowed to 1.8% yoy, down from 1.9% yoy, matched expectations. CPI core-media was unchanged at 1.8% yoy. CPI core-trim was unchanged at 1.9% yoy.

Trump said he won’t drop auto tariffs to zero even if EU proposes so

In a Fox Business interview, Trump repeated that EU is treating the US as bad as China in terms of trade. And, asked if he would agree to zero tariffs on autos if the EU proposed so, Trump said “no”. He added, “I would do it for certain products, but I wouldn’t do it for cars.” Trump is again inconsistent with what he said before. Apparently, he’s not that much of a free trade advocate as he proclaimed.

In the G7 summit last June, Trump surprised other leaders and called for dropping all tariffs, trade barriers and subsidies. He said that “Ultimately that’s what you want, you want tariff free, no barriers, and you want no subsides because you have some countries subsidizing industries and that’s not fair”. And, “so you go tariff free, you go barrier free, you go subsidy free, that’s the way you learned at the Wharton School of Finance.”

Economic advisor Larry Kudlow also aid “I don’t know if they were surprised with President Trump’s free trade proclamation, but they certainly listened to it and we had lengthy discussions about that… “As the president said, reduce these barriers, in fact go to zero, zero tariffs, zero non-tariff barriers, zero subsidies, and along the way we’re going to have to clean up the international trading system.”

Japan CPI core slowed to 0.7% yoy, drifting away from BoJ’s target

Japan national CPI core (all items less fresh food) slowed to 0.7% yoy in February, down from 0.8% yoy and missed expectation of 0.8% yoy. CPU core-core (all items less food and energy) remained sluggish at 0.4% yoy, unchanged from January. Headline all items CPI was unchanged at 0.2%.

Despite BoJ’s massive monetary stimulus, there is no sign for CPI core to achieve the 2% target. And even worse, it’s actually moving farther away from the goal. Sluggish core-core reading is providing no help too. Moreover, there are risks of drag by slowdown in overseas economy. For now, there is practically no case for BoJ to exit ultra-loose policy any time soon.

Japan PMI manufacturing unchanged at 48.9, sustained downturn

Japan PMI manufacturing was unchanged at 48.9 in March, missed expectation of 48.9. Markit noted there are “further production cutbacks amid weaker new order inflows”. Also, “business confidence remains below long-run average”.

Joe Hayes, Economist at IHS Markit, said: “Further struggles for Japanese manufacturers were apparent at the end of Q1, with latest flash PMI data showing a sustained downturn. Slack demand from domestic and international markets prompted the sharpest cutback in output volumes for almost three years. With input purchasing falling, firms appear to be anticipating further troubles in the short-term. Indeed, concern of weaker growth in China and prolonged global trade frictions kept business confidence well below its historical average in March.”

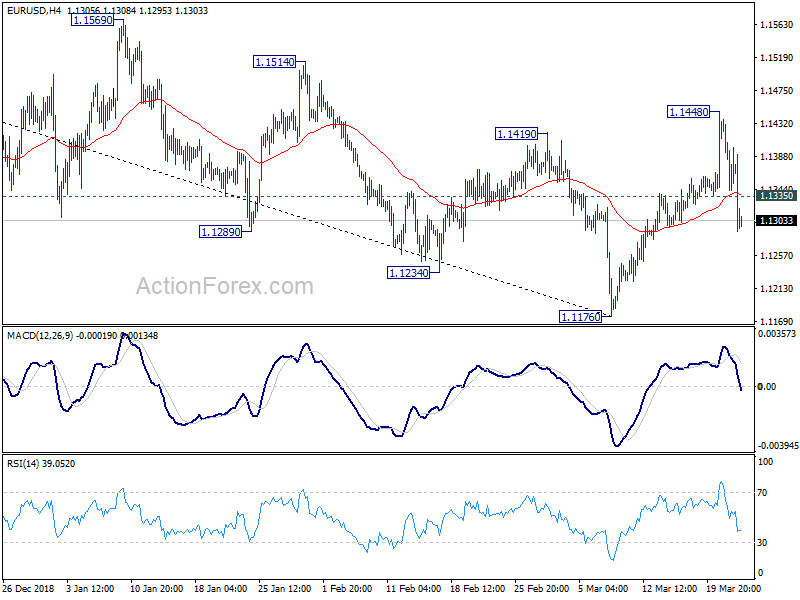

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1329; (P) 1.1384; (R1) 1.1429; More…..

EUR/USD’s sharp decline today and break of 1.1335 minor support suggests that rebound from 1.1176 has completed at 1.1148. The development dampened prior bullish view. Intraday bias turned back to the downside for retesting 1.1176 low first. On the upside, break of 1.1448 will extend the rebound to 1.1514/1569 resistance zone first.

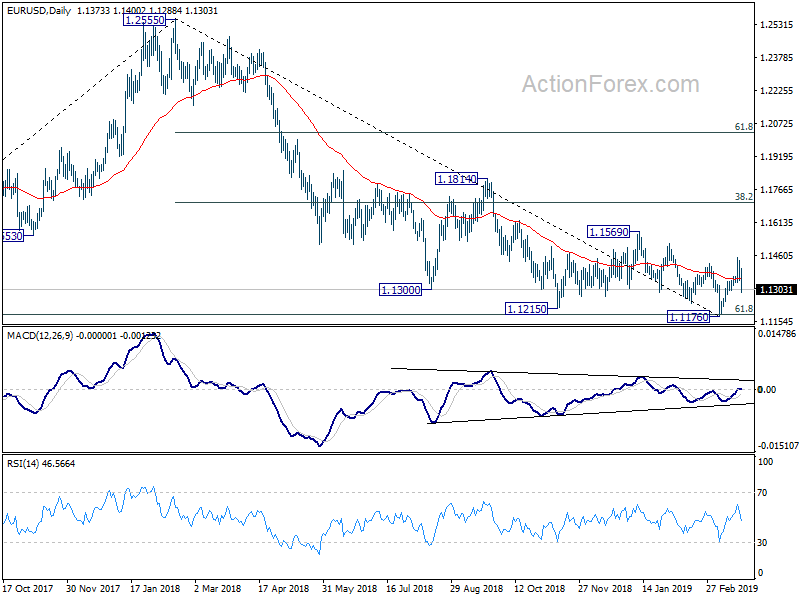

In the bigger picture, current development suggests that a medium term bottom could be formed at 1.1176 already. That came after hitting 61.8% retracement of 1.0339 (2016 low) to 1.2555 (2018 high) at 1.1186, on bullish convergence condition in daily MACD. Further rally could be seen back to 38.2% retracement of 1.2555 to 1.1176 at 1.1703. It’s a bit early to confirm medium term bullish reversal. The structure of the rise from 1.1176 and reaction to 1.1703 fibonacci level will be watched for making an assessment later. But in any case, decisive break of 1.1176 is needed to confirm resumption of down trend. Otherwise, outlook is neutral at worst.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Feb | 0.70% | 0.80% | 0.80% | |

| 00:30 | JPY | PMI Manufacturing Mar P | 48.9 | 49.2 | 48.9 | |

| 08:15 | EUR | France Manufacturing PMI Mar P | 49.8 | 51.4 | 51.5 | |

| 08:15 | EUR | France Services PMI Mar P | 48.7 | 50.6 | 50.2 | |

| 08:30 | EUR | Germany Manufacturing PMI Mar P | 44.7 | 48 | 47.6 | |

| 08:30 | EUR | Germany Services PMI Mar P | 54.9 | 54.8 | 55.3 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | 47.6 | 49.5 | 49.3 | |

| 09:00 | EUR | Eurozone Services PMI Mar P | 52.7 | 52.7 | 52.8 | |

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | 36.8B | 17.3B | 16.2B | |

| 12:30 | CAD | Retail Sales M/M Jan | -0.30% | 0.40% | -0.10% | -0.30% |

| 12:30 | CAD | Retail Sales Ex Auto M/M Jan | 0.10% | 0.10% | -0.50% | -0.80% |

| 12:30 | CAD | CPI M/M Feb | 0.70% | 0.60% | 0.10% | |

| 12:30 | CAD | CPI Y/Y Feb | 1.50% | 1.40% | 1.40% | |

| 12:30 | CAD | CPI Core – Common Y/Y Feb | 1.80% | 1.80% | 1.90% | |

| 12:30 | CAD | CPI Core – Median Y/Y Feb | 1.80% | 1.80% | 1.80% | |

| 12:30 | CAD | CPI Core – Trim Y/Y Feb | 1.90% | 1.80% | 1.90% | |

| 13:45 | USD | US Manufacturing PMI Mar P | 53.6 | 53 | ||

| 13:45 | USD | US Services PMI Mar P | 55.8 | 56 | ||

| 14:00 | USD | Wholesale Inventories M/M Jan | 0.10% | 1.10% | ||

| 14:00 | USD | Existing Home Sales Feb | 5.10M | 4.94M |