{kind=link}

Sterling is trading as the weakest one for today so far after suffering some selling in European session. No support is seen for the Pound even though high profile Brexiteer Jacob Rees-Mogg indicated that he might support Prime Minister Theresa May’s Brexit deal. However, loss is limited in Sterling as the overall picture remains unclear. For now, it’s uncertain whether the government will pull tomorrow’s Brexit meaningful vote due to far insufficient support.

Staying in the currency markets, Australian Dollar was lifted earlier today by strong rally in Chinese stocks. But it lost some momentum after European markets turned mixed. Also, the Aussie will facing tests from RBA minutes as well as house price data in the upcoming session. Euro picked up some strengthen even though Bundesbank warned of subdued German growth in Q1. Rise in German yield is unpinning Euro for now. Overall, the markets lack clear direction in early US session.

In Europe, FTSE is up 0.64%. DAX is down -0.30%. CAC is flat. German 10-year yield is up 0.0094 at 0.095, getting close to 0.1 handle. Earlier in Asia, Nikkei rose 0.62%. Hong Kong HSI rose 1.37%. China Shanghai SSE rose 2.47%. Singapore Strait Times rose 0.40%. Japan 10-year JGB yield rose 0.002 to -0.035.

On the data front, Canada international securities transactions rose CAD 28.4B in January. Eurozone trade surplus widened to EUR 17.0B in January, missed expectation of EUR 17.2B. UK Rightmove house price rose 0.4% mom in March. Japan industrial production was finalized at -3.4% mom in January, trade surplus widened slightly to JPY 0.12T in February.

Bundesbank: German growth subdued in Q1 as consumption offset by weak manufacturing

Bundesbank said in the monthly report that German economic growth remained subdued in Q1. The main reasons include weak industrial production, falling auto exports and deteriorating manufacturing sentiment. Manufacturing sector would drag down overall economic performance for the third straight quarter.

On the other hand, construction and private consumption should provide support to the economy. Employment also continues to rise despite slowdown. Bundesbank added that private consumption could pickup significantly as signaled by strong increase in retail sales.

German FM Scholz : Some richer countries only think of their own interest

German Finance Minister Olaf Scholz warned in at the World Policy Forum in Berlin that trade conflicts are damaging the world. Without naming any country, he singled out “richer countries” who only think of their own interest. At the same time, he also urged Europe to have one voice to have more bargaining power.

Scholz said “trade conflicts, as we have seen over the last months – especially between richer countries only thinking of their own interest – are damaging the world economy”. He added that “trade policy has been an EU-level responsibility for a long time”. And, “it is obvious that we have much more bargaining power if we speak with one European voice… only together we are able to set and enforce standards of fair trade.”

EU to seek China agreement to open up market in upcoming summit

Reuters reported that EU is seeking China’s agreement to open up its market by summer 2019. An EU drafted six-page joint communique obtained reads China and the EU will “agree by summer 2019 on a set of priority market access barriers and requirements facing their operators.” It’s intended to be the deliverable of the EU-China summit on April 9 in Brussels. Chinese Premier Li Keqian is expected to be there, meeting European Commission President Jean-Claude Juncker and European Council President Donald Tusk.

While there is no other detail reported, we believed it’s released to the proposed 10 actions by the European Commission on relations with China release last week. The proposal will be discussed and endorsed at the European Council meeting this week on March 21. There, EU described China as a “cooperation partner” and “negotiating partner” as well as “systemic rival promoting alternative models of governance.” Some important actions focus on issues like subsidies and forced technology transfers, reciprocity and open up procurement opportunities in China.

Brexiteer Rees-Mogg hints he might back May’s deal, as it’s better than no Brexit

One of the most influential Brexiteer hinted today that the might back Prime Minister Theresa May’s Brexit deal because a bad deal is better than no Brexit. Jacob Rees-Mogg, chairman of the European Research Group told LBC Radio that “no deal is better than a bad deal but a bad deal is better than remaining in the European Union in the hierarchy of deals.”

Rees-Mogg warned that “a two-year extension is basically remaining in the European Union.” But he also noted: “The question people like me will ultimately have to answer is: can we get to no-deal instead? If we can get to no-deal instead, that is a better option… but I am concerned the prime minister is determined to stop a no-deal.”

Separately, Foreign Minister Jeremy Hunt said there were “cautious signs of encourage” regarding May’s deal. And the government would “hope” to have another meaningful vote tomorrow. But he emphasized “we need to be comfortable that we’ll have the numbers”. Hunt of said “the risk of no-deal, at least as far as the UK parliament is concerned, has receded somewhat but the risk of Brexit paralysis has not.”

BCC downgrades UK growth forecasts on Brexit and global slowdown

The British Chambers of Commerce (BCC) has downgraded UK growth forecast on “weaker outlook for business investment and trade amid continued Brexit uncertainty and slower expected global economic growth”. For 2019, growth forecast was downgraded from 1.3% to 1.2%. For 2020, growth forecasts was downgraded from 1.5% to 1.3%. in 2021, growth is projected to pick up slightly to 1.4%.

Also, BCC noted that business investment is projected to contract by -1.0% in 2019. And that would be the weakest outturn in a decade since the financial crisis in 2009. BCC blamed that “ongoing uncertainty over the UK’s future relationship with the EU is expected to continue to weigh on investment intentions.” And, “diversion of resources to prepare for no deal and the high upfront cost of doing business in the UK is also projected to limit the extent to which investment activity will bounce back over the near term.”

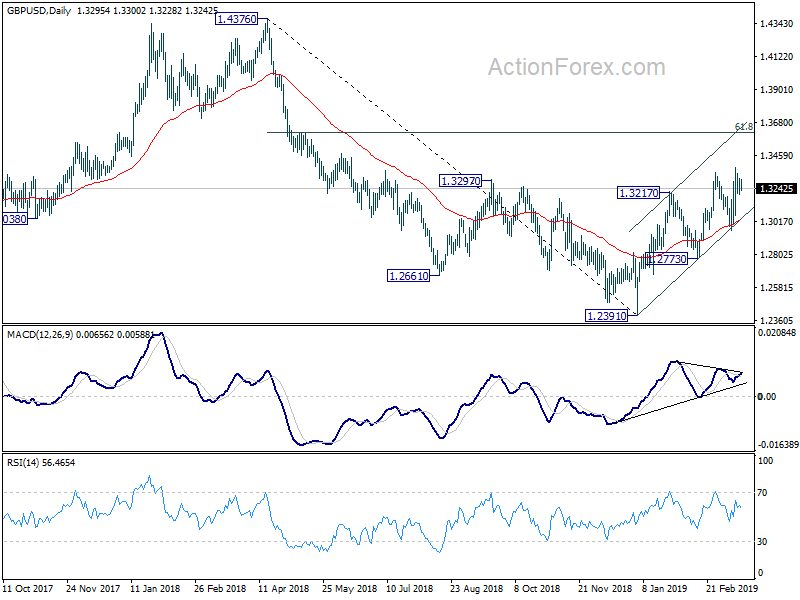

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3231; (P) 1.3265; (R1) 1.3328; More….

GBP/USD is staying in consolidation below 1.3381 temporary top and intraday bias remains neutral. Further rise is expected as long as 1.2960 support holds. On the upside, firm break of 1.3381 will target 61.8% retracement of 1.4376 to 1.2391 at 1.3618 next. However, on the downside, firm break of 1.2960 will indicate that rebound from 1.2391 has completed earlier than expected. Deeper fall would then be seen to 1.2773 support for confirmation.

In the bigger picture, medium term decline from 1.4376 (2018 high) should have completed at 1.2391. Rise from 1.2391 is now seen as the third leg of the corrective pattern from 1.1946 (2016 low). Further rise could be seen through 1.4376 in medium term. On the downside, though, break of 1.2773 support will dampen this view. Focus will be turned back to 1.2391 low and break will resume the fall from 1.4376 to 1.1946.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Feb | 0.12T | 0.09T | -0.37T | -0.29T |

| 00:01 | GBP | Rightmove House Prices M/M Mar | 0.40% | 0.70% | ||

| 04:30 | JPY | Industrial Production M/M Jan F | -3.40% | -3.70% | -3.70% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | 17.0B | 17.2B | 15.6B | 16.0B |

| 12:30 | CAD | International Securities Transactions (CAD) Jan | 28.40B | 15.03B | -18.96B | |

| 14:00 | USD | NAHB Housing Market Index Mar | 63 | 62 |