{kind=link}

Australian and New Zealand Dollar are the strongest ones for today so far as the forex markets seem to be cheering positive developments in US-China trade negotiations. The idea of 60-day extension to trade truce is certainly welcomed given the complexity in the deal, in particular enforcement. Data from Japan and Germany also showed both countries avoided technical recession in H2 2018. But such positive sentiment is actually not reflected in the stock markets. Though, for now, Yen is the weakest one for today, followed by Dollar.

Over the week, commodity currencies remain the strongest ones, led by New Zealand Dollar. Dollar received some blessing from stronger than expected CPI overnight and it’s trading down only against NZD, AUD and CAD. The greenback will look into retail sales and PPI today for some more strength. Yen is the worst performing one, followed by Swiss Franc. Sterling is not too far away and it’s awaiting Brexit debate in the Commons.

Technically, USD/JPY’s stronger than expected rise now puts 114.20/54 resistance into focus. EUR/USD breached 1.1257 overnight but quickly recovered. Similarly, USD/CHF breached 1.0092 resistance but retreated quickly. The greenback is still in favor to rise against the two. GBP/USD is eyeing 1.2832 temporary low. Break there will likely give Dollar a hand.

In other markets, Nikkei closed down -0.02%. Hong Kong HSI is down -0.25%. China Shanghai SSE is down -0.05%. Singapore Strait Times is up 0.07%. Japan 10-year JGB yield is down -0.0093 at -0.016, staying negative. Overnight, DOW rose 0.46%. S&P 500 rose 0.30%. NASDAQ rose 0.08%. 10-year yield rose 0.024 to 2.708, reclaimed 2.7 handle. 30-year yield rose 0.012 to 3.034, staying above 3.0 handle.

Trump considering 60-day extension to trade truce as high level talks start

High level US-China trade negotiations started in the Diaoyutai state guest house in Beijing today, involving US Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer, and Chinese Vice Premier Liu He. Ahead of that, Mnuchin said he’s “looking forward to discussions today”. There was no elaborate and so far, there is no news leaked regarding the talks.

Trump indicated earlier this week that he’s willing to let the March 1 trade truce deadline slide a little bit. Trump further added that the talks are “going along very well” and the Chinese are “showing us tremendous respect.” Bloomberg reported that Trump is indeed considering to extend the deadline by 60 days, after rejecting the initial request by China of 90 days extension. But the rumor is not confirmed.

China trade balance: Import from US plunged -41%, from EU rose…

January trade data from China showed a better picture. Exports grew 9.1% yoy versus expectation of -3.3% yoy. Import dropped only -1.5% yoy versus expectation of -10.2% yoy. Trade surplus narrowed to USD 39.2B, above expectation of USD 32.0B. However, it should be noted that the trade data for the first two months of the year are generally distorted by Lunar New Year holidays. Thus, while the data are positive, it’s premature to declare that the slow down in China has bottomed. Nevertheless, it’s worth noting that exports to the US since tariff war began were not so much affected. But import from the US plunged, quite notably in Jan by -41%.

In USD terms, total trade rose 4.0% yoy to USD 396B. Import dropped -1.5% yoy to USD 178.4B. Exports rose 9.1% yoy to USD 217.6B. Trade surplus rose to USD 39.2B.

With EU, total trade rose 12.4% yoy to USD 64.5B. Import rose 8.2% yoy to 25.9B. Export rose 15.3% yoy to USD 38.6B. Trade surplus was at USD 12.7B.

With US, total trade dropped -13.9% yoy to USD 45.8B. Import dropped -41% yoy to USD 9.2B. Exports dropped -2.4% yoy to USD 36.5B. Trade surplus was at USD 27.3B.

With AU, total trade rose 10.8% yoy to USD 14.4B. Import rose 7.6% yoy USD 10.1B. Export rose 19.1% yoy to USD 4.3B. Trade deficit was at USD 5.8B.

German economy stagnated in Q4, but narrowly escaped recession

Germany GDP stagnated in Q4 and grew 0.0% qoq. But that was enough to narrow escape a technical recession following -0.2% contraction in Q3. Over the year, GDP grew 0.9% yoy in Q4. For the whole year of 2018, GDP grew 1.5% calendar adjusted.

Looking at the details, positive contributions mainly came from domestic demand. Development of foreign trade did not make a positive contribution to growth in the fourth quarter. According to provisional calculations, exports and imports of goods and services increased nearly at the same rate in the quarter-on-quarter comparison.

UK RICS house price balance dropped, resolution of Brexit negotiations critical

UK RICS house price balanced dropped to -22 in January, below expectation of -20. RBIC noted that activity measures for both buyers and sellers continue to slip. Also, price balance weakens at the national level, led by London and the South East. And, as sales drop, the lettings market is faring better with demand rising.

Simon Rubinsohn, RICS chief economist, warned that “resolution of the Brexit negotiations is widely seen as critical to encouraging potential buyers back into the market, although whether that will be sufficient in London and parts of the South East where affordability remains stretched and the tax changes are most penal remains to be seen.”

Japan GDP rebounded with weak momentum, but avoided recession

Japan GDP grew 0.3% qoq in Q3, rebounding from Q3’s -0.6% qoq contraction. The good news is that Japan avoided a technical recession of two consecutive quarters of contraction. But growth was disappointing and missed expectation of 0.4% qoq. GDP deflator dropped -0.3% yoy, slightly better than expectation of -0.4% yoy.

Japanese Economy Minister Toshimitsu Motegi said in a statement that “the economy is in gradual recovery as growth is led by private demand”. However, “China-bound exports of information-related materials have weakened as the Chinese economy slowed”. He added that the government needs to “monitor uncertainty over global economic outlook including Chinese economy as well as fluctuations in financial markets.”

Looking head

Eurozone GDP and employment will be the main feature in European session. Later in the data, US data will take center stage. Retail sales, PPI, jobless claims and business inventories will be released. Canada will also release manufacturing sales and new housing price index.

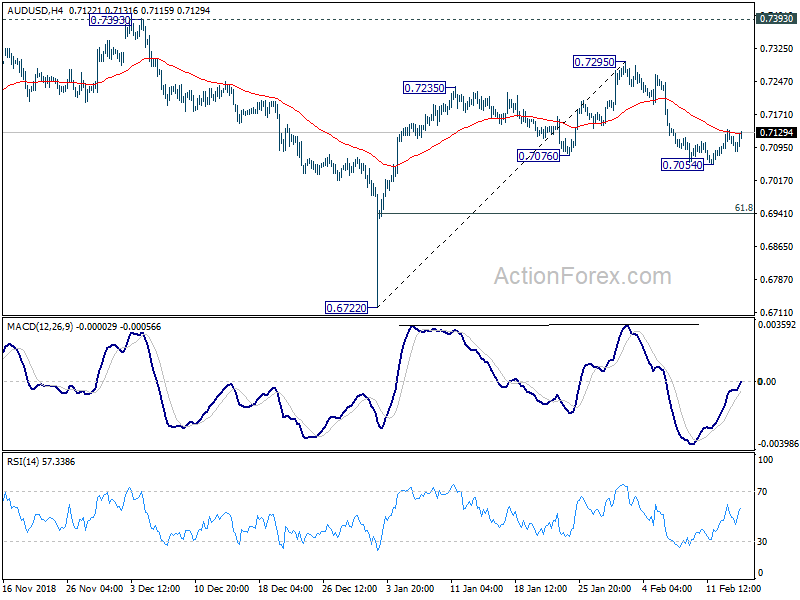

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7071; (P) 0.7103; (R1) 0.7122; More…

Intraday bias in AUD/USD remains neutral at this point. Consolidation from 0.7054 is still in progress. Stronger rise could be seen but upside should be limited well below 0.7295 resistance to bring another decline. We’re holding on to the view that rebound from 0.6722 has completed at 0.7295 already. On the downside, break of 0.7054 will turn bias to the downside for 61.8% retracement of 0.6722 to 0.7295 at 0.6941 next.

In the bigger picture, as long as 0.7393 resistance holds, we’d treat fall from 0.8135 as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q4 P | 0.30% | 0.40% | -0.60% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | -0.30% | -0.40% | -0.30% | |

| 00:00 | AUD | Consumer Inflation Expectation Feb | 3.70% | 3.50% | ||

| 00:01 | GBP | RICS House Price Balance Jan | -22.00% | -20.00% | -19.00% | |

| 02:00 | CNY | Trade Balance (USD) Jan | 39.2B | 32.0B | 57.1B | |

| 02:00 | CNY | Trade Balance (CNY) Jan | 271B | 235B | 395B | |

| 07:00 | EUR | German GDP Q/Q Q4 P | 0.00% | 0.10% | -0.20% | |

| 07:30 | CHF | Producer & Import Prices M/M Jan | -0.40% | -0.60% | ||

| 07:30 | CHF | Producer & Import Prices Y/Y Jan | -0.20% | 0.60% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.20% | 0.20% | ||

| 10:00 | EUR | Eurozone Employment Q/Q Q4 P | 0.20% | 0.20% | ||

| 13:30 | CAD | Manufacturing Sales M/M Dec | 0.70% | -1.40% | ||

| 13:30 | CAD | New Housing Price Index M/M Dec | 0.00% | 0.00% | ||

| 13:30 | USD | Initial Jobless Claims (FEB 09) | 225K | 234K | ||

| 13:30 | USD | PPI M/M Jan | 0.10% | -0.20% | ||

| 13:30 | USD | PPI Y/Y Jan | 2.10% | 2.50% | ||

| 13:30 | USD | PPI Core M/M Jan | 0.20% | -0.10% | ||

| 13:30 | USD | PPI Core Y/Y Jan | 2.50% | 2.70% | ||

| 13:30 | USD | Retail Sales Advance M/M Dec | 0.10% | 0.20% | ||

| 13:30 | USD | Retail Sales Ex Auto M/M Dec | 0.00% | 0.20% | ||

| 15:00 | USD | Business Inventories Nov | 0.20% | 0.60% | ||

| 15:30 | USD | Natural Gas Storage | -237B |