{kind=link}

Yen and Swiss Franc are trading broadly lower today thanks to rebound in global equities. Fresh selling is seen on news that White House senior counselor Kellyanne Conway said Trump may still meet Chinese President Xi Jinping in the near future. And she said that it looks like US and China are getting closer to deal. Dollar also rides on the news and jumps broadly in early US session. Meanwhile, Sterling is generally weak after poor GDP data, which showed deep contraction in December. But loss in the pound is so far limited.

Lower-level US-China trade talks started today in Beijing. Later on Thursday and Friday, high level talks will be carried out involving USTR Robert Lighthizer, Treasury Secretary Steven Mnuchin, and Chines Vice Premier Liu He. There has to be some breakthroughs in the areas of on intellectual property theft, forced technology transfer, State owned enterprises, and enforcement of agreement in order to have a deal in the near futures.

Technically, USD/CHF’s rally resumed by taking out 1.0028 and is on track to retest 1.0128 high. USD/JPY also broke out of tight range, through 110.16, to resume recent rebound. EUR/USD edges lower today and is eyeing 1.1289 support. Break there will bring retest of 1.1215 low next. AUD/USD weakens today, thanks to Dollar’s strength mainly, and it main challenge 0.7060 temporary low later in the session.

In European markets, currently, FTSE is up 0.77%. DAX is up 1.02%. CAC is up 1.09%. German 10-year yield is up 0.0241 at 0.114. Earlier in Asia, Hong Kong HSI rose 0.71%. China Shanghai SSE was back from holiday and rose 1.36%. Singapore Strait Times rose 0.13%. Japan was on holiday today.

UK GDP contracted -0.4% in Dec, Q4 growth slowed to 0.2%

The batch of economic data from UK is all the way poor. GDP grew only 0.2% qoq in Q4, below expectation of 0.3% qoq, and a sharp slowdown from Q3’s 0.6% qoq. In December, GDP contracted -0.4% mom , much worse than expectation of 0.0% mom. Annually, GDP growth slowed to 1.4%, lowest since 2012.

ONS Head of GDP Rob Kent-Smith said in the release that ” manufacturing of cars and steel products seeing steep falls and construction also declining.” Also, “declines were seen across the economy in December, but single month data can be volatile meaning quarterly figures often give a better indication of the health of the economy.”

Also from UK, Industrial production dropped -0.5% mom, -0.9% yoy in December versus expectation of 0.1% mom, -0.5% yoy. Manufacturing production dropped -0.7% mom, -2.1% yoy in December versus expectation of 0.2% mom, -1.1% yoy. Construction output dropped -2.8% in December versus expectation of 0.1% mom. Trade deficit narrowed to GBP -12.1B in December versus expectation of -12.0B.

Also released, Swiss CPI slowed to 0.6% yoy in January, down from 0.7% yoy and matched expectations.

UK Fox: Brexit is not the only reason for slowdown

UK Trade Minister Liam Fox said today that Brexit is not the only reason for growth slowdown. He said in a news conference that “clearly there are those who believe that Brexit is the only economic factor applying to the UK economy.”

But he argued that “the predicted slowdown in a number of European economies is not disconnected from the slowdown, for example, in China”. And, “the idea that Brexit is the only factor affecting the global economy is just to miss the point.”

Meanwhile, even with Brexit impasse, “the chances of having a second referendum are as close to nil as I could imagine.”

UK PM May to update parliament on Brexit on Tuesday

UK Prime Minister Theresa May’s spokesman said she will make a statement in the parliament tomorrow. And, “that will be an update on Brexit talks and is in advance of the debate taking place on Thursday.”

That was a day ahead of market expectations. But anyway, parliament debate on February 14 will be a major focus this week. Attention would be on any motions that could shift the control of Brexit from the government to the parliament. And if so, that would open up the route for lawmakers to renegotiate, delay, or even block Brexit.

EU chief Brexit negotiator Michel Barnier warned today that “this time that remains is extremely short”. And he reiterated that that Brexit deal on the table ” remains the best way to ensure an orderly withdrawal of the UK.” Luxembourg’s Prime Minister Xavier Bettel said alongside Barnier that “We never pushed for Brexit, we never demanded Brexit… The responsibility started in London and is still in London.”

UK and Swiss signed agreement to protect GBP 32B trade relationship after Brexit

UK and Switzerland signed an agreement on Sunday that will protect GBP 32B trade relationship between the two countries. With the agreement, both countries will continue to trade on preferential terms after Brexit. That is, the two countries could continue to trade freely without new tariffs. But financial services are not included in the deal.

UK Trade Minister Liam Fox hailed that “Switzerland is one of the most valuable trading partners that we are seeking continuity for.” And, “this is of huge economic importance to UK businesses so I’m delighted to be here in Bern ensuring continuity for 15,000 British exporters. ”

Fox added that “not only will this help to support jobs throughout the UK but it will also be a solid foundation for us to build an even stronger trading relationship with Switzerland as we leave the EU.”

Bank of France: GDP to growth 0.4% in Q1

Bank of France said today that according to the monthly index of business activity (MIBA), the country’s GDP is expected to grow 0.4% qoq in Q1 this year.

The business sentiment indicator in manufacturing dropped to 99 in January, down from 102. in December. Services indicator dropped to 100, down from 101. Construction indicator was unchanged at 105.

Also, BoF said for February, Business leaders expect industrial production to pick up, service sector activity to accelerate and construction sector activity to continue to grow.

ECB de Guindos: Wage growth increasingly broad-based, inflation to rise over medium term

ECB Vice President Luis de Guindos sounded confidence in his comments on inflation today. He said that “wage growth has become increasingly broad-based in recent years.” And, “this, together with our monetary policy measures and the ongoing economic expansion, is expected to translate into higher underlying inflation over the medium term.”

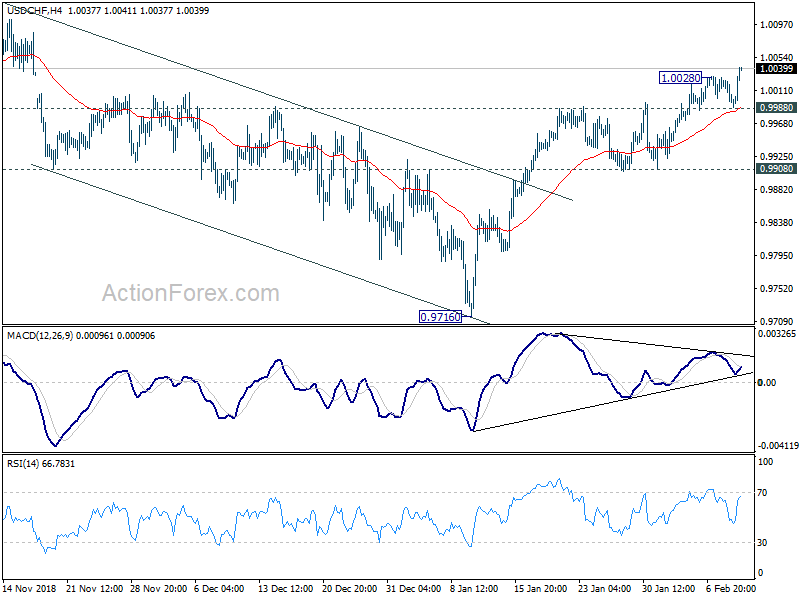

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9989; (P) 1.0009; (R1) 1.0023; More….

USD/CHF’s rise from 0.9716 resumed quickly after brief consolidation. Intraday bias is back on the upside for 1.0128 key resistance. Decisive break there will resume larger up trend from 0.9186. On the upside, below 0.9988 minor support will turn intraday bias neutral again. But any retreat should be contained by 0.9908 support to bring rise resumption.

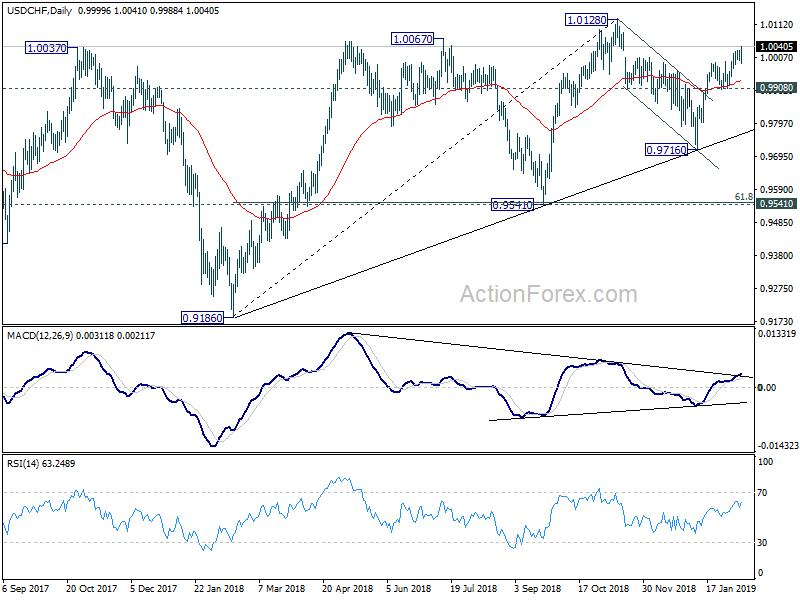

In the bigger picture, USD/CHF drew strong support from medium term trend line and rebounded. That suggests rise from 0.9186 is still in progress. Further break of 1.0128 will confirm up trend resumption and target 1.0342 key resistance. Nevertheless, break of 0.9716 will dampen this bullish view and at least bring deeper fall to 0.9541 key support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 7:30 | CHF | CPI M/M Jan | -0.30% | -0.30% | -0.30% | |

| 7:30 | CHF | CPI Y/Y Jan | 0.60% | 0.60% | 0.70% | |

| 9:30 | GBP | GDP M/M Dec | -0.40% | 0.00% | 0.20% | |

| 9:30 | GBP | GDP Q/Q Q4 P | 0.20% | 0.30% | 0.60% | |

| 9:30 | GBP | GDP Y/Y Q4 P | 1.30% | 1.40% | 1.50% | |

| 9:30 | GBP | Total Business Investment Q/Q Q4 P | -1.40% | -1.00% | -1.10% | |

| 9:30 | GBP | Index of Services 3M/3M Dec | 0.40% | 0.40% | 0.30% | 0.40% |

| 9:30 | GBP | Visible Trade Balance (GBP) Dec | -12.1B | -12.0B | -12.0B | -12.4B |

| 9:30 | GBP | Industrial Production M/M Dec | -0.50% | 0.10% | -0.40% | -0.30% |

| 9:30 | GBP | Industrial Production Y/Y Dec | -0.90% | -0.50% | -1.50% | -1.30% |

| 9:30 | GBP | Manufacturing Production M/M Dec | -0.70% | 0.20% | -0.30% | -0.10% |

| 9:30 | GBP | Manufacturing Production Y/Y Dec | -2.10% | -1.10% | -1.10% | -1.20% |

| 9:30 | GBP | Construction Output M/M Dec | -2.80% | 0.10% | 0.60% |