{kind=link}

Pound is at the center of focus today as it finally shows some commitment on the downside. The trigger of the selloff is report that UK Prime Minister Theresa May is going to call off tomorrow’s Brexit parliamentary vote. Weak economic data of course also add to the pressure of the Pound. At this point, Sterling is overwhelmingly the weakest one for today, followed by Yen, and then Canadian. New Zealand Dollar is the strongest one so far. Euro shrugs off poor investor confidence data and follows as second strongest, thanks to rally to EUR/GBP.

Technically, GBP/USD’s break of 1.2661 key support now indicates medium term down trend resumption. EUR/GBP is heading to 0.9098 and break will put focus on 0.9305 high. GBP/JPY also breaks 142.76 support and is now on track to 139.88 key support. The forex markets are rather steady elsewhere though. Dollar trades a touch weaker against Euro and Swiss Franc but there is no follow through selling. The greenback is also bounded in familiar range against Aussie and Canadian.

In other markets, FTSE is now trading up 0.49%, thanks to lower Pound. DAX is down -0.39% and CAC is down -0.30%. German 10 year yield is up 0.0076 at 0.258. Meanwhile, Italian 10 year yield is down -0.031 at 3.100. German-Italian spread continues to narrow. WTI crude oil is trading at around 51.7 as consolidation continues. Gold is consolidating at around 1245. Earlier in Asia, all major indices closed lower, but except Nikkei, losses were limited. Nikkei closed down -2.12%, Hong Kong HSI down -1.19%, China Shanghai SSE down -0.82%, Singapore Strait Times dropped -1.24%. Japan 10 year JGB yield dropped for another day, by -0.023 to 0.04, pretty strong rally in bonds.

May to call off tomorrow’s Brexit vote, to make a statement at 1530GMT.

It’s reported that May has abruptly called off tomorrow’s parliamentary vote on her Brexit deal. There is no confirmation yet but the news is widely reported and not denied. May is set to make a statement later at 1530GMT.

Scotland’s First Minister Nicola Sturgeon criticized that “this is a watershed moment and an act of pathetic cowardice by a Tory government which has run out of road and is now collapsing into utter chaos”. She added that “the Prime Minister’s deal should come before the (UK parliament) immediately so that it can be voted down and we can replace Tory chaos with a solution that will protect jobs, living standards and Scotland’s place in Europe.”

Northern Irish DUP deputy leader Nigel Dodds said “If anyone needs any further lesson or demonstration on how not to negotiate, look at the shambles today of the government in the House of Commons having to pull a vote on something that they said was the only way forward.”

Opposition Labor Party leader Jeremy Corbyn said “The government has decided Theresa May’s Brexit deal is so disastrous that it has taken the desperate step of delaying its own vote at the eleventh hour”. And, “We don’t have a functioning government … Labour’s alternative plan for a jobs first deal must take centre stage in any future talks with Brussels.”

ECJ said UK free to revoke Brexit unilaterally

As widely expected, the European Court of Justice finally ruled today that “the United Kingdom is free to revoke unilaterally the notification of its intention to withdraw from the EU.” And, “Such a revocation, decided in accordance with its own national constitutional requirements, would have the effect that the United Kingdom remains in the EU under terms that are unchanged as regards its status as a Member State.

Separately, European Commission Jean-Claude Juncker talked with May over night weekend. His spokeswoman reiterated the position that “we have an agreement on the table” and “we will not renegotiate”, regarding Brexit deal. And, She added that European Union is ready for “all scenarios” of Brexit.

UK GDP rose 0.1% mom, industrial and manufacturing production contracted

Some volatility is seen in Sterling in early part of European session. It firstly declined against Euro, then was limited mildly by ECJ’s ruling on Brexit revocation. But overall movements are limited and not even a batch of weak economic data was economy to kick the Pound out of range.

UK GDP rose 0.1% mom in October, matched expectations. For the rolling three months Aug to Oct, growth to 0.4%, down from 0.6% from Jul to Sep. The slow down was even more noticeable, comparing to 0.7% recorded in both May to Jul and Jun to Aug periods. Services was the biggest contributor to growth in the Aug to Oct period, up 0.23%. Production rose merely 0.05% while construction rose 0.08%.

Also from UK, industrial production dropped -0.6% mom, -0.8% yoy in October versus expectation of 0.1% mom, -0.2% yoy. Manufacturing production dropped -0.9% mom, -1.0% yoy versus expectation of 0.0% mom, 0.0% yoy. Trade deficit widened to GBP -11.9B versus expectation of GBP -10.5B. Construction output dropped -0.2% mom versus expectation of -0.4% mom.

Eurozone Sentix investor confidence dropped to -0.3, downside similar to pre-crisis year 2007

Eurozone Sentix Investor Confidence dropped sharply to -0.3 in December, down from 8.8 and missed expectation of 8.4. It’s also the fourth decline in a row, and lowest reading since December 2014. Expectation index also dropped to -18.8, lowest since August 2012. Sentix noted that “the dynamics of the downturn are similar to those of the pre-crisis year 2007.”

Also, “sheer downward momentum that the economy is currently offering is impressive. The economy is “slimming down at a considerable pace, with pressures coming from “all corners” including “trade disputes, the Italian crisis, unrest in France and Belgium or Brexit.” Besides, “the momentum of the current downturn is in many respects similar to that of 2007, and banks, especially in Europe, appear to be in a similarly precarious position”.

Also released in European session, German trade surplus narrowed slightly to EUR 17.3B in October. Swiss unemployment rate dropped 0.1% to 2.4% in November.

OECD: RBA policy rates should start to rise soon

In a report released over the weekend, OECD said Australia’s “long span of positive output growth continues”. And, “continued robust output growth of around 3% is projected in the near future”. On RBA, OECD said that “in the absence of negative shocks, policy rates should start to rise soon”. It warned that “monetary conditions remain very accommodative, with the risk of imbalances accumulating further if the low-interest rate environment persists.” And, “in the absence of a downturn, a gradual tightening should start as inflation edges up and wage growth gains momentum.”

However, OECD also warned that the housing market is “a source of vulnerability”. So far, “data point to a soft landing without substantial consequence for the overall economy.” But “risk of a hard landing remains.” And it urged authorities to “prepare contingency plans for a severe collapse in the housing market. These should include the possibility of a crisis situation in one or more financial institutions.

Released earlier in Asia Pacific, New Zealand manufacturing activity rose 2.0% qoq in Q3. Japan GDP was finalized at -0.6% qoq in Q3, revised down from -0.5% qoq. Current account surplus narrowed to JPY 1.33T. Australia home loans rose 2.2% mom in October, versus expectation of -0.5% mom.

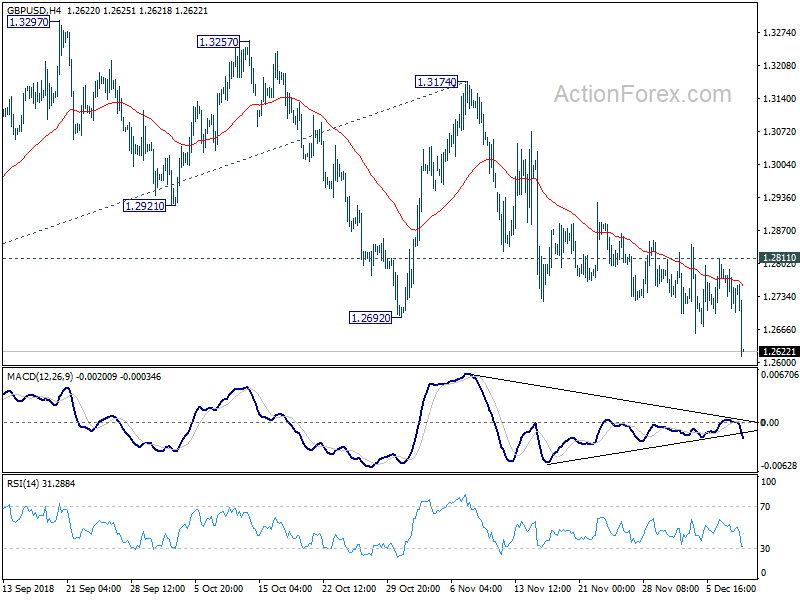

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2693; (P) 1.2749; (R1) 1.2787; More…

GBP/USD drops to as low as 1.2611 so far today. Break of 1.2661 support indicates resumption of down trend from 1.4376. Intraday bias is now on the downside for deeper decline. Next target is 61.8% projection of 1.4376 to 1.2661 from 1.3174 at 1.2114. On the upside, break of 1.2811 resistance is needed to indicate short term bottoming. Otherwise, near term outlook will remain bearish even in case of recovery.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend from 2.1161 (2007 high). And this will now remain the preferred case as long as 1.3174 structural resistance holds. GBP/USD should now target a test on 1.1946 first. Decisive break there will confirm our bearish view.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Activity SA Q/Q Q3 | 2.00% | 1.80% | ||

| 23:50 | JPY | GDP Q/Q Q3 F | -0.60% | -0.50% | -0.30% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 F | -0.30% | -0.30% | -0.30% | |

| 23:50 | JPY | Current Account (JPY) Oct | 1.21T | 1.29T | 1.33T | |

| 00:30 | AUD | Home Loans M/M Oct | 2.20% | -0.50% | -1.00% | |

| 05:00 | JPY | Eco Watchers Survey Current Nov | 51 | 49.5 | 49.5 | |

| 06:45 | CHF | Unemployment Rate Nov | 2.40% | 2.50% | 2.50% | |

| 07:00 | EUR | German Trade Balance Oct | 17.3B | 17.2B | 17.6B | |

| 09:30 | GBP | Visible Trade Balance (GBP) Oct | -11.9B | -10.5B | -9.7B | -10.7B |

| 09:30 | GBP | Industrial Production M/M Oct | -0.60% | 0.10% | 0.00% | |

| 09:30 | GBP | Industrial Production Y/Y Oct | -0.80% | -0.20% | 0.00% | |

| 09:30 | GBP | Manufacturing Production M/M Oct | -0.90% | 0.00% | 0.20% | |

| 09:30 | GBP | Manufacturing Production Y/Y Oct | -1.00% | 0.00% | 0.50% | |

| 09:30 | GBP | Construction Output M/M Oct | -0.20% | -0.40% | 1.70% | |

| 09:30 | GBP | GDP M/M Oct | 0.10% | 0.10% | 0.00% | |

| 09:30 | GBP | Index of Services 3M/3M Oct | 0.30% | 0.30% | 0.40% | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | -0.3 | 8.4 | 8.8 | |

| 13:15 | CAD | Housing Starts Nov | 216K | 198K | 206K | 207K |

| 13:30 | CAD | Building Permits M/M Oct | -0.20% | -0.20% | 0.40% |