{kind=link}

Dollar is trying to recover again today, with rather weak momentum so far. FOMC minutes released overnight didn’t prompt renewed selling in the greenback. Instead, traders are turning cautious ahead of the highly anticipated meeting between Trump and China Xi in Argentina. For now, Yen is the second strongest one for today, following Kiwi. Swiss Franc is the weakest one today with Australian Dollar. Euro and Sterling are mixed.

Technically, the forex markets are generally in consolidative mode. EUR/USD is in range of 1.1267/1472. USD/CHF is in range of 0.9908/1.0006. GBP/USD is in range of 1.2725/2927. Even the strong AUD/USD couldn’t get ride of 0.7314 resistance cleanly. EUR/AUD breached 1.5519 support yesterday but there was no follow through selling. GBP/JPY is bounded in range of 144.02/145.99. EUR/GBP is also held in range below 0.8939 resistance.

In other markets, major US indices closed slightly lower overnight DOW was down -0.11%, S&P 500 down -0.22% and NASDAQ down -0.25%. Treasury yield also closed slightly lower with 10-year yield down -0.009 at 3.035. Asian indices are mildly higher but trading is subdued. Nikkei is up 0.39% at the time of writing. Singapore Strati Times up 0.53%. Hong Kong HSI and China SSE are up 0.69% and 0.23% respectively.

Dollar mixed after FOMC minutes, no more follow through selling

Dollar is mixed after FOMC minutes revealed nothing new, nothing special. The greenback was sold off earlier this week after Fed Chair Jerome Powell’s comment that interest rate is “just below” neutral. However, there was no follow through selling since then. Dollar is still trading up against Yen, Sterling and Canadian for the week.

The FOMC minutes for the November revealed that the members still considered a rate hike in December is appropriate. Yet, they debated on the change in forward guidance regarding the pledge on “further gradual increases” in the policy rate. Some judged that the policy rate is near to the neutral level, while some suggested stressing the importance of incoming data on monetary policy decision. The members in general were upbeat on the economic developments. Yet, they were concerned about the negative impacts of Trump’s imposition of trade tariff on the economy, as well as the “volatility in equity markets was accompanied by a rise in risk spreads on corporate debt”. More in FOMC Minutes Signals Rate Hike “Fairly Soon”, Policy Outlook Masked by Tariff and Debts.

More suggested reading on FOMC.

- Northern Exposure: FOMC to Press on with Hikes, Cautiously

- FOMC Minutes – Flexible is the New Gradual

- Minutes of the Federal Open Market Committee November 7-8, 2018

Trump tries to sound hardline ahead of meeting with Xi

Ahead of the highly anticipated meeting with China’s Xi, Trump tried to sound hardline in his comments on the trade negotiations. He told reporters yesterday that “I think we’re very close to doing something with China but I don’t know that I want to do it.” And, “because what we have right now is billions and billions of dollars coming into the United States in the form of tariffs or taxes, so I really don’t know.” Also, “I will tell you that I think China wants to make a deal, I’m hoping to make it a deal but, frankly, I like the deal we have right now.”

UK PM May focused on getting parliament vote on Brexit, not plan B

On her way to G20 summit in Argentina, UK Prime Minister Theresa May said she’s focusing on the Brexit vote in the Parliament rather than a plan B. She said, “The focus of myself and the government is on the vote that is taking place on Dec. 11. We will be explaining to members of parliament why we believe that this is a good deal for the UK.”

And, she added “I ask every member of parliament to think about delivering on the Brexit vote and doing it in a way that is in the national interest and doing it in a way that is in the interests of their constituents because it protects jobs and livelihoods.” Also, “We haven’t had the vote yet. Let’s focus on the deal that we have negotiated with the European Union.”

Japan industrial production rose 2.9%, strongest since Jan 2015

Japan industrial production rose strongly by 2.9% mom in October, way above expectation of 1.2% mom. It’s also more than enough to reverse the -0.4% mom contraction in September. Besides, it’s the fastest month-on-month gain since January 2015. Nevertheless, it’s noted by economists that the strong reading was mainly a reaction to supply-chain disruptions caused by natural disasters. The rebound should be considered a one-off and outlook remains dim ahead on global slowdown.

Also from Japan, unemployment rate edged up to 2.4% in October, above expectation of 2.3%. Tokyo CPI core was unchanged at 1.0% yoy in November, matched expectations.

Release in Asian session, China PMI manufacturing dropped -0.2 to 50 in November. PMI non-manufacturing dropped -0.5 to 53.4. Australia Private sector credit rose 0.4% mom in October. New Zealand building permits rose 1.5% mom in October. UK Gfk consumer sentiment dropped -2 to -13 in November.

Looking ahead

Swiss will release KOF leading indicator in European session. Eurozone will release November CPI flash and unemployment rate. Canadian data will take center stage later in the day with GDP, IPPI and RMPI. US will also release Chicago PMI.

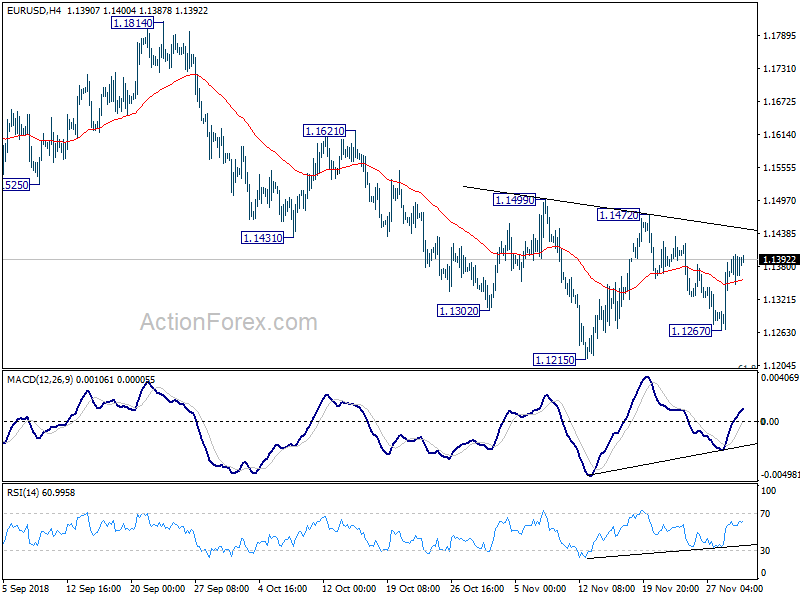

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1361; (P) 1.1381; (R1) 1.1415; More…..

EUR/USD is still bounded in range of 1.1267/1472 and intraday bias remains neutral first. On the upside, decisive break of 1.1472 resistance will complete a head and shoulder bottom pattern (ls: 1.1302; h: 1.1215; rs: 1.1267). That will indicate near term reversal and bring stronger rise back to 1.1814 resistance. On the downside, below 1.1267 will turn bias back to the downside for 1.1215 low.

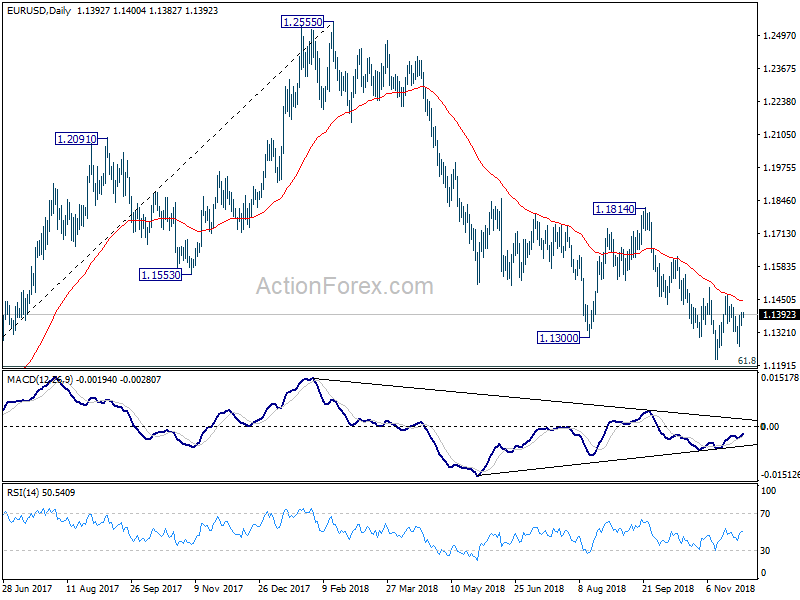

In the bigger picture, down trend from 1.2555 medium term top is still in progress and should target 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 next. Sustained break there will pave the way to retest 1.0339. On the upside, break of 1.1814 resistance is now needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Oct | 1.50% | -1.50% | -1.30% | |

| 23:30 | JPY | Jobless Rate Oct | 2.40% | 2.30% | 2.30% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | 1.00% | 1.00% | 1.00% | |

| 23:50 | JPY | Industrial Production M/M OCt P | 2.90% | 1.20% | -0.40% | |

| 0:01 | GBP | GfK Consumer Confidence Nov | -13 | -11 | -10 | |

| 0:30 | AUD | Private Sector Credit M/M Oct | 0.40% | 0.40% | 0.40% | |

| 1:00 | CNY | Manufacturing PMI Nov | 50 | 50.2 | 50.2 | |

| 1:00 | CNY | Non-manufacturing PMI Nov | 53.4 | 53.8 | 53.9 | |

| 5:00 | JPY | Consumer Confidence Index Nov | 43.3 | 43 | ||

| 5:00 | JPY | Housing Starts Y/Y Oct | 0.20% | -1.50% | ||

| 8:00 | CHF | KOF Leading Indicator Nov | 99.8 | 100.1 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Oct | 8.00% | 8.10% | ||

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Nov | 2.10% | 2.20% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov A | 1.10% | 1.10% | ||

| 13:30 | CAD | GDP M/M Sep | 0.10% | |||

| 13:30 | CAD | Industrial Product Price M/M Oct | 0.10% | |||

| 13:30 | CAD | Raw Materials Price Index M/M Oct | -0.90% | |||

| 14:45 | USD | Chicago PMI Nov | 58.5 | 58.4 |