{kind=link}

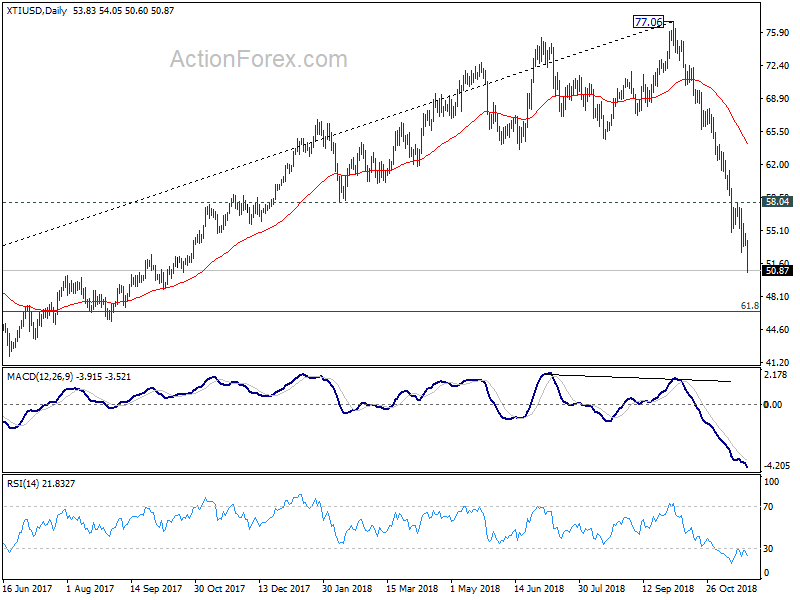

Yen rises broadly today as risk aversion is back. Chinese stocks dived sharply in otherwise quiet Asian session. The Shanghai SSE closed down -2.49% at 2579.48 has likely completed recent corrective rebound. European indices also reversed initial gain and are trading broadly lower at the time of writing. Weak Eurozone PMI data is a factor weighing down sentiments. In the background, WTI crude oil is extending recent free fall and hits as low as 50.60. 50 psychological level is now in touching distance.

Back to the currency markets, Dollar and Swiss Franc are following as the second and third strongest for now. New Zealand Dollar is the weakest one for today, followed by Euro and the Sterling. The lift by UK-EU political declaration was rather brief. Focuses will turn to whether EU27 leaders, including Spain, would approve the Brexit withdrawal agreement this Sunday. For the week, Swiss Franc remains the strongest one, followed by Yen and then Sterling. Australian, New Zealand and Canadian Dollar are the weakest.

In other markets, FTSE is now down -1.1%, DAX is down -0.73%, CAC is down -0.63%. German 10 year yield is down -0.0303 at 0.343. Italian 10 year yield is down -0.004 at 3.437. Earlier today, Nikkei rose 0.65%, Hong Kong HSI rose 0.18%, Singapore Strait Times rose 0.09%. But China Shanghai SSE dropped -0.23%.

Eurozone PMI composite dropped to 47-month low, Q3 weakness not just a blip

Eurozone PMI manufacturing dropped to 51.5 in November, down from 52.0, missed expectation of 52.0. That’s the lowest reading in 30 months. PMI services dropped to 53.1, down from 53.7 and missed expectation of 53.6. That’s the lowest reading in 25 months. PMI composite dropped to 52.4, down from 53.1, lowest in 47 months.

Chris Williamson, Chief Business Economist at IHS Markit said November’s reading “brought further signs that the manufacturing-led slowdown is spilling over to services”. And, the data suggest that “weakness of GDP in the third quarter may not have been a blip, and that the underlying trend is one of slower economic growth”. The reading indicates 0.3% GDP growth in Q4, but “forward-looking indicators such as new orders and future expectations remaining worryingly subdued.”

Also release, Germany PMI manufacturing dropped to 51.6 in November, down from 52.2 and missed expectation of 52.2. That’s the lowest level in 32 months. PMI services dropped to 53.3, down from 54.7 and missed expectation of 54.5. PMI composite dropped to 52.2, down from 53.4, hit a 47-month low. Germany Q3 GDP was finalized at -0.2% qoq.

France PMI manufacturing dropped to 50.7 in November down from 51.2 and missed expectation of 51.3. That’s the lowest in 26 months. PMI services dropped to 55.0, down from 55.3 and matched expectations. PMI composite dropped to 54.0, down from 54.1.

Canadian Dollar ignores CPI and retail sales, tumbles as WTI crude oil diving to 50

Canada headline CPI accelerated to 2.4% yoy in October, up from 2.2% yoy and beat expectations of 2.2% yoy. CPI core was unchanged at 1.9% yoy. CPI core median was unchanged at 2.0% yoy. CPI core trim was also unchanged at 2.1% yoy. Looking at the details, prices rose in all major components. Headline retail sales rose 0.2% mom in September, above expectation of 0.0% mom. But ex-auto sales rose 0.1% mom only, below expectation of 0.30%.

Canadian Dollar drops sharply after the release, mainly as delayed reaction to the free fall in oil prices. WTI crude oil is now heading to 50 psychological level. And overall, we maintain the view that WTI’s fall from 77.06 is a medium term decline. Further fall would likely be seen to 61.8% retracement of 27.69 to 77.06 at 46.54 before bottoming.

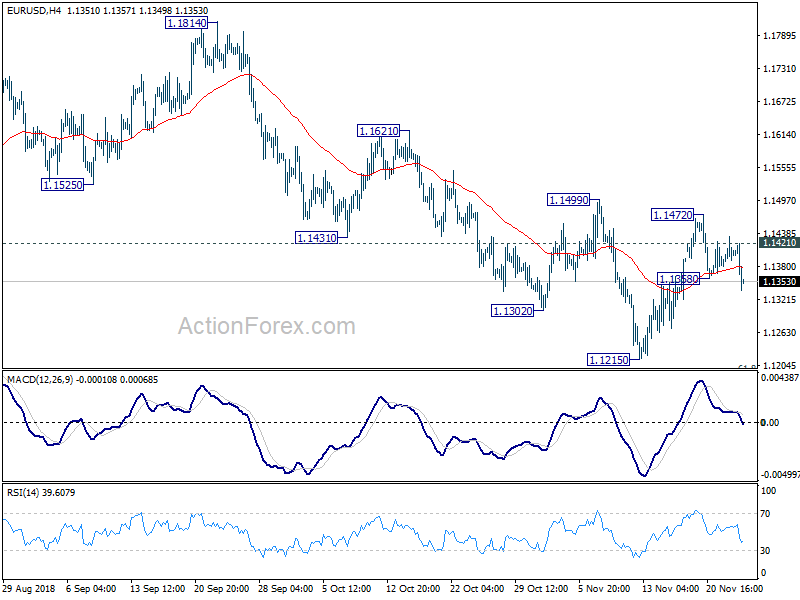

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1378; (P) 1.1407; (R1) 1.1432; More…..

EUR/USD’s break of 1.1358 suggests that fall from 1.1472 has resumed. Intraday bias is turned back to the downside for 1.1215 low first. Decisive break there will resume medium term down trend. On the upside, above 1.1421 will turn intraday bias neutral again. Overall, near term outlook stays bearish as long as 1.1499 resistance holds and further decline is expected.

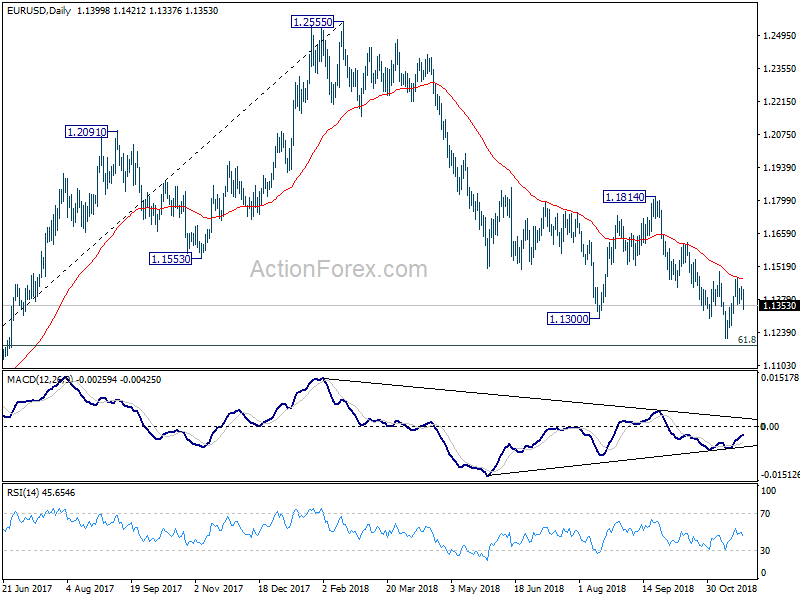

In the bigger picture, down trend from 1.2555 medium term top has just resumed and should target 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 next. Sustained break there will pave the way to retest 1.0339. On the upside, break of 1.1814 resistance is now needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | German GDP Q/Q Q3 F | -0.20% | -0.20% | -0.20% | |

| 08:15 | EUR | France Manufacturing PMI Nov P | 50.7 | 51.3 | 51.2 | |

| 08:15 | EUR | France Services PMI Nov P | 55 | 55 | 55.3 | |

| 08:30 | EUR | Germany Manufacturing PMI Nov P | 51.6 | 52.2 | 52.2 | |

| 08:30 | EUR | Germany Services PMI Nov P | 53.3 | 54.5 | 54.7 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Nov P | 51.5 | 52 | 52 | |

| 09:00 | EUR | Eurozone Services PMI Nov P | 53.1 | 53.6 | 53.7 | |

| 13:30 | CAD | Retail Sales M/M Sep | 0.20% | 0.00% | -0.10% | 0.00% |

| 13:30 | CAD | Retail Sales Ex Auto M/M Sep | 0.10% | 0.30% | -0.40% | |

| 13:30 | CAD | CPI M/M Oct | 0.30% | 0.10% | -0.40% | |

| 13:30 | CAD | CPI Y/Y Oct | 2.40% | 2.20% | 2.20% | |

| 13:30 | CAD | CPI Core Y/Y Oct | 1.90% | 1.90% | 1.90% | |

| 13:30 | CAD | CPI Core – Median Y/Y Oct | 2.00% | 2.00% | 2.00% | |

| 13:30 | CAD | CPI Core – Trim Y/Y Oct | 2.10% | 2.10% | 2.10% | |

| 14:45 | USD | US Manufacturing PMI Nov P | 55.8 | 55.7 | ||

| 14:45 | USD | US Services PMI Nov P | 55 | 54.8 |