{kind=link}

Overall, market sentiments stabilized today as started in Asian session. With the help of rebound in Asian and strengthen Europe, US stocks are set to open higher to pare some of yesterday’s steep losses. As a result, New Zealand and Australian Dollar are the strongest ones for today so far, followed by Euro. The common currency is rather resilient today even though European Commission has started step one in preparation for disciplinary action on Italy over its budget. On the other hand, Yen turns weaker, followed by Dollar and then Sterling. The greenback is weighed further down by disappointing US data.

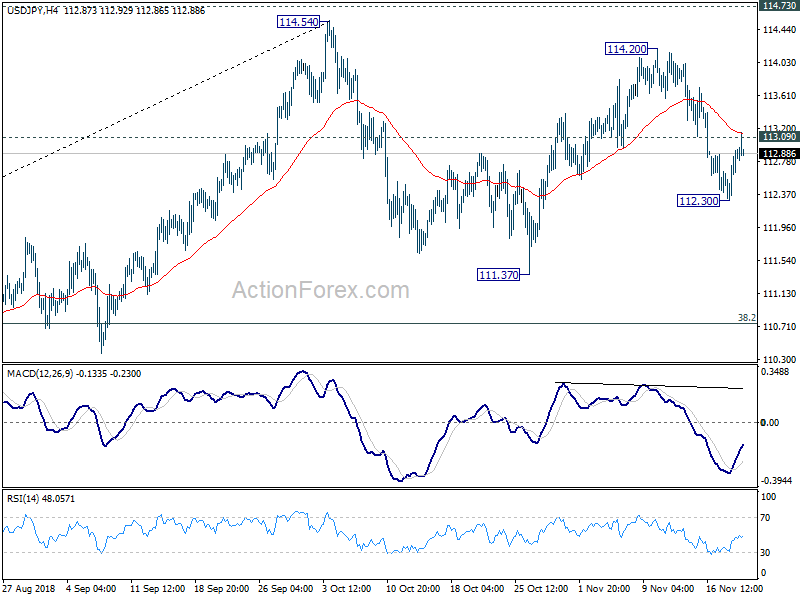

Technically, despite breaching 113.09 minor resistance, USD/JPY quickly retreats. EUR/USD also recovers back above 1.14. For now, there is no sign of a sustainable comeback in Dollar yet. Indeed, AUD/USD is now quietly turning focus back to 0.7314 key resistance. Sustained break there will carry medium term bullish implications.

In Europe, at the time of writing, FTSE is up 1.10%, DAX is up 0.98%, CAC is up 0.56%. German 10 year yield is up 0.0094 at 0.364. Italy 10 year yield is down -0.111 at 3.507. German-Italian spread remains above 310. In Asia, Nikkei close down -0.35%. But Hong Kong HSI, China Shanghai SSE and Singapore Strait Times were all up, by 0.51%, 0.21% and 0.39% respectively. Japan 10 year JGB yield dropped -0.0094 to 0.094, back below 0.1%.

US initial jobless claims rose to 224k, durables dropped -4.4%

Initial jobless claims rose 3k to 224k in the week ended November 17, above expectation of 215k. Four-week moving average of initial claims rose 2k to 218.5k. Continuing claims dropped -2k to 1.668M in the week ended November 10. Four-week moving average of continuing claims rose 7.5k to 1.650M. Headline durable goods orders dropped sharply by -4.4% in October, missed expectation of -2.5%. Ex-transport orders rose just 0.1%, missed expectation of 0.4% too.

Also released today, Canada wholesale sales dropped -0.5% mom in September. UK public sector net borrowing jumped GBP 8B in October. Australia Westpac leading index rose 0.1% mom in October. Japan all industry activity index dropped -0.9% mom.

European Commission: Italy’s 2019 budget a serious case of non-compliance, Excessive Deficit Procedure warranted

The European Commission confirms in a statement today the “existence of a particularly serious case of non-compliance” with EU’s recommendation in Italy’s Draft Budget Plan. The Commission has “carried out a new assessment of the prima facie lack of compliance with the debt criterion The new assessment was necessary because “Italy’s fiscal plans for 2019 represent a material change in the relevant factors analysed by the Commission last May.”

The Commission also noted that (i) the fact that macroeconomic conditions, despite recently intensified downside risks, cannot be argued to explain Italy’s large gaps to compliance with the debt reduction benchmark, given nominal GDP growth above 2% since 2016; (ii) the fact that the government plans imply a marked backtracking on past growth-enhancing structural reforms, in particular the past pension reforms; and above all (iii) the identified risk of significant deviation from the recommended adjustment path towards the medium-term budgetary objective in 2018 and the particularly serious non-compliance for 2019 with the recommendation addressed to Italy by the Council on 13 July 2018, based on both the government plans and the Commission 2018 autumn forecast.

European Commission Vice President Valdis Dombrovskis confirmed debt criterion should be considered as not complied and a “debt-based Excessive Deficit Procedure is thus warranted” for Italy. He emphasized that “Euro area countries are in the same team and should be playing by the same rules.” And, “these rules are there to protect us. They provide certainty, stability and mutual trust.”

Economics commissioner Pierre Moscovici tweeted that “Today is not yet the opening of an EDP. First the Member States must give their views within two weeks, then the @EU_Commission will have to prepare the procedure, including a new recommendation for Italy to correct its deficit and debt trajectory.” Also, “Our door remains open to dialogue with Italy. As we move closer to opening an Excessive Deficit Procedure, it is even more essential that the Italian authorities engage constructively with the @EU_Commission.”

Italian Prime Minister Giuseppe Conte insisted that the 2019 budget is “excellent”. He’s expected to meet European Commission President Jean-Claude Juncker on Saturday. Conte added “during the course of the conversation we will finally have the chance to talk in detail and fully explain this budget.”

Italy Istat lowers 2018 and 2019 GDP forecasts

Italy’s Istat, National Institute of Statistics, revised down both 2018 and 2019 GDP growth forecasts. For 2018, growth is projected to be at 1.1%, down from May’s forecast of 1.4%. For 2019, growth is projected to be at 1.3%. Istat noted that “this projections take into account the less favourable international framework and the expansionary fiscal policies implemented in the 2018 Budget Law.”

Istat’s forecast for 2019 is notably lower than the coalition government’s overly optimistic 1.5%. But it’s higher than European Commission’s 1.2% and IMF’s 1.0%. GDP forecast is a key figure in Italy’s draft budget plan.

USTR: China has not fundamentally altered its unfair practices

The US Trade Representative released an update on Section 301 IP investigation on China yesterday. Less than two weeks ahead of the Trump-Xi meeting as sideline of G20 summit in Argentina, USTR is piling more pressure on China for reforms. In short, the report complained that “China has not fundamentally altered its unfair, unreasonable, and market-distorting practices that were the subject of the March 2018 report on our Section 301 investigation.”

The report also noted that “despite repeated U.S. engagement efforts and international admonishments of its trade technology transfer policies, China did not respond constructively and failed to take any substantive actions to address U.S. concerns.” And, China, “made clear – both in public statements and in government-to-government communications – that it would not change its policies in response to the initial Section 301 action.” The report also said “China largely denied there were problems with respect to its policies involving technology transfer and intellectual property”.

OECD: Growth peaked, prepare for soft landing, and beware of trade war

OECD said in a report released today that global growth has already peaked and it’s now set for a “soft landing”. And, the global economy is navigating “rough seas” with “downside risks abound”. It also noted that “policy makers will have to steer their economies carefully towards sustainable, albeit slower, GDP growth.” The organization also pointed out that “global trade and investment have been slowing on the back of increases in bilateral tariffs while many emerging market economies are experiencing capital outflows and a weakening of their currencies”. OECD also warned that ” accumulation of risks could create the conditions for a harder-than-expected landing”. And the risks include firstly, further trade tensions, secondly, tightening financial conditions and thirdly, a sharp slowdown in China.

For 2019, global growth forecasts was revised down to 3.5% and stay there in 2020. US growth was left unchanged at 2.7% in 2019 and then slow to 2.1% in 2020. Eurozone growth was revised down to 1.8% in 2019 then slow further to 1.6% in 2020. Japan growth would accelerate to 1.0% in 2019, an upward revision, but slow to 0.7% in 2020. China’s growth is projected t slow to 6.3% in 2019, downwardly revised, and then further to 6.0% in 2020.

OECD Secretary-General Angel Gurría warned that “trade conflicts and political uncertainty are adding to the difficulties governments face in ensuring that economic growth remains strong, sustainable and inclusive.” And, “we urge policy-makers to help restore confidence in the international rules-based trading system and to implement reforms that boost growth and raise living standards – particularly for the most vulnerable.”

According to OECD, trade tensions have already shaved between 0.1-0.2% from global GDP this year. If US raise tariffs on all Chinese goods to 25%, world economy growth could fall to just 3.0% in 2020, no more 3.5%. And, growth in the US could drop by -0.8% and by -0.6% in China.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.39; (P) 112.61; (R1) 112.97; More..

USD/JPY breached 113.09 resistance briefly but failed to sustain above yet. Intraday bias stays neutral first. Another fall is mildly in favor. On the downside, below 112.30 will resume the fall from 114.20 to 111.37 support. Such decline is seen as the third leg of the consolidation pattern from 114.54. Downside should be contained by 38.2% retracement of 104.62 to 114.54 at 110.75 to bring rebound. On the upside, firm break of 113.03 minor resistance will turn bias back to the upside for 114.54/73 key resistance zone.

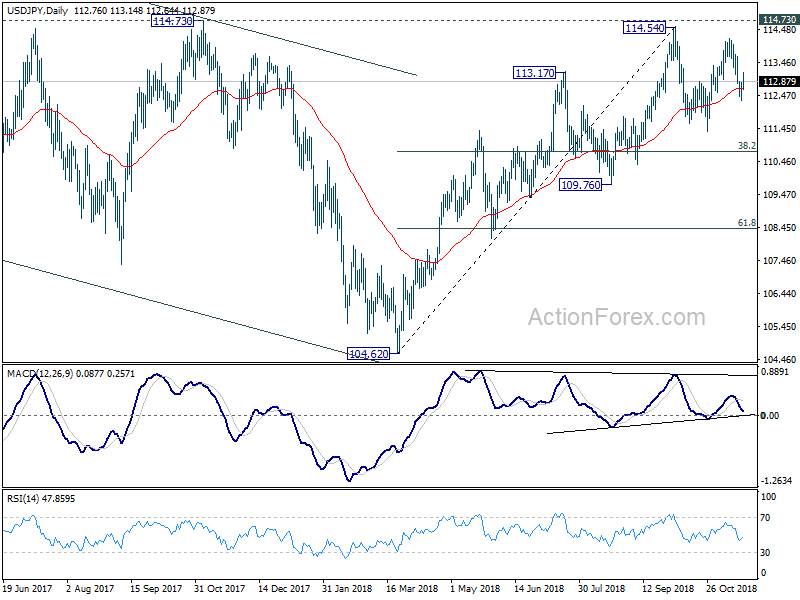

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.76 support holds. However, decisive break of 109.76 will dampen this bullish view and turns outlook mixed again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Oct | 0.10% | -0.10% | 0.00% | |

| 04:30 | JPY | All Industry Activity Index M/M Sep | -0.90% | -0.90% | 0.50% | 0.40% |

| 09:30 | GBP | Public Sector Net Borrowing Oct | 8.0B | 5.6B | 3.3B | 2.0B |

| 13:30 | CAD | Wholesale Trade Sales M/M Sep | -0.50% | 0.40% | -0.10% | |

| 13:30 | USD | Durable Goods Orders Oct P | -4.40% | -2.50% | 0.70% | |

| 13:30 | USD | Durables Ex Transportation Oct P | 0.10% | 0.40% | 0.00% | |

| 13:30 | USD | Initial Jobless Claims (NOV 17) | 224K | 215K | 216K | 221K |

| 15:00 | USD | Leading Index Oct | 0.10% | 0.50% | ||

| 15:00 | USD | Existing Home Sales Oct | 5.20M | 5.15M | ||

| 15:00 | USD | U. of Mich. Sentiment Nov F | 98.3 | 98.3 | ||

| 15:30 | USD | Crude Oil Inventories | 2.5M | 10.3M | ||

| 17:00 | USD | Natural Gas Storage | -105B | 39B |