{kind=link}

Sterling is sold off broadly today as Brexit optimism quickly turned into political turmoil. UK Prime Minister Theresa May appeared to have secured Cabinet support on her Brexit agreement with EU. But in less than 24 hours, four ministers resigned in protest, including the high profile figure in Brexit Minister Dominic Raab. That’s not the end of it though.

ERG chair Jacob Rees-Mogg is sending a letter to Sir Graham Brady, chair of the 1922 Committee, requesting a no confidence vote. Rees-Mogg expects 48 letters to come in to trigger the vote, though not necessarily today. And, leadership contest could happen quickly in weeks. That would definitely overlap with the scheduled EU summit for Brexit on November 25. It feels like it’s just the start of another stage of problem for the Pound.

Staying in the currency markets, Sterling is in no doubt the weakest one today, followed by Euro and then Dollar. Australian Dollar is the strongest one as supported by strong employment data, as well as hope for progress in US-China trade negotiations. The Aussie is followed by Yen, and then New Zealand Dollar.

Technically, EUR/GBP rebound and break of 0.8773 minor resistance now suggests near term reversal and focus is back on 0.8939 resistance. GBP/JPY’s break of 145.99 minor support should confirm rejection by 149.70 resistance earlier, and deeper fall should be seen back to 142.76 support. GBP/USD is also heading back to 1.2692 support. Otherwise, dollar are generally in consolidations, and we’ll see how long the consolidations would extend.

Little attention paid to the data released in European and US session

Released from the US, headline retail sales rose 0.8% in October, above expectation of 0.5% mom. Ex-auto sales rose 0.7%, above expectation of 0.5 mom. Import price index rose 0.5% mom in October, much higher than expectation of 0.1% mom. Empire State Manufacturing index rose to 23.3 in November, up from 21.1 and beat expectation of 19.3. Philly Fed Business outlook dropped to 12.9, down from 22.2, below expectation of 20.7. Initial jobless claims rose 2k to 216k in the week ended November 10. Continuing claims rose 46k to to 1.676M in the week ended November 3.

From UK, October retail sales data were rather poor. Including auto and fuel, sales dropped -0.5% mom in October versus expectation of 0.2% mom. Excluding auto and fuel, sales dropped -0.4% mom versus expectation of 0.2% mom. The Pound has enough trouble already. So we’d tend not to blame the selloff on retail sales data. From Eurozone, trade surplus narrowed to EUR 13.4B in September, below expectation of EUR 16.7B.

While the data were important, markets paid little attention.

UK PM May in political turmoil for her Brexit agreement

UK Brexit Secretary Dominic Raab resigns today, just after Prime Minister Theresa May seemed to have got Cabinet support on her Brexit plan. Raab complained that “Above all, I cannot reconcile the terms of the proposed deal with the promises we made to the country in our manifesto at the last election.” Raab also warned in his resignation letter “no democratic nation has ever signed up to be bound by such an extensive regime, imposed externally without any democratic control over the laws to be applied, nor the ability to decide to exit the arrangement.” And he emphasized that “this is, at its heart, a matter of public trust,” and “I cannot support the proposed deal.”

Nevertheless, Raab suggested he retained confidence in May as PM later in the day. He told BBC that “I think she needs a Brexit secretary that will pursue the deal that she wants to put to the country with conviction. I don’t feel I can do that in good conscience. But I respect her, I hold her in high esteem, I think she should continue, but I do think we need to change course on Brexit.”

In addition to Raab, Welfare Minister Esther McVey, junior Northern Ireland Minister Shailesh Vara, junior Brexit Minister Suella Braverman also resigned.

Prime Minister Theresa May responded to the resignations by warning that “The choice is clear: We can choose to leave with no deal, we can risk no Brexit at all, or we can choose to unite and support the best deal that can be negotiated.” And she also said “We have been preparing for no-deal and we continue to prepare for no-deal because I recognize that we have a further stage of negotiation with the European council and then that deal when finalised … has to come back to this House.”

In his letter to Sir Graham Brady, chair of the 1922 Committee, Chair of the European Research Group (ERG), Jacob Rees-Mogg criticized that “the draft withdrawal agreement presented to parliament today has turned out to be worse than anticipated and fails to meet the promises given to the nation by the prime minister, either on her own account or on behalf of us all in the Conservative party manifesto.”

And, “It is of considerable importance that politicians stick to their commitments or do not make such commitments in the first place. Regrettably, this is not the situation, therefore, in accordance with the relevant rules and procedures of the Conservative party and the 1922 committee this is a formal letter of no confidence in the leader of the party, the Rt. Hon. Theresa May.”

China made formal concessions to US on trade, but concerns remain

Chinese and Hong Kong stocks surged today on reports that China has sent written responses to the US regarding the concessions it’s willing to made. That could pave the way for some sort of agreement during Xi-Trump meeting at the G20 summit on November 30. The act is generally seen as constructive for the trade negotiations.

However, concerns remain as most of China described in the documents were just old wine in a new bottle. They’re just recap of what Xi Jinping has announced recently, such case raising the equity caps on foreign investments in some industries. There is so far nothing substantial regarding opening of the markets and removing barriers on trade and investments. Mostly likely too, there wasn’t anything regarding the highly criticized dominance of State-Owned Enterprises in the country.

Further more, at this point, Treasury Secretary Steven Mnuchin is the one handling the discussion with China. Even if White House economic advisor Larry Kudlow would be involved, they remain far from the stage of making a trade deal. The work of trade agreements fall into the area of trade representative Robert Lighthizer. And, not until Lighthizer is involved, there would only be ceasefire, but no constructive progress.

Fed Powell: From now on, Fed can and will move at any meeting

Fed Chair Jerome Powell had an hour long exchange with Dallas Fed President Robert Kaplan, titled “Global Perspectives with Jerome H. Powell“. Powell reiterated his upbeat comments on the US economy. He said “I’m very happy about the state of the economy now”. He also hailed the Fed collectively and said “our policy is part of the reason why our economy is in such a good place right now.”

A key take away is his comments regarding the arrangement of having press conference after all eight FOMC meetings during the year, starting next. He said “certainly all meetings are live now, there’s no question about it now.” And he added, “over time, folks will get used to the idea that we can and will move at any meeting.”

On interest rates, Powell acknowledged the need to thing about “how much further to raise rates and the pace at which we will raise rates.” And, “the way we will be approaching that is to be looking really carefully at how the markets and the economy and business contacts will be reacting to our policy.” He emphasized that “our goals will be to extend the recovery … and to keep unemployment low and inflation low. So that’s how we’re going to think about it.”

On headwinds, Powell noted slowing growth abroad, waning effect of the administration’s tax cuts and spending increases are some that the economy might face. Also, he noted that there are a lot of factors weighing on home building too.

Australia employment jumped 32.8k, with strong growth in full-time jobs

Australia employment rose 32.8k in October, much better than expectation of 20.3k. Full-time employment jumped 42.3k to 8.70M. Part-time jobs dropped -9.5k to 3.97M. Unemployment rate was unchanged at 5.0%, below expectation of 5.1%. Participation rate rose 0.1% to 65.6%. Monthly worked hours in all jobs also rose 0.3%. Released yesterday, wages grew 2.3% in Q3, fastest annual pace in three years. The overall set of employment data released this week is pretty encouraging.

The set of data should be very welcomed by the RBA. However, they kind of just confirmed RBA’s outlook, without too much out-performance. Wage growth remains the key for lifting inflation. And there’s still much more work to do. Nevertheless, it’s a step in the right direction and affirmed that the next move is a hike rather than a cut. But, that leaves RBA with no urgency to move any time soon.

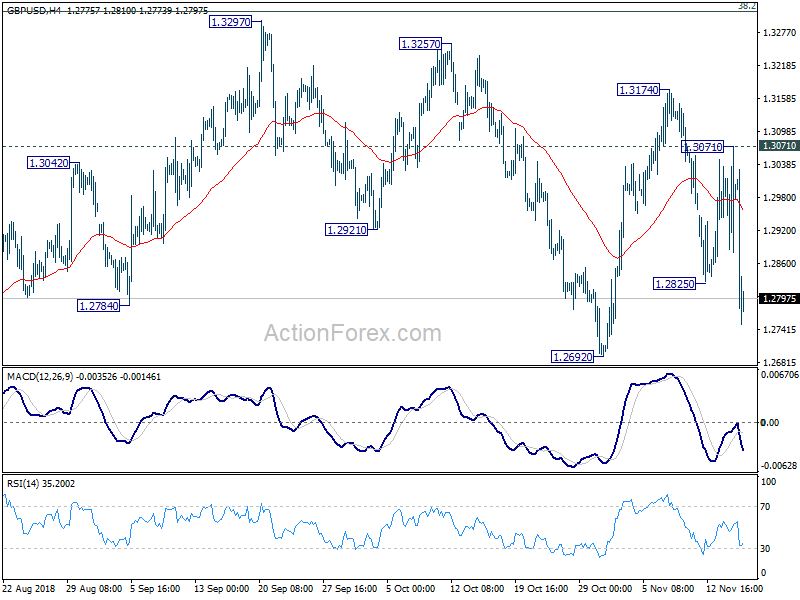

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2888; (P) 1.2980; (R1) 1.3081; More…

GBP/USD dives to as low as 1.2750 so far today. The break of 1.2825 suggests resumption of fall from 1.3174. Intraday bias is back on the downside for retesting 1.2661/92 key support zone. Decisive break there will resume larger down trend from 1.4376. On the upside, break of 1.3071 will bring another rebound. But upside should be limited by t 1.3316 fibonacci level. Overall, price actions from 1.2661 are viewed as a consolidation pattern. Down trend from 1.4376 should resume after completion of the consolidation.

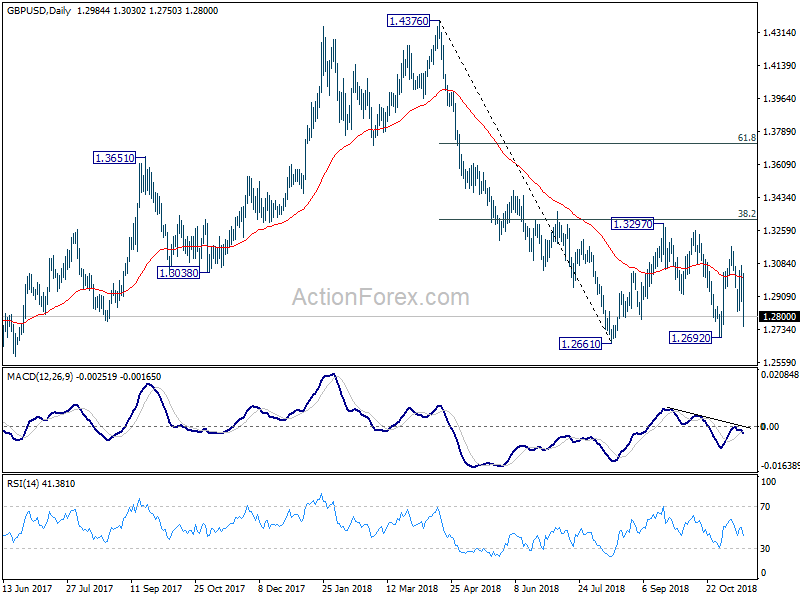

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectation Nov | 3.60% | 4.00% | ||

| 00:30 | AUD | Employment Change Oct | 32.8K | 20.3K | 5.6K | 7.8K |

| 00:30 | AUD | Unemployment Rate Oct | 5.00% | 5.10% | 5.00% | |

| 09:30 | GBP | Retail Sales Inc Auto Fuel M/M Oct | -0.50% | 0.20% | -0.80% | -0.40% |

| 09:30 | GBP | Retail Sales Inc Auto Fuel Y/Y Oct | 2.20% | 2.80% | 3.00% | 3.30% |

| 09:30 | GBP | Retail Sales Ex Auto Fuel M/M Oct | -0.40% | 0.20% | -0.80% | -0.30% |

| 09:30 | GBP | Retail Sales Ex Auto Fuel Y/Y Oct | 2.70% | 3.30% | 3.20% | 3.60% |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | 13.4B | 16.7B | 16.6B | 16.8B |

| 13:30 | CAD | ADP Non-Farm Employment Change Oct | -23.0K | 28.8K | ||

| 13:30 | USD | Retail Sales Advance M/M Oct | 0.80% | 0.50% | 0.10% | |

| 13:30 | USD | Retail Sales Ex Auto M/M Oct | 0.70% | 0.50% | -0.10% | |

| 13:30 | USD | Empire State Manufacturing Nov | 23.3 | 19.3 | 21.1 | |

| 13:30 | USD | Philadelphia Fed Business Outlook Nov | 12.9 | 20.7 | 22.2 | |

| 13:30 | USD | Import Price Index M/M Oct | 0.50% | 0.10% | 0.50% | 0.20% |

| 13:30 | USD | Initial Jobless Claims (NOV 13) | 216K | 213K | 214K | |

| 15:00 | USD | Business Inventories Sep | 0.30% | 0.50% | ||

| 15:30 | USD | Natural Gas Storage | 35B | 65B | ||

| 16:00 | USD | Crude Oil Inventories | 2.9M | 5.8M |