{kind=link}

Asian stocks gapped sharply lower follow steep fall in US equities overnight. But sentiments were then lifted by optimism over US-China trade negotiations. Australian and New Zealand Dollar benefited from the development and are now trading as the strongest ones. On the other hand, Yen and Dollar turn softer, paring yesterday strong’s gains. Though for the week so far, New Zealand Dollar is the strongest, followed by US Dollar and Canadian. Euro is the worst as markets are awaiting Italy’s formal response to EU budget rejection. Sterling is the second weakest on Brexit impasse.

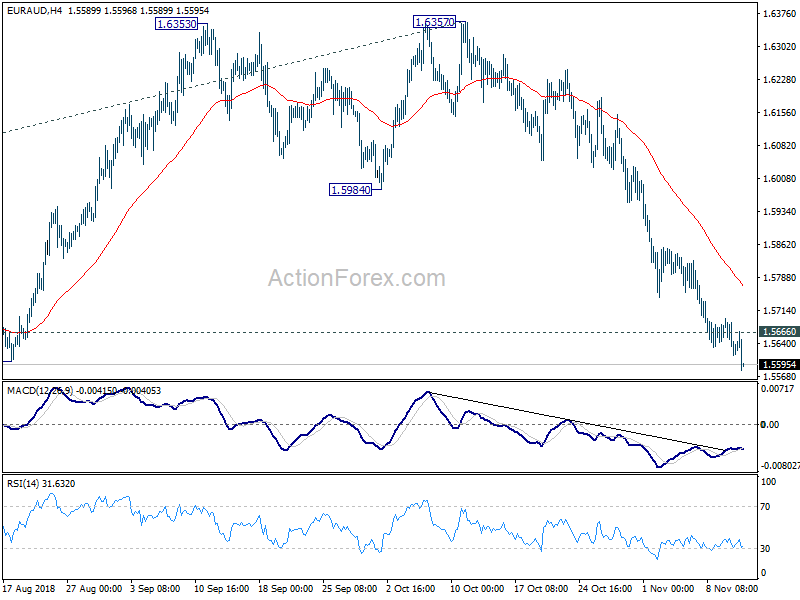

Technically, after taking out 1.1300 yesterday, there is no sign of bottoming in EUR/USD yet. Medium term down trend is in progress and should be extending to 1.1186 fibonacci level. USD/JPY continues to lose momentum ahead 114.54/73 resistance and we might see a near term reversal from there. AUD/USD breached 0.7182 support briefly but followed Asian stocks and rebound. EUR/AUD also breaks through 1.5601 structure support without much hesitation, which is quite bearish. It’s probably not the time for selloff in Aussie yet.

In other markets, DOW closed sharply lower by -602.12 pts or -2.32% at 25387.18. S&P 500 dropped -1.97% and NASDAQ declined -2.78%. Treasury yield were steady though, as 10 year yield closed down -0.003 at 3.186. In Asia, Nikkei lags behind others and is trading down -2.20%. But Hong Kong HSI staged a 500 pts reversal after gapping down. It’s now down just -0.07%. Similarly, China Shanghai SSE also dripped to as low as 2597 but it’s now at 2653, up 0.86%. Singapore Strait Times also pared back some losses and is down only -0.58%.

Asian Stocks rebound as Chinese VP Liu will visit US for trade shortly

Hong Kong stocks opened the day sharply lower with HSI hitting as low as 25092.30. That followed -2.32% decline in DOW overnight. But sentiments were then lifted by US-China trade news. The HSI just had an over 500pts swing and is now at 25060.49, down just -0.1%. AUD/USD is also lifted notably after breaching 0.7182 minor support earlier today.

It’s firstly reported that US Treasury Secretary Steven Mnuchin has resumed discussed with China Vice Premier Liu He on Friday. While there was certainly no breakthrough, it’s a positive step on preparation for Xi-Trump meeting at G20 summit on November 30.

Then, another report emerged saying that Liu would visit the US shortly to carry on with the preparations. The Hong Kong SCMP newspaper said two sources, on both sides, have confirmed the development, even though there is no final schedule yet.

Fed Daly: Premature to say Dec hike a definite, Fed not on autopilot

San Francisco Fed president Mary Daly said yesterday that her modal forecasts was for two to three more rate hikes over the next period. However, she also noted that “the exact timing not being certain”. She went further saying that it’s “premature” to say that a December rate hike is a “definite”. And, “we have a lot of time between now and December to see how the economy unfolds.”

Nevertheless, Daly still believed that Fed should gradually raise interest rates towards neutral. Her estimate of neutral rate is between 2.5 and 2.8%. For now, she’d “probably” pick the middle of the rate at around 2.7% as the neutral rate. She added that “gradual is helpful because it allows us to raise the rate, look around, evaluate, interpret the data and then, and only then, make another increase”. And, “the frequency and size of any increase I think is something that we want to continue to have open and not be on autopilot.” Also, she thought it’s premature to discuss whether interest rate need to go into restrictive region.

Her comments came after giving a speech titled “A Strong Economy—But We Can Aim Higher“. There she said that the current state of economy is “very good”. But “some people are getting left behind”. She said essentially all labor market indicates are “flashing bright green” and signaled the US labor market is “indeed at full employment”. The “key exception is continued low rates of labor force participation”. While monetary policy can’t directly cure the participation problem, Fed can help by “keeping the expansion going”. She also noted that there are “upside potential for US workforce participation”.

UK PM May: Brexit negotiations in the endgame, but significant issues remain

Addressing the lord mayor’s banquet at the Guildhall in London on Monday night, UK Prime Minister Theresa May declared that “the negotiations for our departure are now in the endgame”. She added, “we are working extremely hard, through the night, to make progress on the remaining issues in the withdrawal agreement, which are significant.”

May believed that “both sides want to reach an agreement”even though “what we are negotiating is immensely difficult:”. But she also emphasized that “this will not be an agreement at any cost”.

But no matter what May said, seeing is believing and nothing is done until 100% is done. For now, it’s still seen unlikely for the Brexit deal to be completed within November.

BoJ assets rose to JPY 553.6T, larger than Q2 GDP annualized

Latest data from BoJ showed that the central bank is holding JPY 553.6T of assets as of November 10. Among them, JPY 469.1T are Japanese government securities, accumulated through over five years of the Quantitative and Qualitative easing program.

The total assets now surpassed the countries’ GDP. Based on Q2 (April to June) data, Japan’s nominal GDP was annualized at JPY 552.8T. Q3’s data might, due on Wednesday, might come in a bit lower due to natural disasters. Nevertheless, Japan is now the first among G7 countries to own a pool of assets larger than its own GDP.

The situation drew criticism that the ultra loose monetary policy is clearly not sustainable. Some noted that BoJ would suffer losses if it would have to raise interest rate. But that’s not so much of an immediate problem. The bigger risk is that in case of real emergency, like a full blown disaster, BoJ will not be able to finance government bonds any more.

Australia business confidence dragged down by employment, wage growth constrained

Australia NAB Business Confidence dropped 2pts from 6 to 4 in October. Business Conditions also dropped 2pts from 14 to 12. Alan Oster, NAB Group Chief Economist noted that “the decline in the month was driven by weakness in the employment component – though at these levels the survey still suggests ongoing employment growth at around 20k per month. At this rate we should see recent labour market gains maintained”.

Also, it’s noted in the release that “surveyed wage bill measures and the official wage price index suggest that enough spare capacity has remained in the labour market to constrain a significant pickup in wage growth”. Hence, “September quarter wage data to be released later this week will show a small rise in the pace of growth but that overall wage growth will remain low relative to history.”

The data certainly supports the “no rush” stance of RBA.

Looking ahead

European data will be the main focus for today. UK will release employment data, including wage growth and unemployment rate. Germany will release ZEW economic sentiment and CPI final. Swiss will also release PPI.

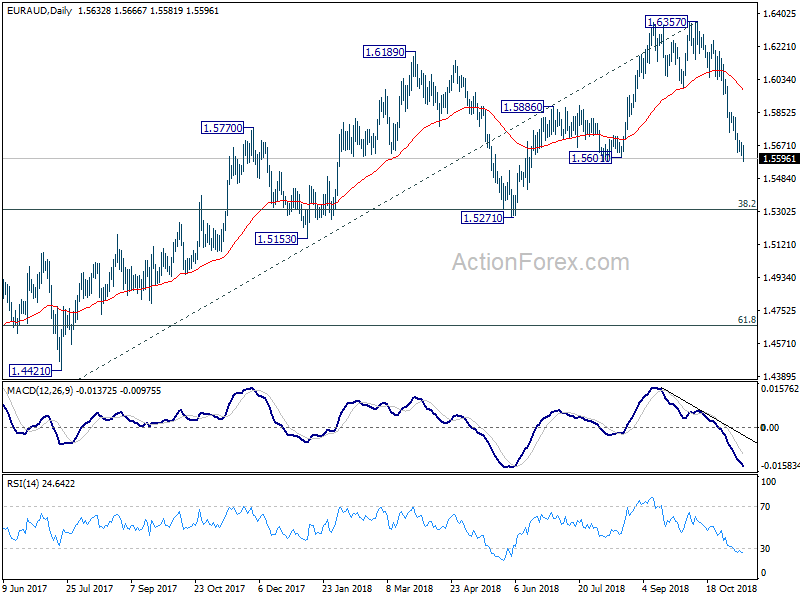

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5603; (P) 1.5649; (R1) 1.5683; More….

EUR/AUD’s decline continues today and reaches as low as 1.5581 so far. Break of 1.5601 support further affirms the case of medium term bearish reversal. Intraday bias remains on the downside for 1.5271/5313 cluster support zone next. On the upside, above 1.5666 minor resistance will turn intraday bias neutral and bring consolidations, before staging another fall.

In the bigger picture, current development argues that up trend from 1.3624 (2017 low) is possibly completed at 1.6357, ahead of 1.6587 (2015 high). This is supported by bearish divergence condition in weekly MACD. Deeper decline is now in favor to 1.5271 cluster support (38.2% retracement of 1.3624 to 1.6357 at 1.5313). Break will target 61.8% retracement at 1.4668. On the upside, break of 1.5984 support turned resistance is now needed to revive the prior medium term up trend. Otherwise, further decline will be in favor even in case of interim rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | NAB Business Confidence Oct | 4 | 6 | ||

| 0:30 | AUD | NAB Business Conditions Oct | 12 | 15 | ||

| 7:00 | EUR | German CPI M/M Oct F | 0.20% | 0.20% | ||

| 7:00 | EUR | German CPI Y/Y Oct F | 2.50% | 2.50% | ||

| 8:15 | CHF | Producer & Import Prices M/M Oct | 0.10% | -0.20% | ||

| 8:15 | CHF | Producer & Import Prices Y/Y Oct | 2.60% | |||

| 9:30 | GBP | Jobless Claims Change Oct | 4.3K | 18.5K | ||

| 9:30 | GBP | Claimant Count Rate Oct | 2.60% | |||

| 9:30 | GBP | Average Weekly Earnings 3M/Y Sep | 3.00% | 2.70% | ||

| 9:30 | GBP | Weekly Earnings ex Bonus 3M/Y Sep | 3.10% | 3.10% | ||

| 9:30 | GBP | ILO Unemployment Rate 3Mths Sep | 4.00% | 4.00% | ||

| 10:00 | EUR | German ZEW Economic Sentiment Nov | -24.2 | -24.7 | ||

| 10:00 | EUR | German ZEW Current Situation Nov | 65 | 70.1 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | -17.3 | -19.4 | ||

| 19:00 | USD | Monthly Budget Statement (USD) Oct | -116.6B | 119.1B |