{kind=link}

Dollar is making a come back as US treasury yield surged after FOMC rate decision and statement. The decision to stand pat was widely expected. One surprise was probably the lack of reference to the stock market crash in October. Fed policymakers appear to be not bothered by it at all. Five-year yield closed up 0.029 at 3.090. 10-year yield rose 0.021 to 3.234. 30-year yield, though, was just up 0.002 at 3.427. It should be noted that technically, five-year yield has breached near term resistance at 3.092. 10 year-year yield is close to 3.248 resistance with strong up side momentum. Medium term up trends in yields are very likely ready to resume and that would give Dollar more upside momentum.

Yen is also trading generally higher today thanks to risk aversion in Asia. At the time of writing, Nikkei is down -0.86%, Hong Kong HSI down -2.26%, China Shanghai SSE down -1.11% and Singapore Strait Times down -0.72%. Stocks in the US were soft with DOW closed up 0.04% only. S&P 500 and NASDAQ closed down -0.25% and -0.53% respectively. Commodity currencies are now the weakest ones for today.

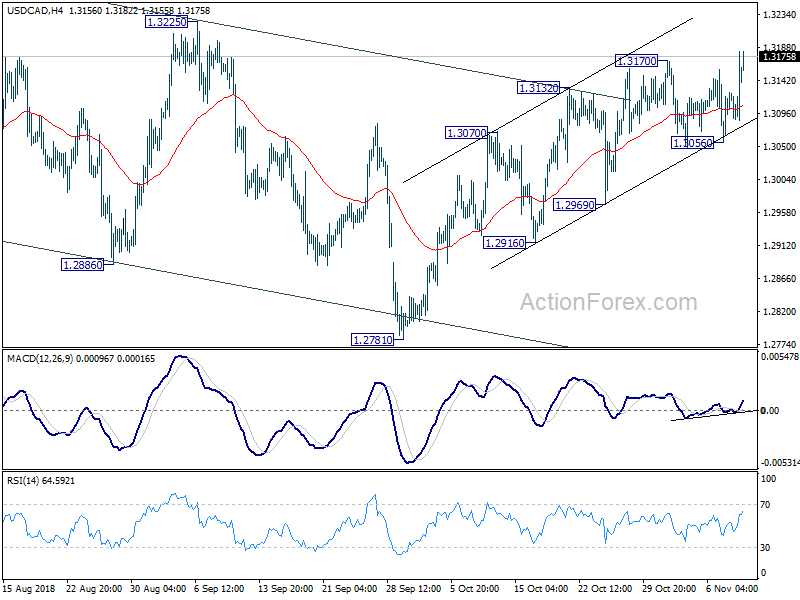

Technically, USD/JPY and USD/CAD have resumed recent rise by breaking 113.81 and 1.3170 resistance respectively. USD/CHF is on track to test 1.0094 resistance. EUR/USD’s breach of 1.1353 minor support now put 1.1300 low back into focus. More upside is now mildly in favor in Dollar. Meanwhile, AUD/USD, EUR/JPY and GBP/JPY retreat just ahead of 0.7314, 130.20 and 149.70 resistance respectively We might see, at least, deeper pull back in these three pairs for today.

Fed stands pat, on track for December hike

As widely anticipated, FOMC left the target range for the federal funds rate unchanged at 2.00-2.25% overnight. The changes in the accompanying statement were limited. This is not unusual as the November meeting is in between important ones in September and December. No press conference and updated economic projections and median dot plots are accompanied. The lack of new information, thus, would not change the expectations for a December rate hike. Still, we are hoping to get some insight from the minutes, due three weeks from now, before December. More in Limited News from FOMC, December Rate Hike Hopes Unaltered.

Also on FOMC:

- Fed Stays on the December Rate Hike Path

- FOMC Review: No change to the Fed’s hiking plans

- Fed Holds Rates Steady; December Hike Still Looks Very Likely

- FOMC Recap: 43 Days to Change 24 Words

- Fed Leaves Funds Rate Steady, Widespread Strength Means All Systems Go for a Hike in December

RBA paints better outlook, but still nowhere near rate hike

Despite painting a slightly more upbeat picture on economic outlook in the quarterly monetary statement, RBA maintained the stance that it’s no where near a move interest rate. 2018 year-average GDP growth projection was raised slightly from 3.25% to 3.50%. 2019 GDP growth projection was kept unchanged at 3.25%. Meanwhile, 2020 year-average GDP growth projection was raised slightly from 3.00% to 3.25% too. Unemployment rate is forecast to drop to 5.00% by end of 2018, stay there through 2019 and then drop further to 4.75% in by June 2020.

Headline inflation by December 2018 was raised from 1.75% to 2.00%, indicating that the temporary drag was less severe than expected. CPI would then climb further to 2.25% by December 2019 and stay there still December 2020, unrevised. Core inflation is projected to be at 1.75% by the end of 2018. Core CPI would then rise to 2.25% by December 2019, revised up from 2.00%. For December 2020, core CPI is projected to stay at 2.25%, unrevised.

RBA pointed out that “household income remains a key uncertainty around this forecast, especially in the context of high household debt and a slowing housing market.” It added further that the uncertainty is on “outlook for household income growth” and “how households may respond to significant housing price declines”.

But after all, RBA maintained that “given the expected gradual nature of that progress,” if reducing unemployment and improving inflation, “the Board does not see a strong case to adjust the cash rate in the near term.”

On the data front

Japan M2 rose 2.7% yoy in October versus expectation of 2.8% yoy. China CPI was unchanged at 2.5% yoy in October, matched expectation. China PPI slowed to 3.3% yoy, missed expectation of 3.4% yoy. Australian home loans dropped -1.0% mom in September, slightly better than expectation of -1.1% mom.

UK data will take center stage today. Q3 GDP growth is expected to accelerate to 0.6% qoq. Trade balance and productions will also be released. Later in the day, US will release PPI, wholesale inventories and U of Michigan sentiment.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3100; (P) 1.3141; (R1) 1.3196; More…

USD/CAD’s break of 1.3170 suggest that recent rebound from 1.2781 has resumed. Intraday bias is back on the upside for 1.3225 key near term resistance. Decisive break there will confirm completion of choppy fall from 1.3385 and target a retest on this high. For now, near term outlook will remain bullish as long as 1.3056 support holds, in case of retreat. But break of 1.3056 will indicate near term reversal and turn focus back to 1.2781 low.

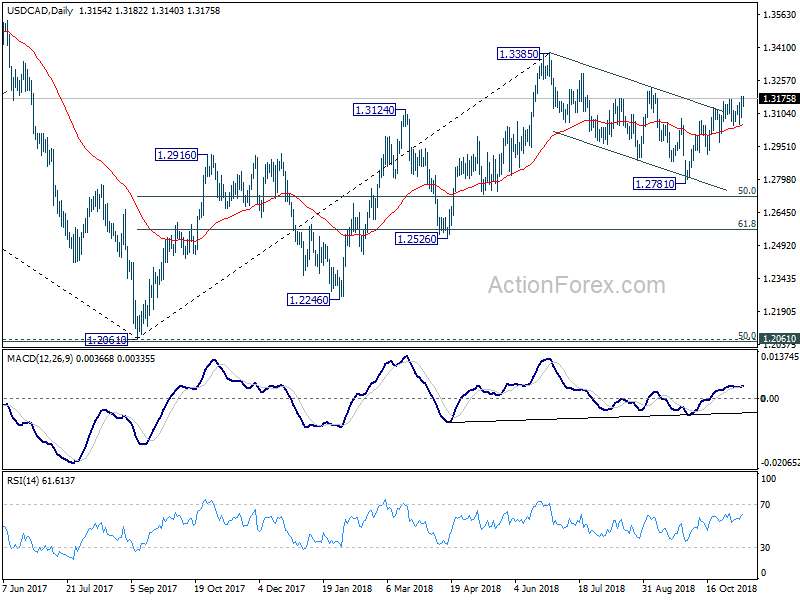

In the bigger picture, current development revives the case that corrective fall from 1.3385 has completed at 1.2781 already. And whole up trend from 1.2061 (2016 low) is ready to resume. Break of 1.3385 will target 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685. This will now be the favored case as long as 1.2781 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Oct | 2.70% | 2.80% | 2.80% | |

| 0:30 | AUD | RBA Monetary Policy Statement | ||||

| 0:30 | AUD | Home Loans M/M Sep | -1.00% | -1.10% | -2.10% | -2.20% |

| 1:30 | CNY | CPI Y/Y Oct | 2.50% | 2.50% | 2.50% | |

| 1:30 | CNY | PPI Y/Y Oct | 3.30% | 3.40% | 3.60% | |

| 9:30 | GBP | Visible Trade Balance (GBP) Sep | -11.4B | -11.2B | ||

| 9:30 | GBP | Industrial Production M/M Sep | 0.10% | 0.20% | ||

| 9:30 | GBP | Industrial Production Y/Y Sep | 0.50% | 1.30% | ||

| 9:30 | GBP | Manufacturing Production M/M Sep | 0.10% | -0.20% | ||

| 9:30 | GBP | Manufacturing Production Y/Y Sep | 0.40% | 1.30% | ||

| 9:30 | GBP | Construction Output M/M Sep | 0.20% | -0.70% | ||

| 9:30 | GBP | GDP M/M Sep | 0.10% | 0.00% | ||

| 9:30 | GBP | GDP Q/Q Q3 P | 0.60% | 0.40% | ||

| 9:30 | GBP | Index of Services 3M/3M Sep | 0.50% | 0.50% | ||

| 13:30 | USD | PPI M/M Oct | 0.20% | 0.20% | ||

| 13:30 | USD | PPI Y/Y Oct | 2.70% | 2.60% | ||

| 13:30 | USD | PPI Core M/M Oct | 0.20% | 0.20% | ||

| 13:30 | USD | PPI Core Y/Y Oct | 2.50% | 2.50% | ||

| 15:00 | USD | Wholesale Inventories M/M (SEP F) | 0.30% | 0.30% | ||

| 15:00 | USD | U. of Mich. Sentiment Nov P | 98 | 98.6 |