{kind=link}

Sterling remains rather resilient despite more Brexit negative news today. There seems to be no progress on negotiation at all and there is little hope for a November EU summit. Nonetheless, the Pound defies gravity and is trading as the second strongest one today. Australian Dollar is the strongest as supported by upbeat RBA statement released earlier today. On the hand other, Canadian Dollar and Dollar are the weakest ones. The greenback is notably softer as markets await the result of US mid-term elections.

Stock markets are also mixed. At the time of writing, FTSE is down -1.06%, possibly mainly due to Sterling’s rally. DAX is down -0.42% and CAC is down -0.52%. German 10 year yield is up 0.001 at 0.430. Italian 10 year yield is up 0.080 at 3.403. German-Italian spread is marginally below 300. Earlier in Asia, Nikkei closed up 1.14% at 22147.75. Hong Kong HSI closed up 0.72% at 26120.96. But China Shanghai SSE dropped -0.23% at 2659.36.

Technically, USD/JPY breached 113.38 resistance earlier today but traders refused to commit so far. Similarly, EUR?GBP also breached 0.8722 support but recovered quickly. These are some signs of hesitation. Though, the Dollar appears to weaken against Euro and Swiss Franc in early US session. And the development suggests that Dollar is now in another leg down as correction extends.

UK PM May made no progress on Brexit at the Cabinet meeting

It appears that no progress on Brexit is made after UK Prime Minister Theresa May’s Cabinet meeting. May’s spokesman James Slack told reporters that there’s still a “significant amount of work” to do, “across government” on how the exit mechanism might work. The discussion inside the Cabinet was “constructive” and there was a shared view that the UK cannot remain in the “backstop indefinitely”.

Separately, EU chief Brexit negotiator talked to Belgian broadcaster RTBF. He said “For now, we are still negotiating and I am not, as I am speaking to you this morning, able to tell you that we are close to reaching an agreement, since there is still a real point of divergence on the way of guaranteeing peace in Ireland, that there are no borders in Ireland, while protecting the integrity of the single market.”

DUP Donaldson said they’re heading for no-deal Brexit

Sterling dipped briefly today after Jeffrey Donaldson, a Democratic Unionist Party lawmaker, tweeted that “Looks like we’re heading for no deal” Brexit. He warned that “such an outcome will have serious consequences for economy of Irish Republic”. And, “in addition, UK won’t have to pay a penny more to EU, which means big increase for Dublin.”

Donaldson referred to Irish Foreign Minister Simon Coveney’s tweet on Sunday that “the Irish position remains consistent and v clear that a “time-limited backstop” or a backstop that could be ended by UK unilaterally would never be agreed to by IRE or EU.”

Eurozone PMI composite finalized at 53.1, notable slowdown in Italy

Eurozone PMI services was finalized at 53.7 in October, down from prior month’s 54.7. PMI composite was finalized at 53.1, down from September’s 54.1. Among the countries, Italy PMI composite dropped to 49.3, a 59-month low. German PMI composite also dropped to 5-month low at 53.4.

Chris Williamson, Chief Business Economist at IHS Markit said the PMI figures hint at upward revision to 0.2% Q3 GDP growth. But “the economy has slowed and that the weakness has intensified into the fourth quarter”. Also, “Italy has recorded an especially noticeable slowdown, slipping into decline during October, whilst Germany has also seen a worrying easing of growth, with both countries affected by rising political uncertainty. France and Spain, in contrast, have seen more resilient business conditions, though both are registering much slower growth than earlier in the year.”

European businesses increasingly desensitized to China Xi Jinping’s constant repetition of empty promises

The European Chamber of Commerce in China blasted Chinese President Xi Jinping’s speech regarding opening up the markets yesterday. In the keynote speech at the China International Import Expo (CIIE), Xi introduced five initiatives, including stimulating potential for imports, broadening market access for foreign investment, creating a world-class business environment, exploring new horizons of opening up, and promote international cooperation multilaterally and bilaterally.

In a statement, the Chamber criticized that much of the content delivered by Xi just “echoed” what was previously announced at Boao in April. And, this was just “constant repetition”, without “sufficient concrete measures or times lines”. And Xi has left the European business community “increasingly desensitized” to these kinds of promises.

RBA kept cash rate at 1.5%, raised growth forecast a little

RBA left cash rate unchanged at 1.50% as widely expected. Overtone is affirmative but as the improve in wages growth and inflation would be gradual, RBA is in no rush to raise interest rate. The central bank provided a glimpse of the new economic forecasts in the statement. We’ll have to wait for the full Monetary Policy Statement on Friday for the details.

RBA noted that GDP growth forecasts for 2018 and 2019 were “revised up a little” to around 3.5%. GDP growth would slow in 2020 due to “slower export growth or resources”. Growth in household consumption is “one continuing source of uncertainty” due to low income growth, high debt levels and some decline in asset prices. Stronger than expected terms of trade are expected to “decline over time” but stay at relatively high level.

Labor market outlook “remains positive” and unemployment rate is expected to drop further to around 4.75% in 2020. Rise is wages growth is “still expected to be a gradual process”. Inflation outcomes were inline with expectations. CPI is expected to pickup over the next couple of years, gradually. CPI is forecast to be at 2.25% in 2019 and a bit higher in 2020.

More on RBA: RBA Turns More Upbeat Over GDP Growth, Keeps Rates Unchanged amidst Low Inflation

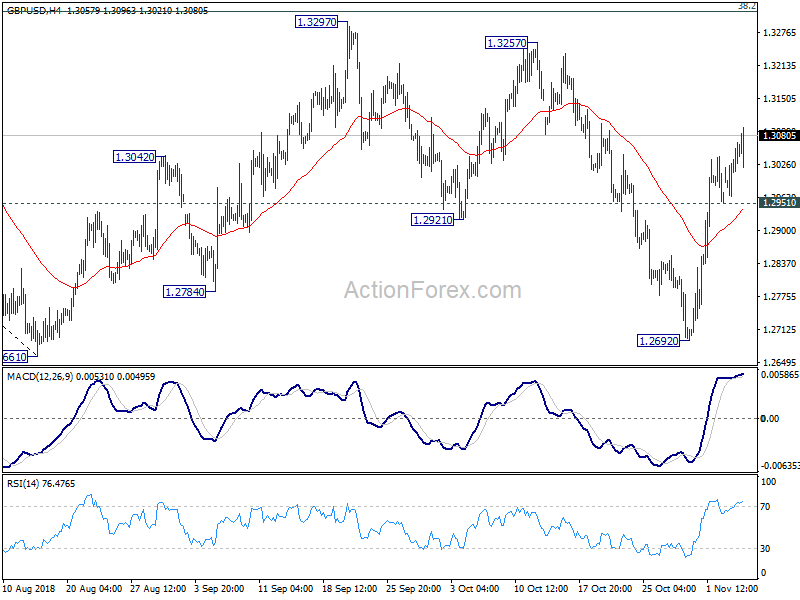

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2985; (P) 1.3021; (R1) 1.3077; More…

No change in GBP/USD’s outlook as the rebound from 1.2692 is in progress. Intraday bias stays on the upside for 1.3257/3297 resistance zone. Such rally is seen as the third leg of consolidation pattern from 1.2661. Hence, we’d expect strong resistance from 1.3316 fibonacci level to limit upside to bring down trend resumption eventually. On the downside, below 1.2951 minor support will turn bias back to the downside for 1.2692 instead.

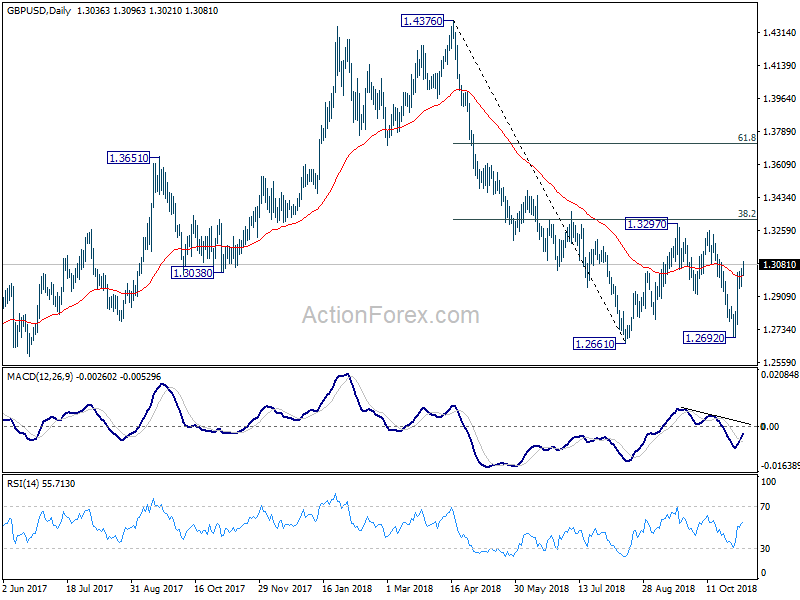

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Sep | -1.60% | 1.60% | 2.80% | |

| 00:01 | GBP | BRC Retail Sales Monitor Y/Y Oct | 0.10% | 0.60% | -0.20% | |

| 03:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 07:00 | EUR | German Factory Orders M/M Sep | 0.30% | -0.40% | 2.00% | 2.50% |

| 08:45 | EUR | Italy Services PMI Oct | 49.2 | 52.1 | 53.3 | |

| 08:50 | EUR | France Services PMI Oct F | 55.3 | 55.6 | 55.6 | |

| 08:55 | EUR | Germany Services PMI Oct F | 54.7 | 53.6 | 53.6 | |

| 09:00 | EUR | Eurozone Services PMI Oct F | 53.7 | 53.3 | 53.3 | |

| 10:00 | EUR | Eurozone PPI M/M Sep | 0.50% | 0.30% | 0.30% | 0.40% |

| 10:00 | EUR | Eurozone PPI Y/Y Sep | 4.50% | 4.20% | 4.20% | 4.30% |

| 13:30 | CAD | Building Permits M/M Sep | 0.40% | 0.30% | 0.40% |