{kind=link}

Asian stocks, as well as Australian and New Zealand Dollar, are shot up by optimism that US-China trade negotiation is having some nice progress. At the time of writing, Hong Kong HSI is leading the way up with 2.4% gain. China Shanghai SSE is up 1.21%. Nikkei and Singapore Strait Times are also rising 0.81% and 0.73% respectively. Additionally, the Chinese Yuan rebounded after tentatively defending the psychologically important 7.000 handle. Further buying is seen in Aussie and Kiwi as traders are preparing to enter into European session.

Sterling pares back some gains today but remains the third strongest on Brexit optimism and hawkish BoE. Additional support is given to the Pound on news of a compromised Irish backstop proposal by the EU. Yen is the weakest on for today, and the week too, on strong risk appetite. Dollar is the second weakest for today as trade war fear recedes. The greenback suffered a roller-coaster ride this week and will need strong job data as savior.

Technical, both AUD/USD and NZD/USD dollar show strong signs of medium term trend reversal. It’s still a bit far, but AUD/USD will look into 0.7314 key resistance. Similarly, EUR/AUD will look into 1.5601 key support to confirm medium term bearish reversal too. Meanwhile, Dollar’s outlook is actually not that bad for now. EUR/USD, while rebounded ahead of 1.1300 key support, is still held by 1.1421 minor resistance. USD/JPY recovered ahead of 112.56 minor support. USD/CHF is also trying to defend 1.0007 minor support. Even USD/CAD is just pressing 1.3068 minor support. There is prospect of a turn around in the greenback.

Chinese Yuan rebounds strongly on US-China trade talk progress

US and Asian stocks are boosted up on hope of resolution in US-China trade tensions. Trump tweeted yesterday that the had “long and very good” conversation with Chinese President Xi Jinping, with “heavy emphasis on trade”. He added the “discussions are moving along nicely” and meeting is being scheduled at the G20 summit in Argentina.

Separately, Xi said on CCTW state television that “the two countries’ trade teams should strengthen contact and conduct consultations on issues of concern to both sides, and promote a plan that both can accept to reach a consensus on the China-U.S. trade issue.” Chinese Premier Li Keqiang also said yesterday that “we do hope that China and the United States will meet each other halfway and work together in the spirit of mutual respect and equality.”

The response in Chinese Yuan was overwhelming. USD/CNH (offshore Yuan), hit as high as 6.9804 this week but it’s now back at 6.9269. And for now, hope is raised for China to defend 7.000 handle for the Yuan.

Focus turns to Non-Farm Payrolls

Dollar had a roller coaster ride this week and is not trading in deep red against Aussie and Kiwi, mixed in general. The greenback will at least need some very solid set of job data to bring back some lives to it. Markets are expecting NFP to show 200k growth in October. Unemployment rate is expected to be unchanged at 3.7%. Average hourly earnings are expected to grow 0.2% mom.

Other job related data released so far were generally solid. ADP employe blew the market with 227k growth in private sector jobs. Initial jobless claims averaged October at 211k, which remained ultra-low in historical standard. The employment component of ISM manufacturing did dropped 2 pts to 56.8. But that’s still well above 50. US consumer confidence surged to 137.9 in October, highest in 18 years. There is little worry in the headline number and the unemployment rate. The questions remains on whether wage growth is strong enough to warrant Fed’s rate path.

Other readings on NFP:

- NFP Preview: Dollar Drops Ahead Of US Jobs Report

- US Jobs Data Expected To Show Wage Growth At Near Decade High: FX And Equity Market Action Eyed

EU floats compromised Irish backstop solution for Brexit

The Financial Times reported that EU is floating around a compromised Irish border backstop proposal to solve the ongoing Brexit negotiation impasse. The proposal was briefed to EU ambassadors earlier on Wednesday.

Under the proposal, EU would lay out the full terms of a “bare-bones” whole-UK customs union in the withdrawal agreement. It would apply a common external tariff on imports from outside the EU and rules of original. Meanwhile, under the backstop, Northern Ireland would remain in a deep customs union with the EU, applying all “customs code” and following EU’s regulations for goods and agri-food products. The stop-gap measures would remain in place until concluding the permanent UK-EU trade deal.

UK Prime Minister Theresa May is expected to tell the EU whether UK is open to the compromise next week. And that would be a key factor to determine if a November Brexit summit is to be held.

BoE stood pat and delivered hawkish signals

Yesterday, BOE voted unanimously to keep all monetary policies unchanged in November. The Bank rate stays unchanged at 0.75%. Meanwhile, purchases of gilts and corporate bonds remain at 435B pound and 10B pound, respectively. The central bank sent a more hawkish-than-expected message to the market. While reiterating “gradual and limited” monetary stance, BOE noted more rate hikes might be needed as there could be overheating in the economy in 2H19. Meanwhile, its desire to hike interest rates could materialise amidst smooth Brexit.

More on BoE

- Hawkish Carney Signals Overheating Economy Could Accelerate BOE Rate Hikes

- BoE Bank Rate projections show more confidence on 2019 rate hike

- Bank Of England Review: Hiking Cycle Continues But Depends On Brexit Deal

- GBP/USD: Renewed Brexit Hopes Lift Cable to Key Level as BoE Remains on Hold

Japan PM Abe: Won’t proceed with sales tax hike if there’s global crisis

Japanese Prime Minister Shinzo Abe appeared to be backing down on his stance regarding the planned sales tax hike next year. For now, he’s still on track to raise sales tax from 8% to 10% in October 2019. He also pledged to mitigate any impact on the economy by providing counter measures.

However, he told parliament that “Our basic stance is that we will proceed with the sales tax hike. But it’s wrong to be too rigid about this and raise the tax rate no matter what.” And, “we will proceed with the tax hike unless the economy is hit by a shock of the scale of the collapse of Lehman Brothers”, which “would be something like a global economic crisis or a huge earthquake.”

On the data front

Japan monetary base rose 5.9% yoy in October versus expectation of 6.2%. Australia PPI rose 0.8% qoq, 2.1% yoy in Q3, retail sales rose 0.2% mom in September.

Swiss will release retail sales in European session. But main focus will be on UK construction PMI as well as Eurozone PMI manufacturing final.

Later in the day, US and Canada will release job report as well as trade balance.

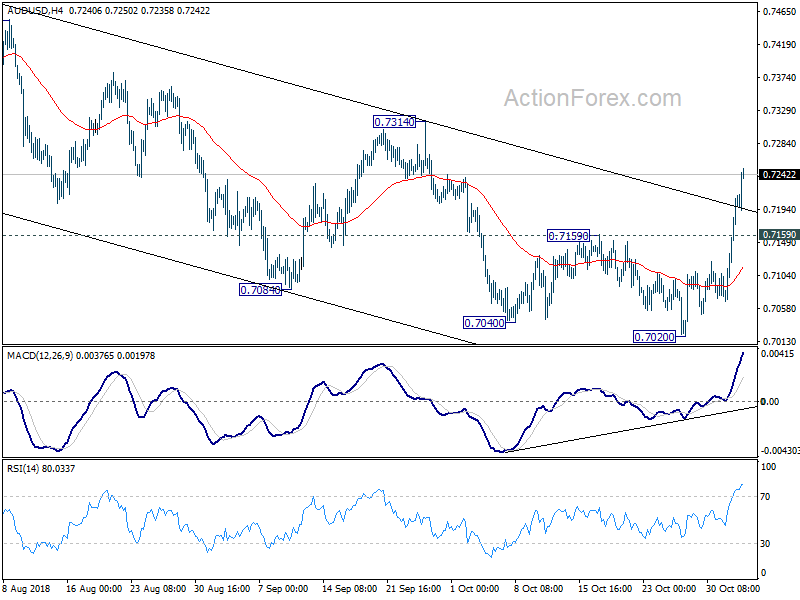

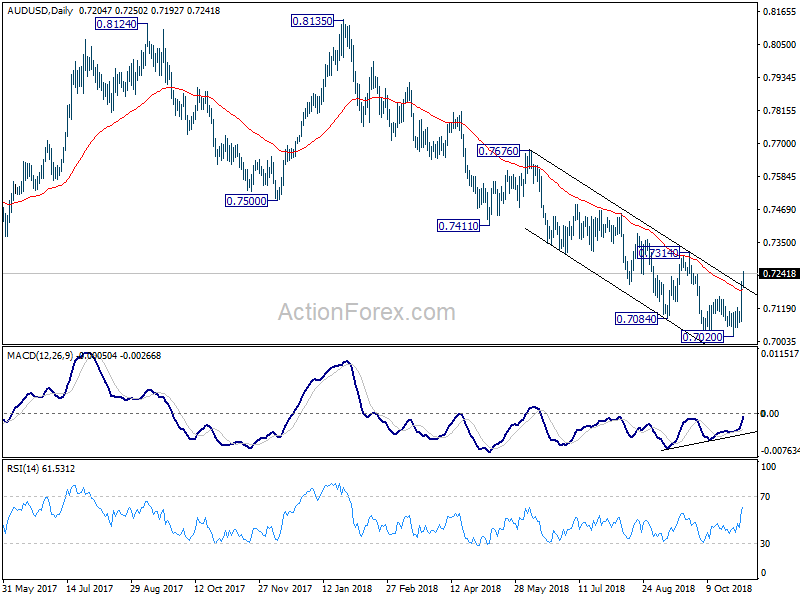

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7115; (P) 0.7164; (R1) 0.7256; More…

AUD/USD’s rally accelerates further to as high as 0.7250 so far today. The case for medium term reversal continues to build up, with bullish convergence condition in daily MACD and break of falling channel resistance. Intraday bias stays on the upside for 0.7314 resistance next. Decisive break there will confirm the bullish case. However, rejection from 0.7314, followed by break of 0.7159 resistance turned support, will retain bearishness and turn focus back to 0.7020 low.

In the bigger picture, fall from 0.8135 is tentatively treated as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 will target 0.6008 key support next (2008 low). On the upside, break of 0.7314 resistance is needed to indicate medium term bottoming. Otherwise, outlook stays bearish even in case of strong rebound. However, firm break of 0.7314 will suggest that whole decline from 0.8135 has completed and bring stronger rise back to 55 week EMA (now at 0.7467).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Oct | 5.90% | 6.20% | 5.90% | |

| 0:30 | AUD | PPI Q/Q Q3 | 0.80% | 0.20% | 0.30% | |

| 0:30 | AUD | PPI Y/Y Q3 | 2.10% | 1.50% | ||

| 0:30 | AUD | Retail Sales M/M Sep | 0.20% | 0.30% | 0.30% | |

| 8:15 | CHF | Retail Sales Real Y/Y Sep | -0.30% | 0.40% | ||

| 8:45 | EUR | Italy Manufacturing PMI Oct | 49.7 | 50 | ||

| 8:50 | EUR | France Manufacturing PMI Oct F | 51.2 | 51.2 | ||

| 8:55 | EUR | Germany Manufacturing PMI Oct F | 52.3 | 52.3 | ||

| 9:00 | EUR | Eurozone Manufacturing PMI Oct F | 52.1 | 52.1 | ||

| 9:30 | GBP | UK Construction PMI Oct | 52 | 52.1 | ||

| 12:30 | CAD | Net Change in Employment Oct | 25.0K | 63.3K | ||

| 12:30 | CAD | Unemployment Rate Oct | 5.90% | 5.90% | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Sep | 0.5B | |||

| 12:30 | USD | Change in Non-farm Payrolls Oct | 200K | 134K | ||

| 12:30 | USD | Unemployment Rate Oct | 3.70% | 3.70% | ||

| 12:30 | USD | Average Hourly Earnings M/M Oct | 0.20% | 0.30% | ||

| 12:30 | USD | Trade Balance Sep | -53.4B | -53.2B | ||

| 14:00 | USD | Factory Orders Sep | 0.30% | 2.30% |