{kind=link}

Sterling surged overnight on Brexit optimism and is boosted further in Asia with more Brexit-positive news. Though, for today, it’s overwhelmed by Australian and New Zealand Dollar on strong risk appetite. The Pound will need to look into BoE economic projections for more inspirations. Dollar, on the other hand, is losing ground broadly again, reversing some of yesterday’s socks and yield supported gains. The greenback is followed by Canadian Dollar and Yen as the second and third weakest.

Technically, Euro is an interesting one to watch today. EUR/USD appears to be supported by 1.1300 key level for now and recovers. However, the selloff in EUR/GBP and EUR/AUD is limiting Euro’s rebound. EUR/GBP’s break of 0.8868 minor support yesterday already suggests near term reversal and could bring deeper fall back to 0.8722 support. The break of 1.5984 support in EUR/AUD is even more important as it’s an early indication of medium term reversal. It remains to be see, after all the movements offset each other, whether EUR/USD could defend this key 1.1300 level successfully.

In other markets, DOW closed up 241.12 pts or 0.97% at 25115.76. S&P 500 gained 1.09% to 2711.74. NASDAQ added 2.01% to 7305.90. There are tentative signs of near term reversal in US stocks. Treasury yields also rose broadly after gapping up. 10-year yield rose 0.049 to 3.159. 30 year yield rose 0.046 to 3.402. In particular, 30-year yield has prospect of breaking 3.424 near term resistance to resume recent up trend, before weekly close. Asian markets are mixed though. Nikkei is currently down -0.7%. But Hong Kong HSI is up 1.84%, China Shanghai SSE is up 1.13% and Singapore Strait Times is up 1.16%. Japan 10 year JGB yield is up another 0.0051 at 0.134.

Sterling extends rally on Brexit optimism, BoE Inflation Report eyed

Pound rallies further today on more positive Brexit news. The Times reported that a tentative deal is agreed between UK and the EU on all aspects of a future partnership on services. Most importantly, that would grant access of EU markets to for British financial services companies. Prime Minister Theresa May’s senior advisor Oliver Robbins is handling the negotiations in Brussels and is expected to complete it within three weeks.

The news came on top of reports that Brexit Minister Dominic Raab told MPs in a letter dated October 24 that November 21 is the date to conclude the Brexit negotiation. There he said “I would be happy to give evidence to the committee when a deal is finalized, and currently expect 21 November to be suitable.” The letter was published on the Commons Brexit committee yesterday. But three hours after that, Raab’s office, Department for Exiting the European Union, backtracked and said there was “There is no set date for the negotiations to conclude. The 21st November was the date offered by the Chair of the Select Committee for the Secretary of State to give evidence.”

BoE is widely expected to keep monetary policies unchanged today. Updated forecasts in the quarterly inflation report are the main focuses. Recent economic data from the UK haven’t been too encouraging. August GDP growth slowed to 0.0%. PMIs showed a mixed picture, with rebound in manufacturing but slowdown in services and construction. CPI also slowed to 2.4%. But after all, BoE’s projections should be based on the main scenario of smooth Brexit, which is still uncertain. For now, there is little chance of seeing when BoE will move interest rate next, until the Brexit dusts settle.

As a recap, this is BoE’s August forecast summary.

White House Kudlow: Additional tariffs on China not set in stone

White House economic adviser Larry Kudlow said the additional tariffs on China are not “set in stone right now”. He added, “if some kind of amicable deal with China were to happen, then a lot of tariffs might be pulled back.” Also, “The policy talks determine this, not an arbitrary timetable. If the policy talks go well, then we’ll have a much better situation. If the policy talks don’t, it may deteriorate.”

Kudlow also said Trump mentioned in a recent interview that if there are “promising policy discussions, I don’t know about a full fledged deal, but if things go well, maybe some tariffs get withdrawn and maybe not.” However, Kudlow didn’t specify which interview he referred to. Instead, the only know one is with Fox News Channel’s “The Ingraham Angle” which Trump said he expects a “great deal” with China, without mentioning withdrawing tariffs.

SNB Jordan: Swiss among hardest hit in full-scale trade war

SNB Chair Thomas Jordan warned yesterday that Switzerland could be heavily hit if full-scale trade war broke out. He said “All countries would feel the detrimental effect of a global trade war, but small, open economies such as Switzerland would be among those hardest hit.”

Additionally, the current trade tensions have already made it more difficult to conduct monetary policy. He noted, “a wave of protectionism would create a lot of uncertainty, be it with regard to the short-term development of the real economy and prices, or with regard to the longer-term macroeconomic context.” And, “the risk of monetary policy mistakes would increase, at least while the economy is in the process of adapting to the changed market conditions.”

Jordan also asked the question that the Swiss Franc could be “sought as a safe haven in the event of a trade war”, and Swiss could “face particularly strong exposure to a severe contraction in world trade”.

Australian manufacturing PMI dropped to 58.3, expansion to continue into 2019

Australia AiG Performance of Manufacturing index dropped to 58.3, seasonally adjusted, in October, down from 59.0. The Australian Industry Group noted in the release that the PMI now indicated twenty-five months of uninterrupted recovery and expansion, “longest run of recovery or expansion in this data series since 2005”. The broad based expansion was led by the wood and paper and the food & beverages sectors. And, the details suggested that manufacturing will “continue to expand for the rest of 2018 and into 2019.”

Also from Australia, trade surplus widened to AUD 3.02B in September.

China Caixin PMI manufacturing: Economy has not seen obvious improvement

China Caixin PMI manufacturing rose 0.1 to 50.1 in October, matched expectations. Markit noted there was only “marginal increase in total new work amid further drop in export sales”. Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said, “Overall, expansion across the manufacturing sector was still weak. Production and business confidence continued to cool despite stable demand. The pressure on production costs didn’t ease. China’s economy has not seen obvious improvement.”

Looking ahead

BoE rate decision will be the main focus for today. UK will also release PMI manufacturing. Swiss will release SECO consumer confidence, CPI and PMI manufacturing in European session too. Later in the day, US data will take center stage with ISM manufacturing, construction spending, non-farm productivity and jobless claims featured.

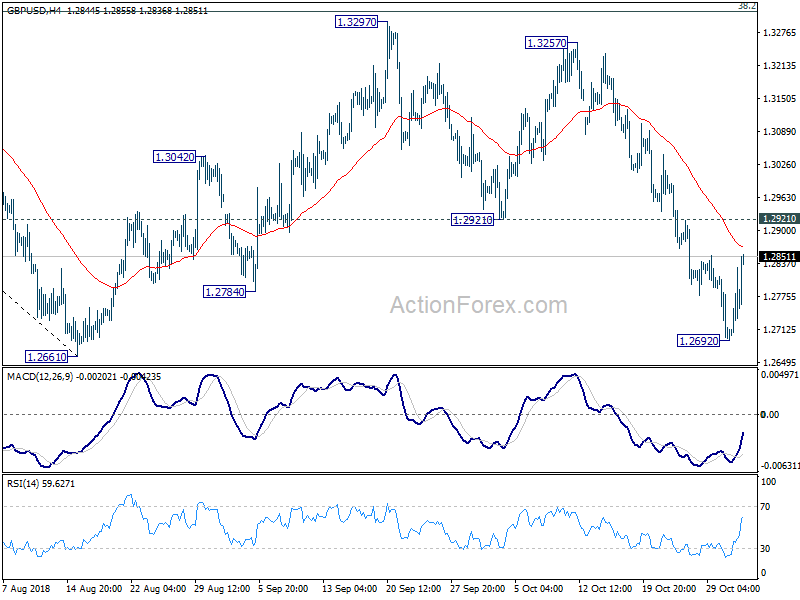

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2698; (P) 1.2765; (R1) 1.2833; More…

GBP/USD’s rebound from 1.2692 extends higher today but it’s limited below 1.2921 support turned resistance. Intraday bias stays neutral first. As long as 1.2921 holds, near term outlook stays cautiously bearish and another decline is in favor. On the downside, break of 1.2692 will target 1.2661 low first. Decisive break there will resume larger down trend from 1.4376. Next target is 61.8% projection of 1.4376 to 1.2661 from 1.3297 at 1.2237. However, break of 1.2921 should extend the consolidation pattern from 1.2661 with another rise towards 1.3297 resistance before completion.

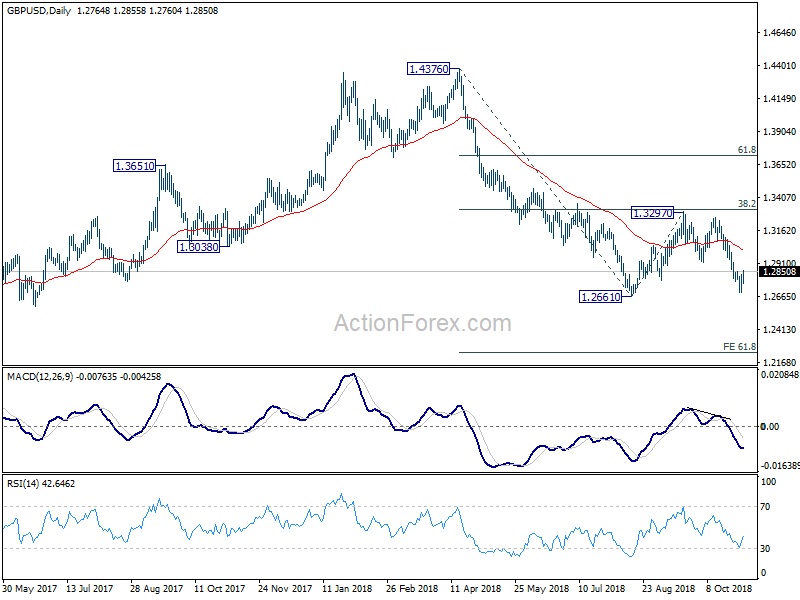

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Manufacturing Index Oct | 58.3 | 59 | ||

| 00:30 | JPY | PMI Manufacturing Oct F | 52.9 | 53.1 | ||

| 00:30 | AUD | Trade Balance (AUD) Sep | 3.02B | 1.71B | 1.60B | 2.34B |

| 01:45 | CNY | Caixin PMI Mfg Oct | 50.1 | 50.1 | 50 | |

| 06:45 | CHF | SECO Consumer Confidence Oct | -8 | -7 | ||

| 08:15 | CHF | CPI M/M Oct | 0.20% | 0.10% | ||

| 08:15 | CHF | CPI Y/Y Oct | 1.10% | 1.00% | ||

| 08:30 | CHF | PMI Manufacturing Oct | 58.5 | 59.7 | ||

| 09:30 | GBP | PMI Manufacturing Oct | 53 | 53.8 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | 70.90% | |||

| 12:00 | GBP | BoE Bank Rate | 0.75% | 0.75% | ||

| 12:00 | GBP | BoE Asset Purchase Target | 435B | 435B | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 0–0–9 | 0–0–9 | ||

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | ||

| 12:00 | GBP | BoE Inflation Report | ||||

| 12:30 | USD | Nonfarm Productivity Q3 P | 2.00% | 2.90% | ||

| 12:30 | USD | Unit Labor Costs Q3 P | 1.10% | -1.00% | ||

| 12:30 | USD | Initial Jobless Claims (OCT 27) | 213K | 215K | ||

| 13:30 | CAD | Manufacturing PMI Oct | 54.8 | |||

| 13:45 | USD | Manufacturing PMI Oct F | 55.9 | 55.9 | ||

| 14:00 | USD | Construction Spending M/M Sep | 0.20% | 0.10% | ||

| 14:00 | USD | ISM Manufacturing Oct | 59 | 59.8 | ||

| 14:00 | USD | ISM Prices Paid Oct | 67.5 | 66.9 | ||

| 14:00 | USD | ISM Employment Oct | 58.8 | |||

| 14:30 | USD | Natural Gas Storage | 53B | 58B |