{kind=link}

Improved risk sentiment is the main theme of today. Italian stocks lead other Europeans higher as investors responded well to S&P’s decision to keep Italy’s ratings unchanged, two notches above junk. Additionally, auto shares are lifted by report that China is considering to cut car purchase tax by half. Yen and Swiss Franc are trading as the weakest ones, naturally, on improved risk appetite. Euro follows as the third weakest. On the other hand, commodity currencies are trading generally higher. US Dollar continues to trade mixed after data showed core PCE inflation unchanged at 2.0%, staying at Fed’s target.

In Europe, the Italy’s FTSE MIB is currently up 2.37%, FTSE 100 is up 1.95%, DAX up 1.99% and CAC up 1.08%. German 10 year yield is up 0.0366 at 0.394, still below 0.4%. Italian 10 year yield dropped -0.123 at 3.307. German-Italian spread is improving at 291. Earlier in Asia, major indices closed mixed. China Shanghai SSE closed down -2.18% at 2542.17. But the closely correlated Hong Kong HSI closed up 0.28%. Nikkei lost -0.16% and Singapore Strait Times gained 0.32%. Japan 10 year yield dropped -0.0095 to 0.105, now very very close to BoJ’s allowed range of -0.1 to 0.1%.

Technically, USD/JPY, EUR/JPY and GBP/JPY have made temporary lows. But it’s too early to confirm near term reversal. For now Dollar is holding in tight range in EUR/USD and GBP/USD. There is prospect of extending decline in these two pairs but we’d pay attention to loss of momentum on next fall.

US headline PCE slowed to 2.0%, core PCE unchanged at 2.2%

In September, US personal income rose 0.2%, below expectation of 0.3%. Spending rose 0.4%, matched expectations. Headline CPI slowed to 2.0%, down from 2.2%. Core PCE was unchanged at 2.0% yoy.

Released elsewhere, UK mortgage approval rose to 65k in September, M3 money supply dropped -0.3% mom. Japan retail sales rose 2.1% yoy in September.

Relief from S&P rating action on Italy may be temporary

S&P refrained from downgrading Italy’s sovereign credit rating, keeping it at BBB, two notches above junk grade. Yet, the relief might just be temporary as the rating agency has placed the country in “negative” watch, suggesting a downgrade can come with the 24-month period. Moody’s went further a week ago by announcing a downgrade to Baa3, making the country’s rating just one notch above junk. With a “stable” watch, such rating should likely stay for the coming 12-18 months. Fitch and DBRS have not released review schedule yet.

However, it should be reminded that European Commission rejected Italy’s draft budget plan as it has violated EU’s budget rules under the Stability and Growth Pact. So far, the populist government has stood firm in their position. The country’s current debt-to-GDP ratios stays at an elevated 130% level, more than doubling EU’s rule. Worse still, both S&P and Moody’s expect the situation won’t improve in coming years. We believe further downgrades are likely down the road.

More in Italy Credit Rating – Further Downgrades are Yet to Come

German Merkel to stop leading CDU, markets shrug

German Chancellor confirmed the rumor that she is not going to run for leadership of the Christian Democratic Union again in December. Also, she’s stay and carry out my duties as chancellor for the rest of the legislative period till 2021. She also confirmed that her hand-picked CDU general secretary, Annegret Kramp-Karrenbauer, and conservative rival, Jens Spahn, will both run as party leader. For now, she is not taking a side but rather, she’s looking at the party leadership race “as an opening, a phase of possibilities,” “a nice process”.

Market reaction is rather muted to the news though. It’s believed that even if Merkel would be replaced as Chancellor, there won’t be much change to the coalition’s policies, which will still be dominated by CDU/CSU and the Spuds, her staying as Chancellor is unlikely to rock the boat. Additionally, it’s also good time for her to pave the way for her successor.

UK Hammond: A different budget strategy needed in case of no-deal Brexit

UK Chancellor of the Exchequer Philip Hammond will deliver his budget speech today. He told Sky News that in case of a no-deal Brexit, “we would need to look at a different strategy and frankly we’d need to have a new budget that set out a different strategy for the future.” And the government would have to ” see how markets and businesses and consumers responded to that.” And then, “we would take appropriate fiscal measures to protect the economy, to prepare us for the future and to strike out in a new direction”.

Separately, he pledge to BBC that he will maintain fiscal buffers, a reserve of borrowing power against my fiscal rules, so if the economy, as a result of a no-deal Brexit or indeed because of something else that we haven’t anticipated, needs support over the coming months and years I have the capacity to provide that support.” And he emphasized “the important point is that I have got fiscal reserves that would enable me to intervene.”

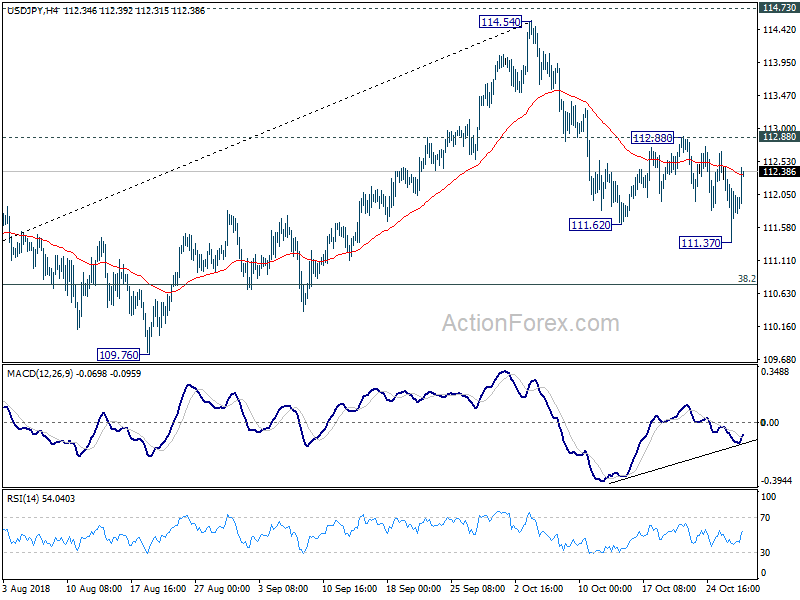

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.36; (P) 111.91; (R1) 112.43; More..

USD/JPY’s strong rebound today suggests temporary bottoming at 111.37 and intraday bias is turned neutral first. Another fall remains mildly in favor as long as 112.88 minor resistance holds. Break of 111.37 will extend the fall from 114.54 to 38.2% retracement of 104.62 to 114.54 at 110.75. As such fall is seen as part of medium term correction, we’ll look for bottoming signal above 109.76 key support. On the upside, break of 112.88 resistance will suggest that the fall has completed and turn bias back to the upside for retesting 114.54.

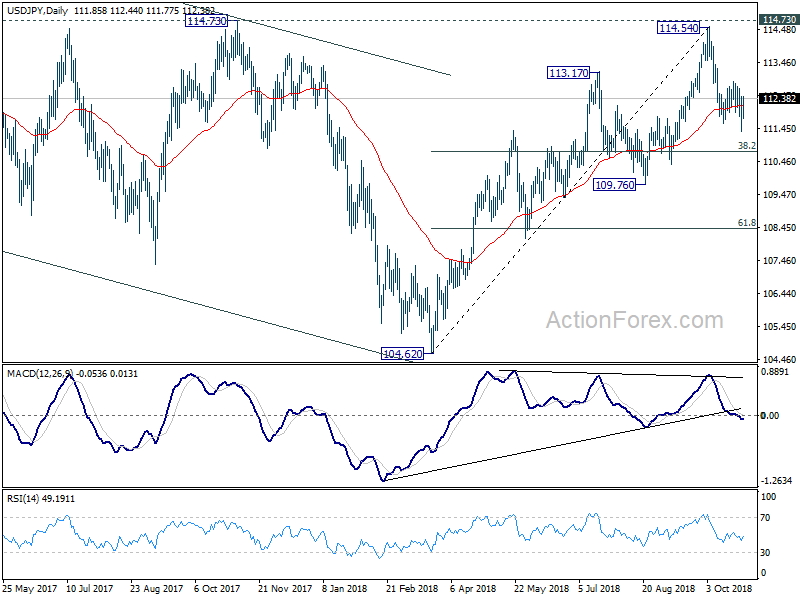

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.76 support holds. However, decisive break of 109.76 will dampen this bullish view and turns outlook mixed again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y Sep | 2.10% | 2.10% | 2.70% | |

| 09:30 | GBP | Mortgage Approvals Sep | 65K | 65K | 66K | |

| 09:30 | GBP | Money Supply M4 M/M Sep | -0.30% | 0.30% | 0.20% | |

| 12:30 | USD | Personal Income Sep | 0.20% | 0.30% | 0.30% | 0.40% |

| 12:30 | USD | Personal Spending Sep | 0.40% | 0.40% | 0.30% | 0.50% |

| 12:30 | USD | PCE Deflator M/M Sep | 0.10% | 0.10% | 0.10% | |

| 12:30 | USD | PCE Deflator Y/Y Sep | 2.00% | 2.20% | 2.20% | |

| 12:30 | USD | PCE Core M/M Sep | 0.20% | 0.10% | 0.00% | |

| 12:30 | USD | PCE Core Y/Y Sep | 2.00% | 2.00% | 2.00% |