{kind=link}

Commodity currencies are trading mildly higher today as Asian markets turned mixed. Australian Dollar is the stronger one, followed by New Zealand. On the other hand, Swiss Franc is the weakest, followed by Euro and Yen. Reactions to S&P’s rating review on Italy were rather muted. Sterling is also slightly firmly as Hammond’ budget speech is awaited. And, like most Mondays, the picture could change drastically as volatility kicks in during the European session. Additionally, we’ll also have some important economic data for almost every major currencies in the week ahead.

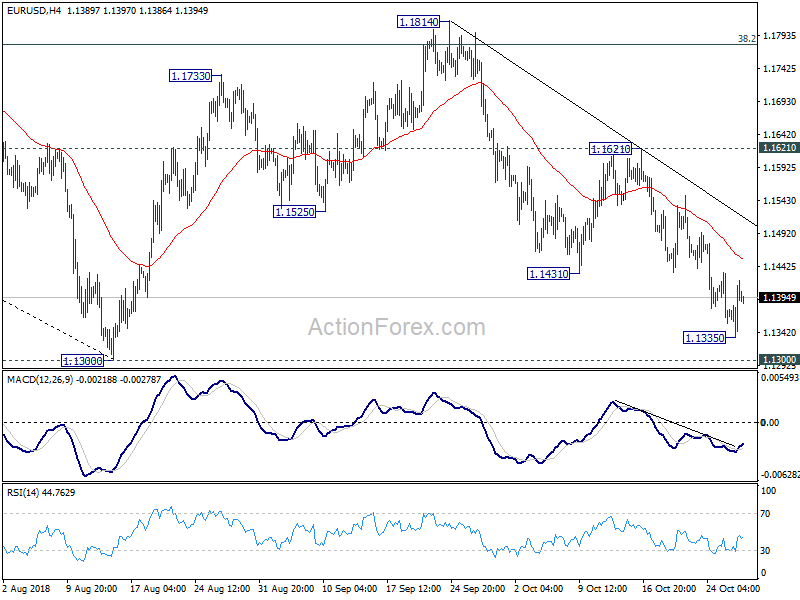

Technically, a key to watch this week is whether Dollar would lose near term upside momentum further, or even reverse. AUD/USD led the way last Friday with the strong rebound and focus will be back on 0.7159 resistance. Meanwhile, EUR/US is now very close to 1.1300 key support level, which is equivalent to 96.98 key support in dollar index. Another focus is how deep Yen crosses will fall to. For now, downside momentum in EUR/JPY, GBP/JPY and even USD/JPY remain rather solid.

In other markets, Nikkei is trading up 0.53% at the time of writing, Singapore Strait Times up 0.56%. But Hong Kong HSI and China Shanghai SSE are down -0.07% and -1.47% respectively. Japan 10 year JGB yield is down -0.0012 at 0.114. Gold is hovering around 1233 and there is no follow through buying through 1240 handle yet.

S&P projects 2.7% debt-to-GDP for Italy in 2019, government’s growth forecasts overly optimistic

Last Friday, S&P kept Italy’s sovereign debt rating unchanged at BBB, two notches above junk. However, outlook was lowered to negative from stable. Nonetheless, the result of the view was already better than Moody’s, which downgraded Italy to a notch above junk with stable outlook.

S&P said in the statement that “the Italian government’s economic and fiscal policy settings are weighing on the country’s economic growth prospects, a critical driver of government debt-to-GDP trajectory.” Also, “the government’s planned economic and fiscal policy settings have eroded investor confidence, as reflected by a rising yield on government debt.”

S&P projected Italy 2019 budget deficit at 2.7% of GDP, higher than the government’s own forecast and pledge of 2.4%. The rating agency noted that the government’s forecasts for economic growth of 1.5% in 2019 and 1.6% in 2020 were “overly optimistic”. And it projected 1.1% growth for both year, even downgraded from 1.4%, as “the demand stimulus from the government’s budgetary measures will likely be short-lived.”

Though, S&P also hailed that Italy “continues to be supported by its wealthy and diversified economy and its strong external position, with the economy close to becoming a net creditor in the context of its net international investment position.”

UK Hammond: A different budget strategy needed in case of no-deal Brexit

UK Chancellor of the Exchequer Philip Hammond will deliver his budget speech today. He told Sky News that in case of a no-deal Brexit, “we would need to look at a different strategy and frankly we’d need to have a new budget that set out a different strategy for the future.” And the government would have to ” see how markets and businesses and consumers responded to that.” And then, “we would take appropriate fiscal measures to protect the economy, to prepare us for the future and to strike out in a new direction”.

Separately, he pledge to BBC that he will maintain fiscal buffers, a reserve of borrowing power against my fiscal rules, so if the economy, as a result of a no-deal Brexit or indeed because of something else that we haven’t anticipated, needs support over the coming months and years I have the capacity to provide that support.” And he emphasized “the important point is that I have got fiscal reserves that would enable me to intervene.”

BoJ and BoE to meet, along with something important for almost every major currencies

Two central banks will meet this week, BoJ and BoE. Both are expected to keep monetary policies unchanged. At the same time, focuses will be on new economic projections from both central banks.

On the data front, there are at least something important for almost every major currencies. US will release PCE, ISM and NFP. Eurozone will release GDP, CPI and unemployment rate. UK will release PMI. Swiss will release KOF and CPI; Canada will release GDP and employment. Australia will release CPI and trade balance. China will release PMIs. So, be prepared for a very busy week.

Here are some highlights:

- Monday: Japan retail sales; UK mortgage approvals, M4 money supply, CBI realized sales; US personal income and spending, PCE inflation

- Tuesday: Japan unemployment rate; Australia building approvals; France GDP; German CPI, unemployment; Italy GDP; Eurozone GDP; Swiss KOF economic barometer; US S&P Case-Shiller house price, consumer confidence

- Wednesday: New Zealand building permits; Japan industrial production, consumer confidence, housing starts, BoJ rate decision; Australia CPI; China PMIs; UK BRC shop price, Gfk consumer confidence; German retail sales; Eurozone CPI, unemployment rate; US ADP employment , employment cost index Chicago PMI; Canada GDP, IPPI and RMPI

- Thursday: Australia trade balance, import price; China Caxin PMI manufacturing; Swiss SECO consumer climate, CPI, manufacturing PMI; BoE rate decision and inflation report, UK PMI manufacturing; US non-farm productivity, jobless claims; ISM manufacturing, construction spending

- Friday: New Zealand ANZ business confidence; Australia retail sales, PPI; German import prices; Eurozone PMI manufacturing final; Swiss retail sales; UK construction PMI; Canada employment, trade balance; US non-farm payrolls, trade balance, factory orders

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1351; (P) 1.1387; (R1) 1.1438; More….

Intraday bias in EUR/USD remains neutral for consolidation above 1.1335 temporary low. On the downside, below 1.1335 will target 1.1300 key support first. Decisive break will resume whole down trend from 1.2555 and target 1.1186 fibonacci level next. On the upside, however, break of 1.1621 resistance will extend the consolidation pattern from 1.1300 with another rise before larger down trend resumption.

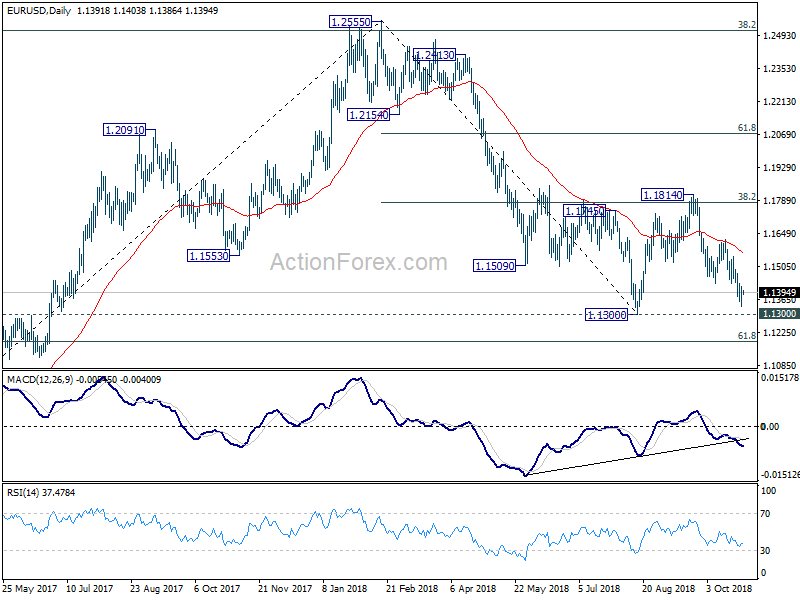

In the bigger picture, corrective pattern from 1.1300 could have completed at 1.1814 after hitting 38.2% retracement of 1.2555 to 1.1300 at 1.1779. Decisive break of 1.1300 will resume the down trend from 1.2555 to 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 next. Sustained break there will pave the way to retest 1.0339. On the upside, break of 1.1814 will delay the bearish case and extend the correction from 1.1300 with another rise before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y Sep | 2.10% | 2.10% | 2.70% | |

| 9:30 | GBP | Mortgage Approvals Sep | 65K | 66K | ||

| 9:30 | GBP | Money Supply M4 M/M Sep | 0.30% | 0.20% | ||

| 11:00 | GBP | CBI Reported Sales Oct | 27 | 23 | ||

| 12:30 | USD | Personal Income Sep | 0.30% | 0.30% | ||

| 12:30 | USD | Personal Spending Sep | 0.40% | 0.30% | ||

| 12:30 | USD | PCE Deflator M/M Sep | 0.10% | 0.10% | ||

| 12:30 | USD | PCE Deflator Y/Y Sep | 2.20% | 2.20% | ||

| 12:30 | USD | PCE Core M/M Sep | 0.10% | 0.00% | ||

| 12:30 | USD | PCE Core Y/Y Sep | 2.00% | 2.00% |