{kind=link}

US equities staged a strong rebound overnight with DOW ended up more than 400 pts. But positive sentiment didn’t carry on in Asia as major indices are all in red. Intensification in selloff in the Chinese Yuan is a possible factor even though we’re not too convinced by this theory. Both Chinese and Hong Kong stocks are just down less than -1% only. Weakness in Asian stocks is more of an extension of recent down trend.

In the currency markets, pressure in back on commodity currencies. New Zealand Dollar lead the way lower, followed by Australian and Canadian. In particular, the resilient AUD/USD has finally taken out 0.7040 low to resume medium term down trend. On the other hand, Yen is the strongest one on risk aversion. The Sterling is the second strongest for now as it’s digesting recent declines. But the recovery in Pound is unlikely to last long. Dollar drew some strength as Trump’s new Fed addition turned out to be hawkish. But it’s cautiously mixed, awaiting Q3 GDP. For the week, Yen is the strongest one while Sterling is the weakest.

Technically, as AUD/USD has resumed recent down trend, it’s time for AUD/JPY to break equivalent support at 78.67 to resume the down trend from 90.29. USD/CAD has reversed all the post BoC losses already. 1.3132 resistance in the pair will be a key focus today, especially with US GDP scheduled. Downside acceleration in both EUR/JPY and GBP/JPY further solidify the case of bearish near term reversal. We’d probably see a take on 124.89 and 139.88 key support level respectively next week. At the same time EUR/USD and GBP/USD should also be heading to recent low at 1.1300 and 1.2661 respectively.

In other markets, DOW closed up 1.63% or 401.13 pts overnight at 24984.55. S&P 500 rose 1.86% and NASDAQ rose 2.95%. 10 year yield rose 0.012 to 3.316 but 30 year yield was flat at 3.346. In Asia, Nikkei closed down -0.40% at 21184.60. Singapore Strait Times is down -1.47%. China Shanghai SSE is down -0.55% and Hong Kong HSI is down -0.86%. Also, Japan 10 year JGB yield is down -0.004 at 0.111.

Chinese Premier Li invites Japanese PM Abe for more mature, steady and progressive relationship

Chinese Premier Li Keqiang invited Japanese Prime Minister Shinzo Abe to build a “more mature, steady and progressive” relationship together. Abe is in a three day visit to China, the first the Prime Minister did in seven years.

Li said, “the China-Japan relationship has gone through wind and rain in the past four decades, yet peace, friendship and cooperation have always been the mainstream.” And he added “we need adhere to the general direction of peace, friendship and cooperation and conform to the trend of the times, so as to jointly build a more mature, steady and progressive China-Japan ties.”

Li also urged “both sides would work hard to promote regional peace, safeguard multilateralism and free trade, and become the axis of stability, growth and momentum for not just Asia but the world,”

Abe said when he arrived in Beijing yesterday that “Today, Japan and China are playing an essential role in economic growth not only in Asia but in the world,” And, “as problems that cannot be resolved by one country alone have risen, the time has come for Japan and China to jointly contribute to world peace and prosperity.”

Today, China and Japan signed a broad range of agreements covering cooperations in areas from finance and trade to innovation and securities listings. In particular, the currency swap arrangement dropped back in 2013 will be revived.

Chinese Yuan selloff intensifies, heading to decade low

Chinese Yuan’s selloff picks up some momentum today. USD/CNH (offshore) break 6.9586 yesterday, as well as a near term channel resistance. The upside acceleration suggests that Yuan selling might intensify for the near term. Now, it looks like a break of 6.9875 high in USD/CNH (2017) low is inevitable. That is, Yuan will hit the lowest level in a decade. The question now is whether there will be intervention of some sort to keep USD/CNH below 7.000 handle.

Trump’s new Fed addition Clarida backs further gradual rate hikes

Fed Vice Chair Richard Clarida, Trump latest addition to the Federal Reserve Board, delivered his first public speech yesterday. And he backs further rate hike by Fed. He said, “if the data come in as I expect, I believe that some further gradual adjustment in the federal funds rate will be appropriate.”

Clarida also noted that “even after our September decision (a 25bps hike), I believe U.S. monetary policy remains accommodative.” He pointed out that ‘the funds rate is just now–for the first time in a decade–above the Fed’s inflation objective”. However, “inflation-adjusted real funds rate remains below the range of estimates for the longer-run neutral real rate, often referred to as r*.”

Additionally, he also noted that “if strong growth and robust employment gains were to continue into 2019 and be accompanied by a material rise in actual and expected inflation, that circumstance would indicate to me that additional policy normalization might well be required beyond what I currently expect.”

Fed Mester: We are beyond maximum employment

In a speech delivered yesterday, Cleveland Fed President Loretta Mester talked down recent market slump again. And as a known hawk, she continues to support further gradually remove of monetary policy accommodation ahead.

She said that “while a deeper and more persistent drop in equity markets could dash confidence and lead to a significant pullback in risk-taking and spending, we are far from this scenario.” And, “similar to the swings in the market we saw earlier this year, the movements of late do not seem to be signaling that investors are becoming overly pessimistic.”

On labor market, she noted that “we are beyond maximum employment”. Much of the explanation of “moderate wage growth”, lies with ” low levels of inflation and productivity growth over this expansion”. And, “I wouldn’t expect to see a strong acceleration in wages unless we see a strong pickup in productivity growth.” Meanwhile, she also emphasized that “maintaining stable inflation expectations will be the key to maintaining inflation at target.

ECB stands pat, confident over outlook

Yesterday, ECB left it policy rates and the asset purchase program unchanged. The main refi rate stays at 0% and the deposit rate at -0.4%. The rationale for the latter is to encourage banks to increase lending, hence stimulate the economy. It reaffirmed that the policy rates would stay on hold until at least the summer of 2019, to ensure that inflation returns sustainably to the target of below, but close to, 2%. Meanwhile, ECB maintains the target of buying 15B euro of assets per month from October to December, reiterating the anticipation that the entire program would finish by until the end of the year.

The members remained confident over the economic outlook but acknowledges some risks, including protectionism and financial market volatility, that could derail the recovery path. As we had anticipated, ECB has kept the details of the reinvestment schedule after QE ends until December. More in ECB Reveals No Details about Reinvestment. December in Focus

Further reading on ECB:

- Draghi Seeks To Reassure By Suggesting Economy Is Solid But ECB Will Be Slow

- ECB Recap: Draghi Sticks to the Script, EUR/USD Bears Eye 16-Month Low Near 1.13

- ECB Review: Steady Draghi Amid Disappointing Data

- ECB press conference live stream, starting in a few minutes

On the data front

Japan Tokyo CPI rose was unchanged at 1.0% yoy in October, matched expectations. US Q3 GDP is the main focus today and is expected to show 3.2% annualized growth

Suggested reading on US GDP: US Q3 GDP Growth Seen Softer But Still Trump-Supportive

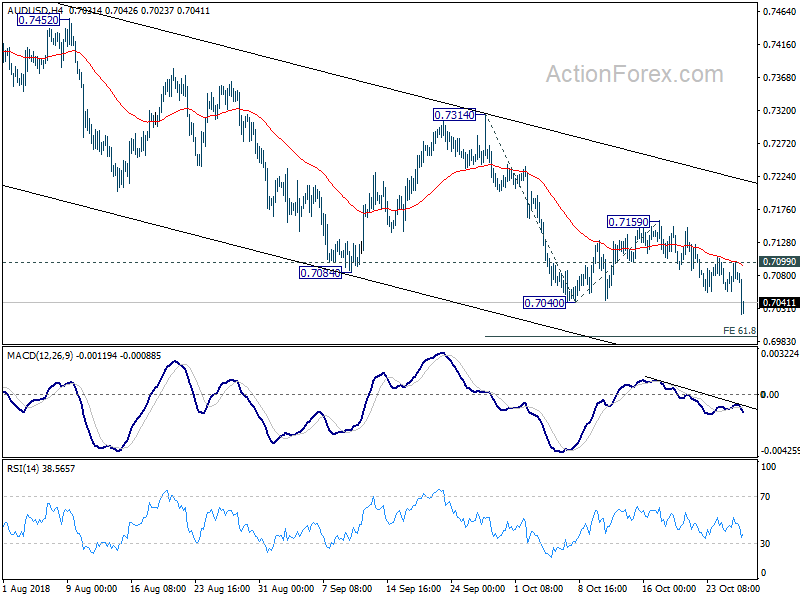

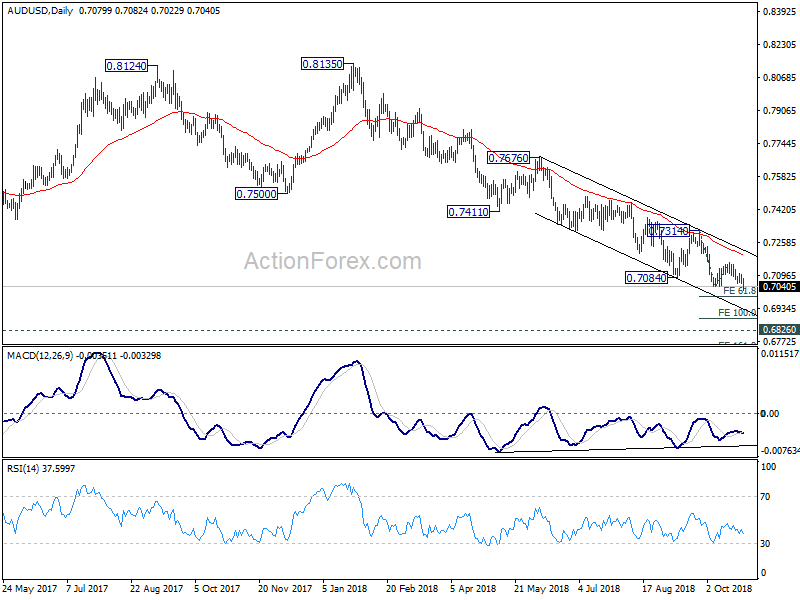

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7057; (P) 0.7078; (R1) 0.7101; More…

AUD/USD drops sharply to as low as 0.7022 so far today. The break of 0.7040 low confirms resumption of the down trend from 0.8135. Intraday bias is back on the downside for 61.8% projection of 0.7314 to 0.7040 from 0.7159 at 0.6990. Break there will target 100% projection at 0.6885. On the upside, break of 0.7099 resistance is needed to signal short term bottoming. Otherwise, outlook will stays bearish in case of recovery.

In the bigger picture, fall from 0.8135 is tentatively treated as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 will target 0.6008 key support next (2008 low). On the upside, break of 0.7314 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook stays bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Oct | 1.00% | 1.00% | 1.00% | |

| 12:30 | USD | GDP Annualized Q3 A | 3.20% | 4.20% | ||

| 12:30 | USD | GDP Price Index Q3 A | 3.00% | |||

| 14:00 | USD | U. of Mich. Sentiment Oct F | 99.2 | 99 |