{kind=link}

Dollar stays steady in early US session after mixed non-farm payrolls report. Even though Canada reported a set of far more impressive data, USD/CAD is back into tight range after initial knee-jerk reactions. For now, Sterling is the strongest one for today, followed by the greenback. Yen is the third strongest one on risk a aversion. On the other hand, New Zealand dollar is the weakest one, followed by Swiss Franc and then Aussie.

In other markets, major European indices are all in red today. FTSE is down -0.87% at the time of writing, DAX down -0.8% and CAC down -0.50%. Earlier today, Nikkei closed down -0.8%, Hong Kong HSI down -0.19%, Singapore Strait Times lost -0.67%. We wonder how much China SSE will fall when it’s back from holiday next week. Strength in global treasury yields is weighing down on investors’ sentiment. German 10 year bund yield is up 0.026 at 0.560. UK 10 year gilt yield is up 0.029 at 1.564. Though, Japan 10 year JGB yield lost -0.0083 to 0.152.

Technically, we might see Dollar gives up more ground before weekly close as it has turned into consolidation against Euro, Sterling, and Yen. Even AUD/USD is losing some downside momentum. The focus is instead on how far Brexit hope could take the Pound to.

US unemployment rate dropped to 49-year low, but headline NFP missed

US unemployment rate dropped to 3.7% in September, down from 3.9% and beat expectation of 3.8%. That’s the lowest level in 49 years. Participation rate was unchanged 62.7%. Headline non-farm payrolls number missed expectation and grew only 134k versus consensus of 188k. But prior month’s upward revisions, from 201k to 270k, was more than enough to cover. Average hourly earnings rose 0.3% mom, matched expectations. Also from US, trade deficit widened to USD -53.2B in August.

From Canada, employment grew another impressive 63.3k in September, nearly double of expectation of 32.5k. Unemployment rate dropped to 5.9%, down fro 6.0% and matched expectations. Trade balance showed CAD 0.5B surplus versus expectation of CAD -1.4B deficit.

Released in European session, Swiss foreign currency reserves rose to CHF 740B in September. CPI slowed to 1.0% yoy in September versus expectation of 1.2% yoy. Germany factory orders rose 2.0% mom in August versus expectation of 0.7% mom. PPI accelerated to 3.1% yoy versus expectation of 2.9% Yoy.

Sterling lifted by news that Brexit deal is very close

Sterling is apparently lifted today by news that EU’s Brexit negotiating team told EU diplomats that a deal is “very close”. And, both sides are working closely for the the summit on October 17-18 first, and then the final one on November 17-18.

Between now and then, October 10 is a key date when EU chief negotiator Michel Barnier will present to European Commission a first draft of the “Outline of new partnership with UK”. That’s for the trade relationship with UK after Brexit.

The issue on Irish border must be cleared before October 17-18 so as for EU to determine that enough progress is made for moving on the the emerging summit in November, when everything would be finalized.

Australia retail sales grew 0.3% in August, South Australia led the way up

Australia retail sales grew 0.3% in August in seasonally adjusted term, matched expectations. There were rises in five of the six industries, except that food retailing was relatively unchanged at 0.0%.

Sales in South Australia led the way by rising 0.8%, followed by Tasmanian by 0.5%, New South Wales by 0.5%, Victoria and Australian Capital Territory both by 0.2%, Queensland by 0.1%. Sales i Western Australia was unchanged at 0.0% whilst there was a fall in the Northern Territory by -1.3%.

Also release in Asian session, Japan overall household spending rose 2.8% yoy in August, versus expectation of 0.2% yoy. Labor cash earnings rose 0.9% yoy versus expectation of 1.3% yoy.

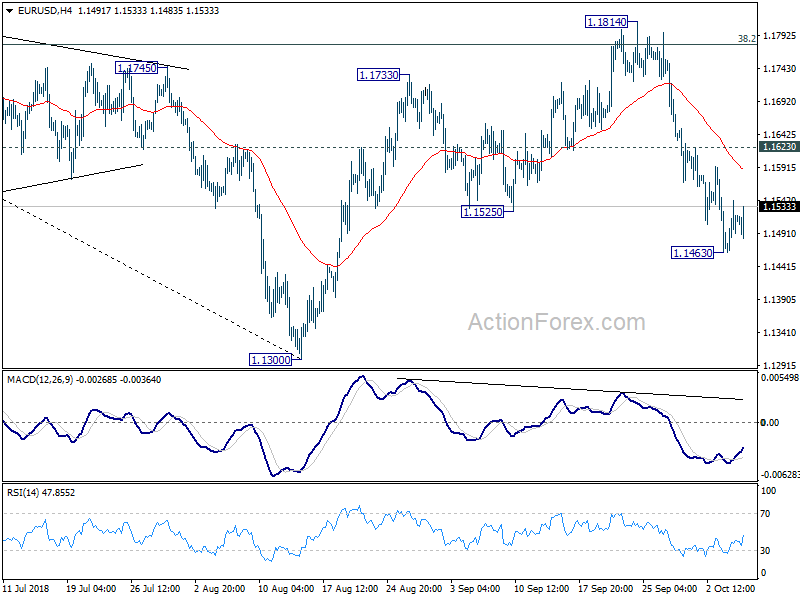

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1470; (P) 1.1507; (R1) 1.1550; More…..

EUR/USD is staying in consolidation above 1.1463 temporary low and intraday bias remains neutral. Further recovery could be seen but upside should be limited below 1.1623 resistance to bring another decline. On the downside, break of 1.1463 will extend the fall from 1.1814 to retest 1.1300 low.

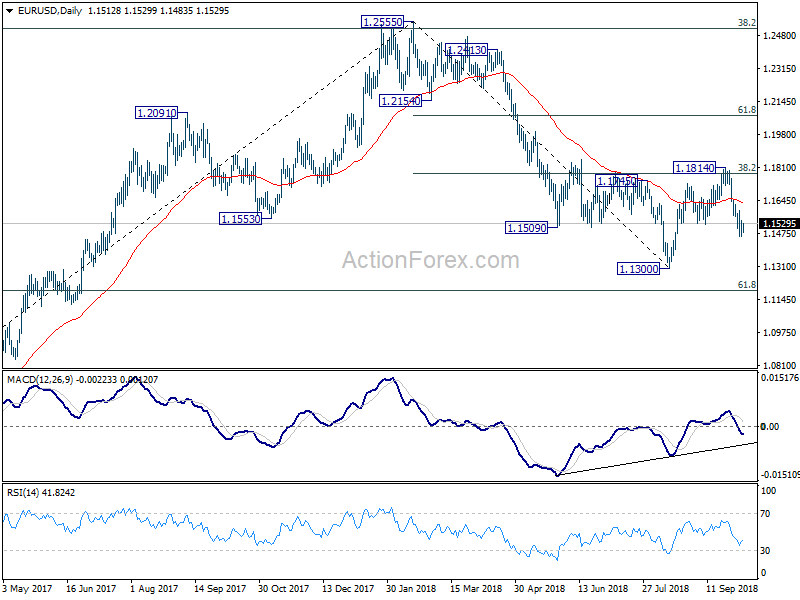

In the bigger picture, a medium term bottom should be in place at 1.1300, on bullish convergence condition in daily MACD and some consolidations would be seen. But still, note that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. That carries some long term bearish implications. Thus, we’d expect fall from 1.2555 high to resume after consolidation completes. Below 1.1300 should send EUR/USD through 61.8% retracement of 1.0339 to 1.2555 at 1.1186. And, in that case, EUR/USD would head to retest 1.0339 (2017 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Aug | 2.80% | 0.20% | 0.10% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y Aug | 0.90% | 1.30% | 1.50% | 1.60% |

| 01:30 | AUD | Retail Sales M/M Aug | 0.30% | 0.30% | 0.00% | |

| 05:00 | JPY | Leading Index CI Aug P | 104.40% | 104.30% | 103.90% | |

| 06:00 | EUR | German Factory Orders M/M Aug | 2.00% | 0.70% | -0.90% | |

| 06:00 | EUR | German PPI M/M Aug | 0.30% | 0.20% | 0.20% | |

| 06:00 | EUR | German PPI Y/Y Aug | 3.10% | 2.90% | 3.00% | |

| 07:00 | CHF | Foreign Currency Reserves Sep | 740B | 731B | ||

| 07:15 | CHF | CPI M/M Sep | 0.10% | 0.00% | 0.00% | |

| 07:15 | CHF | CPI Y/Y Sep | 1.00% | 1.20% | 1.20% | |

| 12:30 | CAD | Net Change in Employment Sep | 63.3K | 32.5K | -51.6k | |

| 12:30 | CAD | Unemployment Rate Sep | 5.90% | 5.90% | 6.00% | |

| 12:30 | CAD | International Merchandise Trade (CAD) Aug | 0.5B | -1.4B | -0.1B | -0.2B |

| 12:30 | USD | Trade Balance Aug | -53.2B | -52.3B | -50.1B | -50.0B |

| 12:30 | USD | Change in Non-farm Payrolls Sep | 134K | 188K | 201K | 270K |

| 12:30 | USD | Unemployment Rate Sep | 3.70% | 3.80% | 3.90% | |

| 12:30 | USD | Average Hourly Earnings M/M Sep | 0.30% | 0.30% | 0.40% | 0.30% |