{kind=link}

Euro recovers broadly today on new that the final version of Italy’s budget could be less worse than originally reported. More details could be published today and we’ll see how the common currency, as well as German and Italian yield react. Meanwhile, Sterling also recovers as markets prefer for UK PM Theresa May’s speech at the Conservative Party Conference in Birmingham. For now, New Zealand and Australian Dollar are the weakest ones today, followed by Swiss Franc.

Asian markets continue to trade in risk averse mode today. Hong Kong HSI is extending yesterday’s steep decline and is down -0.52% at the time of writing. Nikkei is down -0.71%. But Singapore Strait Times is up 0.80%. Overnight, DOW made record high at 26824.78 before closing at 26773.94, up 0.46%. However, S&P 500 dropped -0.04% while NASDAQ lost -0.47%. Treasury yield also closed lower with 10-year yield down -0.024 at 3.056. Gold on the other hand, rebounded strongly and is back above 1200 at 1205.7.

Technically, the triangular relationship of Dollar, Euro and Yen is a development to watch today. EUR/USD’s break of 1.1525 support yesterday was bearish. EUR/JPY breached 130.86 support but quickly recovered, maintaining near term bullishness. USD/JPY lost momentum after hitting 114.05 and is now in near term consolidation. It remains to be see if deeper pull back in USD/JPY would drag down EUR/JPY. Or rebound in EUR/JPY would lift USD/JPY, in push EUR/USD higher instead. It’s very interactive.

Euro recovers as Italy may tame their budget deficit target after 2019

Euro recovers broadly today on news that the detailed version of Italy’s budget is not as bad as it’s initially reported. 5-Star Movement leader Luigi Di Maio has made himself clear that the coalition government is “not not turning back from the 2.4 percent target” referring top budget deficit in terms of GDP. However, it’s reported the coalition has tweaked to plan to cut percentage down the road.

The final version could be budget deficit at 2.4% of GDP in 2019, then 2.2% in 2020 and 2.0% in 2021. That would be, at least gesturally, better than the reported plan of 2.4% through the next three years. Though, firstly, whether the eurosceptic coalition would do it is in question. And, whether EU would accept it is another question.

Di Maio has indicated that some details on the so-called Economic and Financial Document would be defined on Wednesday morning. So we’d expect volatility in Euro to continue.

Fed Powell: Remarkably positive economic outlook to continue

Fed Chair Jerome Powell said in a speech yesterday there’s a “remarkably positive outlook” in the economy. And the forecasts are “not too good to be true”. The US is now in favorable condition with unemployment rate at near 20-year low at 3.9%. And Inflation is running near Fed’s target of 2%. A wide range of data and prices also supports a positive view while these favorable conditions are forecast to continue.

Powell added that the “historically rare pairing of steady, low inflation and very low unemployment is testament to the fact that we remain in extraordinary times”. And, Fed’s policy of “gradual interest rate normalization” showed the effort to balance the risks to extend the expansion, maintain maximum employment, low and stable inflation.

Fed Kaplan not advocating a pause after interest rate hits neutral

Dallas Fed President Robert Kaplan said he’s based case is for Fed hike once more this year and twice next year. And he added that “mathematically there’s at least a couple more increases” to get to his neutral rate of 2.50-2.75%. He also noted that he “not advocating a pause” from there. But rather, he’ll “make that judgment as we go; I haven’t decided yet.”

Additionally he reiterated his view that GDP will grow 3% this year and slow to 2.5% next as impact of fiscal stimulus fades. Also, he warned that the tailwind from debt-funded stimulus could turn into a headwind in the out years.

On the data front

Australia AiG performance of services index rose 0.3 to 52.5 in September. Building approvals dropped sharply by -9.4% mom in August. UK BRC shop price index rose 0.2% yoy in September.

Services data will be major focuses today. Eurozone will release PMI services final and retail sales. UK will release PMI services. US will release ISM non-manufacturing as well as ADP employment.

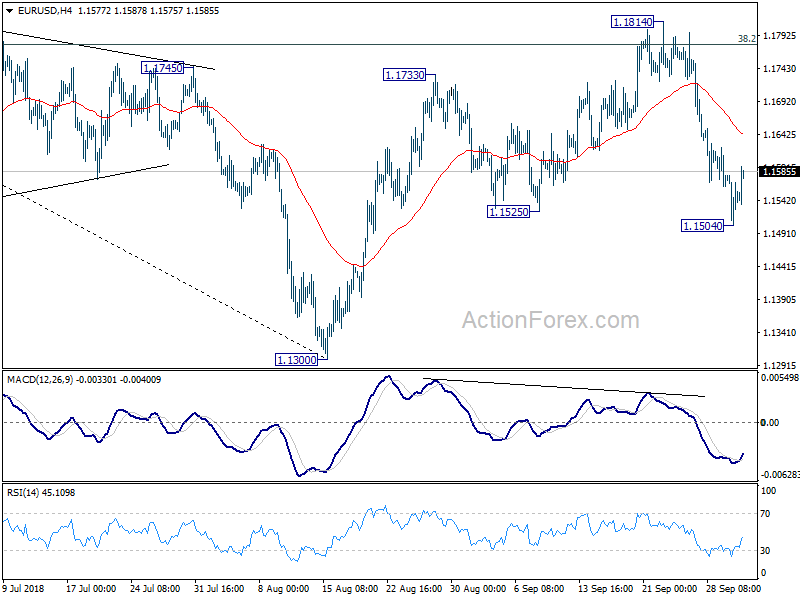

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1507; (P) 1.1544; (R1) 1.1584; More…..

EUR/USD recovers after hitting 1.1504 and formed a temporary low there. Intraday bias is turned neutral for consolidation first. Stronger recovery could be seen to 4 hour 55 EMA (now at 1.1643). But upside should be limited well below 1.1814 resistance to bring another decline. We maintain the view that corrective rise from 1.1300 has completed with three waves up to 1.1814 already. Below 1.1504 will target a test on 1.1300 low first.

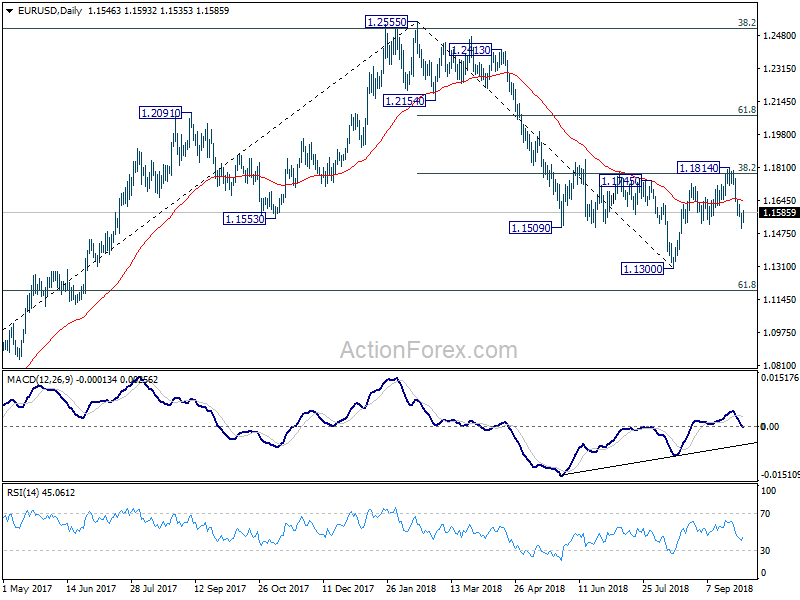

In the bigger picture, a medium term bottom should be in place at 1.1300, on bullish convergence condition in daily MACD and some consolidations would be seen. But still, note that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. That carries some long term bearish implications. Thus, we’d expect fall from 1.2555 high to resume after consolidation completes. Below 1.1300 should send EUR/USD through 61.8% retracement of 1.0339 to 1.2555 at 1.1186. And, in that case, EUR/USD would head to retest 1.0339 (2017 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Service Index Sep | 52.5 | 52.2 | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y Sep | 0.20% | 0.10% | ||

| 1:30 | AUD | Building Approvals M/M Aug | -9.40% | -2.50% | -5.20% | -4.60% |

| 7:45 | EUR | Italy Services PMI Sep | 52.4 | 52.6 | ||

| 7:50 | EUR | France Services PMI Sep F | 54.3 | 54.3 | ||

| 7:55 | EUR | Germany Services PMI Sep F | 55.3 | 55.3 | ||

| 8:00 | EUR | Eurozone Services PMI Sep F | 54.7 | 54.7 | ||

| 8:30 | GBP | Services PMI Sep | 53.9 | 54.3 | ||

| 9:00 | EUR | Eurozone Retail Sales M/M Aug | 0.20% | -0.20% | ||

| 12:15 | USD | ADP Employment Change Sep | 185K | 163K | ||

| 13:45 | USD | US Services PMI Sep F | 53.6 | 52.6 | ||

| 14:00 | USD | ISM Non-Manufacturing/Services Composite Sep | 58.3 | 58.5 | ||

| 14:30 | USD | Crude Oil Inventories | 1.9M |