{kind=link}

Dollar firms up broadly in early US session as markets are awaiting FOMC rate decision. A 25bps hike is widely expected and there is no change for Fed to disappoint. The tricky part is the new economic projections which could make or break Dollar’ rebound. At the time of writing, Yen and Canadian Dollar are trading as the second strongest ones. Swiss Franc suffers another day of deep, broad based selling today and it’s followed by Euro and the Sterling as the weakest ones. Australian Dollar was lifted rather briefly by the rebound in Chinese stocks earlier today. But it’s losing steam into US session.

In other markets, major European indices are mixed at the time of writing. FTSE is down -0.02%, DAX down -0.18% and CAC up 0.34%. Germany 10 year bund yield is down slightly by -0.008 at 0.539 but stays very firm above 0.5 handle. Earlier today, Nikkei closed up 0.39%, Singapore Strait Times up 0.09%, Hong Hong HSI up 1.15%. China Shanghai SSE rose 0.92% to 2806.81, closed above 2800 psychological level. In particular, SSE’s strong close above medium term channel resistance and 55 day EMA should have confirmed defending of 2638.30 key support (2016 low). Further rebound is now in favor in near term. Elsewhere, Gold is back at 1195 but it’s holding above 1187.58 near term support. Thus, another rise remains mildly in favor in near term through 1214.30.

Technically, in spite of the rebound attempt, no technical level is broken by the Dollar. EUR/USD is holding above 1.1723 minor support, GBP/USD above 1.3042, AUD/USD above 0.7228. USD/CAD is also held below 1.2975. More is needed for dollar to confirm its underlying bullish momentum. These mentioned levels will be watched closely for the rest of the session.

FOMC preview: Rate hike for sure, focus on new projections

Fed is widely expected to lift federal funds rate by 25bps to 2.00-2.25% today, without a doubt. The voting will be a point to note to seen how impatient the doves were. But it’s more likely to be unanimous than not at this stage. Also, there are expectations of a slight change in the language. That is, “the stance of monetary policy remains accommodative” could be changed to “somewhat accommodative” or even dropped. But this won’t trigger much market reactions, changed or not.

The major focuses will be on the new economic projections. Firstly, 2021 figures will be released. Based on June’s projections, medium projected appropriate federal funds rate will be at 3.4% by the end of 2020. We’d be eager to know if Fed policy makers expect to stop there through 2021, or they would lean towards more tightening ahead. (Btw, at 3.4% which is above 2.9% projected longer run rate, that’s tightening. Now, it’s just accommodation removal, totally different stage.)

Secondly, while all the figures, inflation, growth, unemployment, policy path matter, we believe the key is on the 2.9% estimated longer run rate. From the communications of Fed officials, the general consensus is for Fed to raise interest rate to “neutral” and see how it goes from there. A raise in the estimated longer run rate will be tied to a perceived higher neutral rate. And that would be, Fed’s rate hike cycle would likely be prolonged further. To us, this is the single most important figure that moves markets.

Here are some suggested readings on FOMC:

- Trump Makes Mark At UN, But Prepare For FOMC Outcome

- What To Look For In Markets Ahead Of Dot Plot

- Fed Preview: Near-Term Path Set in Stone, All Eyes on 2019 and Beyond

- Fed ‘Certain’ to Raise Rates, Optimistic Commentary Likely on Tap

- Greenback’s Path Hinges On The Fed’s Dot Plot

- FOMC Preview: Destination Neutral

ECB Praet: Market curve on interest rate fully coherent with ECB objective

ECB Chief Economist Peter Praet talked again today. He said in a Reuters television interview that on growth, “risks are mounting”. Though, he also noted “so far we haven’t seen any impact on real data… I’m not excessively worried.” He also reiterated the central bank’s base scenario, “where inflation is going to converge towards 2 percent, is conditional on very easy financial conditions in general.”

Financial markets are seeing ECB’s first rate hike in around next October. Praet gave a nod and said “the market curve that we see today, the interest rate curve, is fully coherent with the objective we have.” He added, “you’re going to have low rates for some period of time.”

Praet also dismissed the rhetorics of Italian government officials and politicians on fiscal spending. He said “in Italy, we have a very big contrast between the communication, words, and the deeds.” And, “The key information will be on the budget, so we have to see those figures. The pension reform is quite an important element in the picture.”

China announces tariff reductions and measures to promote foreign investment and trade

China’s State Council announced measures to promote foreign investment projects, lower tariffs on some commodities and speed up customs clearance processes. It should be noted that while lowering of tariffs catches most headlines, there are other measures that would be welcomed by foreign companies doing business in and with China. It’s clearly a gesture for its trade and economic partners like the EU that China is speeding reform and opening up the markets further. At the same time, China is maintaining its firms stance in against Trump’s bullying in trade war.

On promoting “predictable and attractive” environment for foreign investments, China pledged to deepen the reform of “distribution management” and treat foreign and domestic capital equally. Secondly, China will encourage foreign re-investments by expanding the coverage of withholding tax exemptions. Thirdly, China pledged to protect vigorously protect intellectual property rights and further standardize government supervision and enforcement.

Starting November 1, China will lower tariffs of 1585 product lines, including machinery, paper, textiles and construction materials. The reduction should reduce tax burden on enterprises and consumers by nearly CNY 60B. And, total tariff level of China will be reduced from 9.8% in 2017 to 7.5%.

Average rate for electromechanical equipment will be lowered from 12.2% to 8.8%. Average tax rate for textiles, building materials will be cut from 11.5% to 8.4%. Average tax rate for some resource products and primary processed products such as paper products will but reduced from 6.6% to 5.4%.

Also, starting November 1, customs clearance process will be simplified. Number of regulatory documents required for verification will be nearly halved from 86 to 48. Non-compliances charges will be standardized and announced before the end of October.

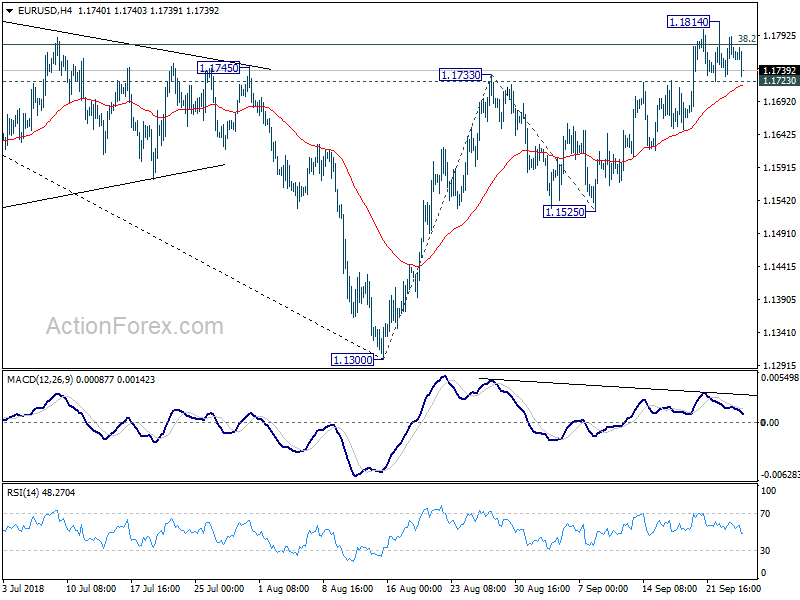

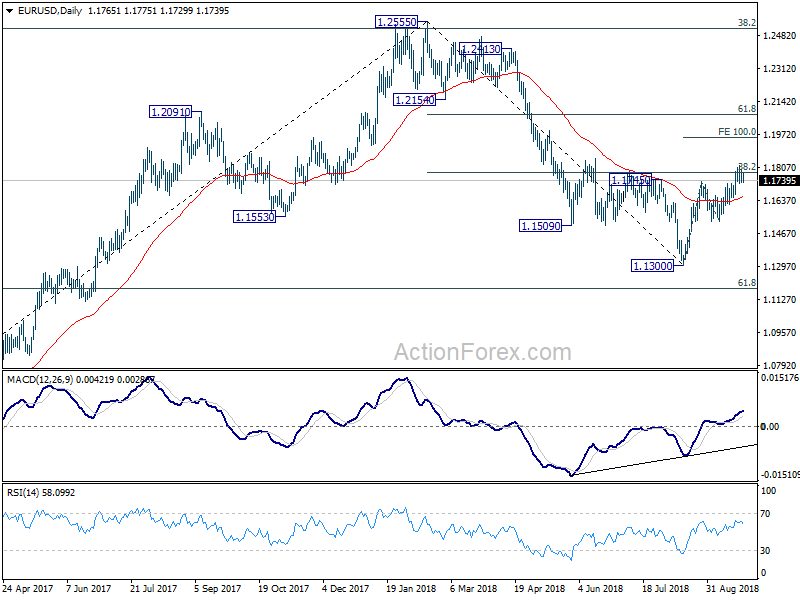

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1734; (P) 1.1763; (R1) 1.1796; More…..

EUR/USD dips notably in early US session but it’s staying in tight range of 1.1723/1814. Intraday bias stays neutral at this point. On the downside, break of 1.1723 minor support will suggest rejection by 38.2% retracement of 1.2555 to 1.1300 at 1.1779. In such case, intraday bias will be turned back to the downside for 1.1525 support. However, sustained break of 1.1779 will pave the way to 100% projection of 1.1300 to 1.1733 from 1.1525 at 1.1958.

In the bigger picture, a medium term bottom should be in place at 1.1300, on bullish convergence condition in daily MACD and some consolidations would be seen. But still, note that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. That carries some long term bearish implications. Thus, we’d expect fall from 1.2555 high to resume after consolidation completes. Below 1.1300 should send EUR/USD through 61.8% retracement of 1.0339 to 1.2555 at 1.1186. And, in that case, EUR/USD would head to retest 1.0339 (2017 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Aug | -1484M | -930M | -143M | -196M |

| 1:00 | NZD | ANZ Business Confidence Sep | -38.3 | -50.3 | ||

| 8:30 | GBP | BBA Mortgage Approvals Aug | 39.4K | 39.7K | 39.6K | |

| 10:00 | GBP | CBI Reported Sales Sep | 23 | 18 | 29 | |

| 14:00 | USD | New Home Sales Aug | 630K | 627K | ||

| 14:30 | USD | Crude Oil Inventories | -2.1M | |||

| 18:00 | USD | FOMC Rate Decision (Upper Bound) | 2.25% | 2.00% | ||

| 18:00 | USD | FOMC Rate Decision (Lower Bound) | 2.00% | 1.75% | ||

| 18:30 | USD | FOMC Press Conference | ||||

| 21:00 | NZD | RBNZ Official Cash Rate | 1.75% | 1.75% |