The forex markets are trading steadily today, as another week starts as usual. Major pairs and crosses are so far still bounded in Friday’s range. It seems that traders took the news regarding escalation in US-China trade war rather lightly. Or, it’s actually widely expected that no matter his colleagues say, Trump is going to march on with tariffs war. For now, New Zealand Dollar is the strongest one, followed by Euro and then Yen. Canadian Dollar is the weakest, followed by Dollar and then Swiss Franc. But this picture could easily change, and drastically, as volatility kicks in.

In other markets, Asian markets are generally lower, with exception of Nikkei which is on holiday. Singapore Strait Times is down -0.65%, Hong Kong HSI is down -1.58% at the time of writing. China Shanghai SSE is losing -1.06% at 2653.15. Last week’s low at 2647.17 is a level SSE would challenge soon. But the key level lies in 2638.30, 2016 low. Gold is bounded in tight range at around 1195. As long as 1187.58 support holds, recent rebound from 1160.36 is still in favor to extend through 1214.30 at a later stage.

Technically, the key development to watch is whether Dollar would extend Friday’s rebound to build up some momentum. EUR/USD is in the middle of range of 1.1525/1733. AUD/USD is inside 0.7084/7228. USD/CHF is inside 0.9633/9757. For now, it’s hard to tell which side Dollar would take on first.

Trump to announce new tariffs on China as soon as Monday

Over the weekend, Reuters reported that, based on unnamed source, Trump is ready to announce the next round of tariffs on USD 200B in Chinese goods, as soon as on Monday. However, the tariff rate could be at 10%, which is much lower than the 25% rate Trump intended to impose. There is no comment from the White House on the news yet. At the same time, Treasury Secretary Steven Mnuchin is restarting trade talks with China, involving Vice Premier Liu He, possibly on around September 20.

The WSJ reported that Chinese government may reject to re-start trade talks with the US if Trump imposes new tariffs. An unnamed Chinese official was quoted saying the country would not negotiation “with a gun pointed to its head”. In addition, other unnamed officials said China could impose export restraints on some supplies needed by US businesses, to disrupt their supply chain.

It doesn’t matter if the new round of tariffs are imposed before or after the meeting. As long as they are imposed, anything agreed during the meeting will not take effect for sure.

Separately, the PBoC surprisingly injected CNY 265B in liquidity to the markets via its one-year medium-term lending facility (MLF) today. Interest rate was unchanged at 3.30%. It’s an unexpected move because no MLF loans were due to expire today.

BCC downgraded UK growth forecasts, economy to grow at a snail’s pace

The British Chambers of Commerce downgraded UK growth forecasts, citing “weaker outlook for trade and investment” as main reasons. Key points in the new forecasts:

- 2018 GDP growth at 1.1%, down from 1.3%. 2019 GDP growth at 1.3%, down from 1.4%. 2020 GDP growth at 1.6%, unchanged.

- 2018 exports growth at 1.7% only, down from 2.8% in prior forecast.

- 2018 total investment growth at 1.4%, down from 1.8%. 2019 at 1.4% and 2020 at 1.5%.

- BoE expected to hike in Q1 2019 and Q2 2020. Bank rate to hit 1.25% by the end of the forecast period.

Adam Marshall, Director General of the BCC said that the UK economy as a whole is set to grow at a “snail’s pace”. Brexit uncertainty “continues to weigh heavily on many firms” as “most of the practical questions” remained unanswered. And, the “lack of precision” of future relationship with the EU “is lowering expectations for both business investment and export growth.” He also warned that “the drag effect on investment and trade would intensify in the event of a ‘messy’ and disorderly Brexit”.

Looking ahead – BoJ and SNB to stand pat

Two central bank meetings will be featured this week, BoJ and SNB. Both are expected to keep policy unchanged. In particular, recent surge in the Swiss Franc highlighted that the markets are still vulnerable to different risks, emerging markets this time. There is no room for complacency for SNB. RBA minutes will also be watched but they shouldn’t do anything to alter RBA’s neutral stance. There is no urgency for RBA to make any rate move in the near term, even though the next move will be a hike.

There are also some important economic data featured in the week. UK CPI and retail sales, Canada CPI and retail sales, Japan CPI, Eurozone PMIs and New Zealand GDP will be watched.

Here are some highlights for the week:

- Monday: Eurozone CPI final; Canada foreign securities purchases; US Empire State manufacturing index

- Tuesday: RBA minutes, Australia house price index; Canada manufacturing sales; US NAHB housing index

- Wednesday: Japan trade balance, BoJ rate decision; Swiss SECO economic forecasts; Eurozone current account; UK CPI, PPI, house price index; US new residential construction, current account

- Thursday: New Zealand GDP; Swiss trade balance, SNB rate decision; UK retail sales; US Philly Fed survey, jobless claims, leading indicator, existing home sales

- Friday: Japan CPI, PMI manufacturing, all industry index; Eurozone PMIs; UK public sector net borrowing; Canada CPI, retail sales; US PMIs

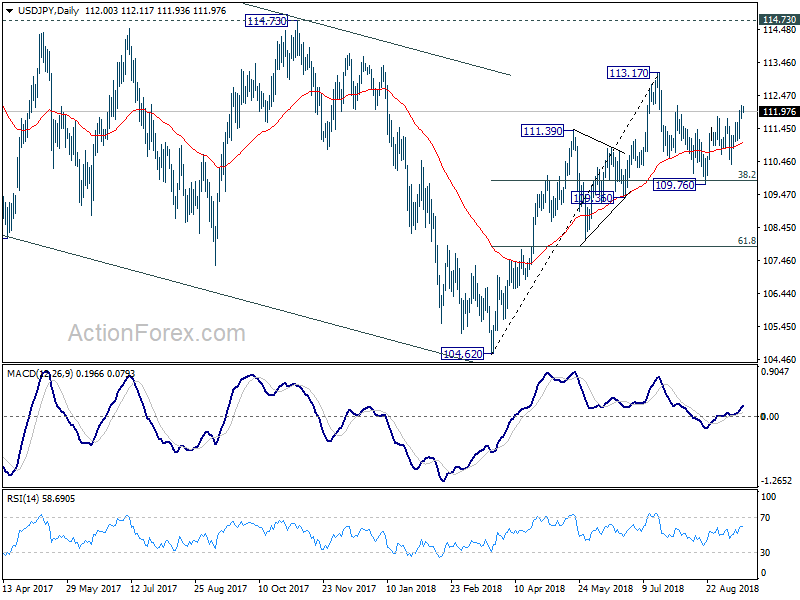

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.82; (P) 112.00; (R1) 112.24; More…

Intraday bias in USD/JPY remains on the upside at this point. Current rebound from 109.76 is in progress for 100% projection of 109.76 to 111.82 from 110.37 at 112.43 first. Break will target a test on 113.17 high. On the downside, break of 111.10 minor support is needed to signal completion of the rebound. Otherwise, near term outlook is cautiously bullish in case of retreat.

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.36 support holds. However, decisive break of 109.36 will mix up the outlook again. And deeper fall should be seen back to 61.8% retracement of 104.62 to 113.17 at 107.88 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Sep | 0.70% | -2.30% | ||

| 9:00 | EUR | Eurozone CPI M/M Aug | -0.30% | -0.30% | ||

| 9:00 | EUR | Eurozone CPI Y/Y Aug F | 2.10% | 2.10% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y Aug F | 1.00% | 1.00% | ||

| 12:30 | CAD | International Securities Transactions (CAD) Jul | 4.35B | 11.55B | ||

| 12:30 | USD | Empire State Manufacturing Index Sep | 23.2 | 25.6 |

{kind=link}