{kind=link}

Market sentiments seem to be hurt by news that China is set to seek WTO backing next week to slap sanctions on the US. The sanctions would be for non-compliance with a WTO ruling over US dumping duties, which China won in 2016. The case was then confirmed in 2017 after the US appealed. Some took that as a signal that China is not going to back down. But indeed, neither side expressed any message that they’re going to soften their stance. Trump is ready to impose 25% tariffs on USD 200B in Chinese import any time, as public hearing ended last week already. China is also well prepared for retaliation on USD 60B of US goods, with tariffs from 5% to 25%. Trump is also ready to start the process for tariffs on another USD 267B in Chinese products. Then no more products to tariff, China would seek other measures to counter. The plot is already written, at least until US mid-term elections.

With trade war back in the headlines, Dollar is trading as the strongest one for today, followed by Swiss Franc. Canadian Dollar is the third strongest. Foreign Minister Chrystia Freeland is back in Washington to restart trade talk with the US. But there is little expectation for breakthrough. Sterling was lifted by stronger than expected wage growth earlier today but it’s now trading in red against all others as rally lost steam. Australian Dollar and New Zealand Dollar are the next weakest.

In other markets, major European indices are all in red today. FTSE is currently down -0.56%, DAX down -0.65%, CAC down -0.39%. German-Italian yield spread continues to widen, signaling calmness regarding Italy’s deficit. In Asia, Nikkei gained 1.3% to 22664.69. But Hong Kong HSI lost -0.72% while Singapore Strait Times dropped -0.35%. In particular, China Shanghai SSE dropped -0.18% to 2664.8, below August’s lowest close at 2668.96. Key support level at 2638.30 (2016 low) looks rather vulnerable. And it seems, investors are preparing themselves well for escalation in US-China trade war.

UK wage growth picked up more than expected

Sterling extends this week’s strong rally as boosted by stronger than expected wage growth. Average weekly earnings including bonus rose 3.6% 3moy in July, up from 2.4% and beat expectation of 2.5%. Weekly earnings excluding bonus rose 2.9% 3moy, accelerated from 2.7% and beat expectation of 2.7%. Unemployment rate was unchanged at 4.0% as expected. In August, claimant count rose 8.7k, above expectation of 3.6k.

ONS statistician David Freeman said that “earnings have grown faster than prices for several months, especially looking at pay excluding bonuses”. Also, “the labour market remains robust, with the number of people working still at historically high levels.”

BoE Governor Carney extends his term till Jan 2020

The UK Treasury announced today that BoE Governor Mark Carney will extend his term until January 2020. Carney has originally planned to step down in June 2019. Chancellor of Exchequer Philip Hammond said in the release that I’m delighted that the Governor has agreed to stay in his role for a further seven months to support a smooth exit from the European Union and provide vital stability for our economy. In the same release, Jon Cunliffe was re-appointed as Deputy Governor till October 2023.

Carney said in a letter to Hammond saying “I recognize that during this critical period, it is important that everyone does everything they can to support a smooth and successful Brexit.” And, “accordingly, I am willing to do whatever I can in order to promote both a successful Brexit and an effective transition at the Bank of England and I can confirm that I would be honored to extend my term to January 2020.”

UK PM May: Salzburg EU meeting a staging post for Chequers Brexit plan

According to UK Prime Minister Theresa May’s spokesman, she will travel to Salzburg next Wednesday to attend an EU informal council. And, that will be “both a staging post in exit negotiations and an opportunity to engage with the rest of the EU on shared challenges”.

Also, referring to the Chequers plan, “it will also be the first time the leaders will discuss together the UK government’s white paper which put forward a series of credible and serious proposals.”

German ZEW economic sentiment jumped to -10.6 as considerable fears diminished somewhat

German ZEW Economic Sentiment improved to -10.6 in September, up from -13.7 and beat expectation of -13.4. Current Situation index rose to 76.0, up from 72.6, above expectation of 72.3. Eurozone ZEW Economic Sentiment rose to -7.2, up from -11.1, beat expectation of -14.9. Current Situation index rose 1.7 pts to 31.7.

ZEW President Professor Achim Wambach noted in the release that “during the survey period, the currency crises in Turkey and Argentina intensified, while German industrial production and incoming orders were surprisingly low in July.” However, “despite these unfavourable circumstances, economic expectations for Germany improved slightly.” And “the considerable fears displayed by the survey participants regarding the economic development have diminished somewhat, which may in part be attributable to the new trade agreement between the USA and Mexico”.

Also from Eurozone, employment rose 0.4% qoq, 1.5% yoy in Q2 versus expectation of 0.4% qoq, 1.4% yoy.

German FM Scholz urged to complete EU banking union this year

German Finance Minister Olaf Scholz urged EU to make progress on banking union this year. He said in the Bundestag lower house of parliament that “we must take action so that we can act in a new crisis – not everything has been done.” Scholz also said Germany and France laid a foundation with an agreement in Meseberg in June. And so, “we can quickly take the last steps to make Europe stable and to equip ourselves for the next crisis”.

He added that ‘have the task of completing a banking union and we should fulfil the most important steps this year.” Under the current EU plan, the Single Resolution Board will be given a clearer mandate to set the level of capital buffers that banks should hold against the risk of failure. However, another pillar of the union, a common bank deposit insurance scheme, is not agreed upon yet.

Australia NAB business confidence hit 2-year low, but business condition rebounded

Australia NAB Business Confidence dropped to 4 in August, down from 7and missed expectation of 5. That’s a two year low since August 2016, and it’s below long-run average. Confidence is lowest in wholesale and manufacturing, highest in mining and construction. And, confidence declined across all states except Western Australia and Queensland in the month, with New South Wales and Victoria continue to lag.

However, Business Condition rose to 15, up from 12 and matched expectations. Results were driven by increases in the profitability and trading indices. Forward looking indicators also rebounded a little in the month. Surveyed price and wage variables continue to show a gradual building of inflationary pressures.

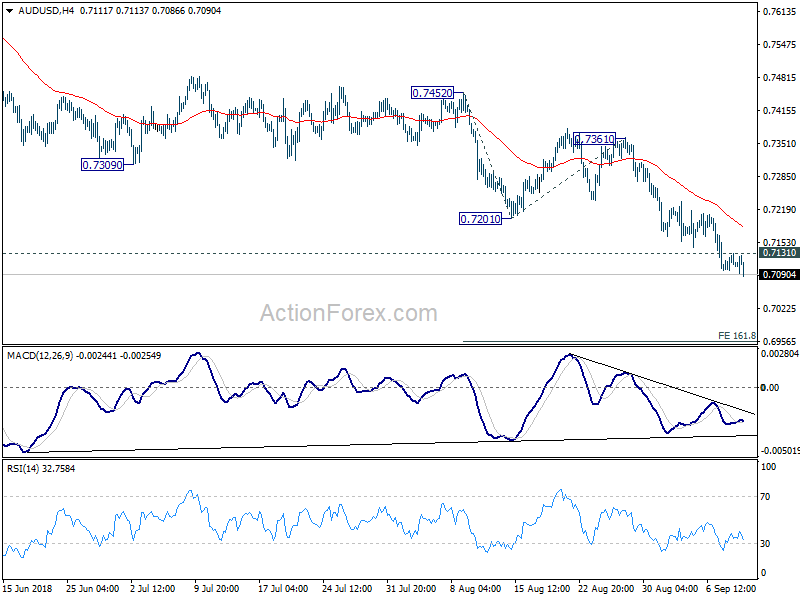

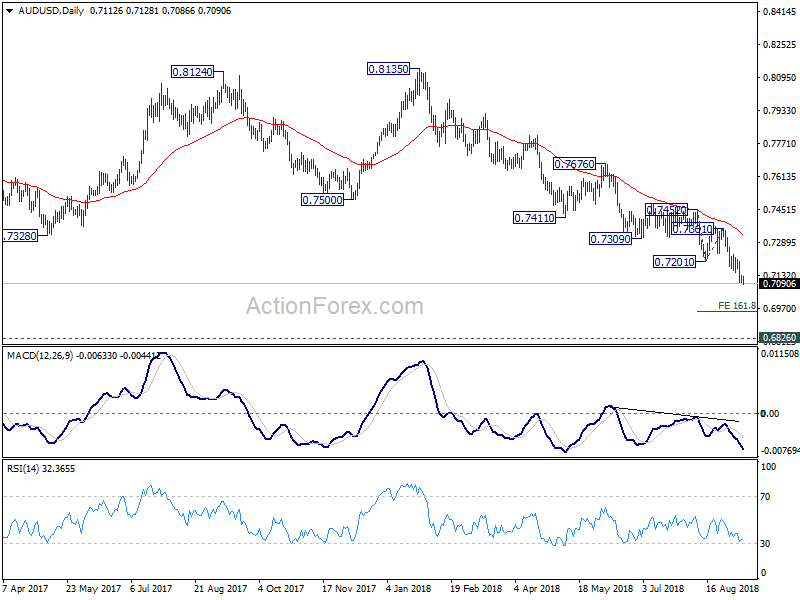

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7097; (P) 0.7115; (R1) 0.7131; More…

AUD/USD’s decline resumes after brief consolidation and reaches as low as 0.7086 so far. Intraday bias remains on the downside. Current fall is part of the down trend from 0.8135. Next target is 161.8% projection of 0.7452 to 0.7201 from 0.7361 at 0.6955. Break will target key support level at 0.6826. On the upside, above 0.7131 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, rebound from 0.6826 (2016 low) is seen as a corrective move that should be completed at 0.8135. Fall from there would extend to have a test on 0.6826. There is prospect of resuming long term down trend from 1.1079 (2011 high). Current downside momentum as seen in daily and weekly MACD support this bearish case. Firm break of 0.6826 will target 0.6008 key support next (2008 low). On the upside, break of 0.7361 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will remain bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Aug | 2.90% | 3.00% | 3.00% | 2.90% |

| 01:30 | AUD | NAB Business Conditions Aug | 15 | 15 | 12 | |

| 01:30 | AUD | NAB Business Confidence Aug | 4 | 5 | 7 | |

| 04:30 | JPY | Tertiary Industry Index M/M Jul | 0.10% | 0.10% | -0.50% | -0.60% |

| 08:30 | GBP | Jobless Claims Change Aug | 8.7K | 3.6K | 6.2K | |

| 08:30 | GBP | Claimant Count Rate Aug | 2.60% | 2.50% | ||

| 08:30 | GBP | Average Weekly Earnings 3M/Y Jul | 2.60% | 2.50% | 2.40% | |

| 08:30 | GBP | Weekly Earnings ex Bonus 3M/Y Jul | 2.90% | 2.70% | 2.70% | |

| 08:30 | GBP | ILO Unemployment Rate 3Mths Jul | 4.00% | 4.00% | 4.00% | |

| 09:00 | EUR | German ZEW Economic Sentiment Sep | -10.6 | -13.4 | -13.7 | |

| 09:00 | EUR | German ZEW Current Situation Sep | 76 | 72.3 | 72.6 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Sep | -7.2 | -14.9 | -11.1 | |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q2 | 0.40% | 0.40% | 0.40% | |

| 09:00 | EUR | Eurozone Employment Change Y/Y Q2 | 1.50% | 1.40% | 1.40% | |

| 12:15 | CAD | Housing Starts Aug | 201K | 218K | 206K | |

| 14:00 | USD | Wholesale Inventories M/M Jul F | 0.70% | 0.70% |