{kind=link}

Sterling opens the weak broadly lower and stays soft after EU chief Brexit negotiator Michel Barnier said he “strongly opposed” to UK’s impractical plan. The Pound has been sensitive to any Brexit headlines and will continue to be so. New Zealand Dollar is the second weakest one. But Canadian Dollar is not too far away after trade talk with the US failed. Yen is trading as the strongest one on risk aversion. Economic data released in Asia Pacific were generally not too supportive. Euro and Australian Dollar are generally higher, next to Yen, and these two are paring last week’s steep losses.

In other markets, Nikkei closed down -0.69% at 22707.38. It’s now getting farther away from 23050 key near term resistance. China Shanghai SSE is down -0.38% at the time of writing. Hong Kong HSI is down -0.83% and Singapore Strait Times is down -0.37%. 10 year JGB yield is rising for another day, up 0.011 to 0.12%. This is another Yen supportive factor too. WTI crude oil breached 70 to 70.5 last week but it’s now back at 69.65. Gold is hovering around 1200 as consolidation continues.

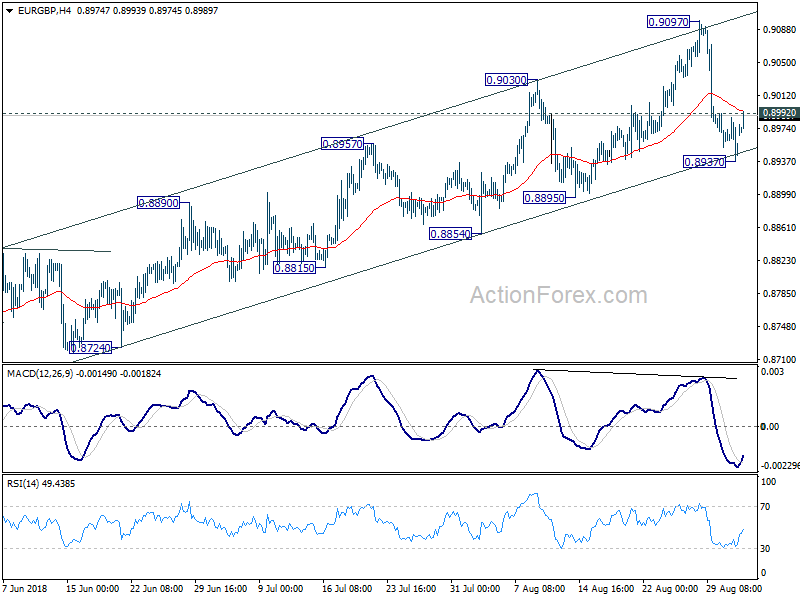

Technically, one development to note is EUR/GBP’s rebound after drawing support from channel support. With 0.8992 minor resistance breached, the cross is possibly heading back to 0.9097 resistance And with the near term rising channel supported, outlook stays bullish for further rally. USD/CAD will be facing near term channel resistance at 1.3098 soon. Decisive break there will suggests that recent correction from 1.3385 has completed and could pave the way to retest this high.

Sterling weakens broadly as EU Barnier blasted Theresa May’s Chequers plan

Sterling opened the week broadly lower after EU chief Brexit negotiator Michel Barnier blasted UK Prime Minister Theresa May’s . And, Barnier “strongly opposed” May’s proposals. On the customs proposals, Barnier said its “not practical”. He added, “it is impossible to tell exactly where a product ends up, on the UK market or in the internal market.” And, “the British proposal would be an invitation to fraud if implemented.”

He also criticized that the “common rulebook” idea as outdated with modern world of trade. He said “the interest of Europeans is to preserve the integrity of the common market. That is our special strength and the reason why we are respected throughout the world, even in the United States.” He added “we have a coherent market for goods, services, capital and people – our own ecosystem that has grown over decades. You cannot play with it by picking pieces.” Therefore, the EU must prevent unfair competition if the United Kingdom has weaker legal requirements than we do. Otherwise we would discriminate and weaken our own companies.”

On the other hand, a UK government spokeswoman defended that the proposal is “precise, pragmatic and that will work for the UK and the EU.” And, “this proposal achieves a new balance of rights and obligations that fulfils our joint ambition to establish a deep and special partnership once the UK has left the EU while preserving the constitutional integrity of the UK. There is no other proposal that does that.

Trump slammed Canada and NAFTA, but the messages were for the Congress

The trade negotiation between US and Canada ended last week without any conclusion. Trump has already notified the Congress of his intent to sign a bilateral trade agreement with Mexico, which is called the United States- Mexico Trade Agreement. US-Canada trade negotiations will resume this Wednesday.

Over the weekend, he slammed Canada and NAFTA with his tweets. He said “there is no political necessity to keep Canada in the new NAFTA deal. If we don’t make a fair deal for the U.S. after decades of abuse, Canada will be out.” And, “Congress should not interfere w/these negotiations or I will simply terminate NAFTA entirely & we will be far better off.” Trump added “we were far better off before NAFTA — should never have been signed. Even the Vat Tax was not accounted for. We make new deal or go back to pre-NAFTA!”

While Canada was the topic of the tweets, the messages were clearly to the Congress. For now, it’s uncertain how Trump could get the US-Mexico trade deal through the Congress, without the involvement of Canada. Last Friday, chief executive of the U.S. Chamber of Commerce, Thomas Donohue also said in a statement that “anything other than a trilateral agreement won’t win Congressional approval and would lose business support.”

Democrat House minority leader Nancy Pelosi also said “actually fixing NAFTA requires reaching a trade agreement with both Mexico and Canada,” “without a final agreement with Canada, the administration’s work is woefully incomplete.”

Japan PMI manufacturing finalized at 52.5, potential escalations in trade conflict weigh on sentiment

Japan PMI manufacturing was finalized at 52.5 in August, unrevised, up from July’s 52.3. Markit noted in the released that “production rises amid faster new order growth”, “export orders fall for second time in three months”, and “geopolitical risks weigh on business sentiment”.

Joe Hayes, Economist at IHS Markit, noted that the “goods-producing sector continued to record growth at the midway point in Q3”. That extended the current stretch of expansion to two years – the “longest since the global financial crisis”. But he also pointed out that “upturn in demand was domestic-led,” with “export sales falling over the month.” And, “potential escalations in trade conflict also contributed to a softening of business confidence.”

However, the so called softening business confidence was not quite reflected in other data. Japan capital spending has increased 12.8% in Q2, nearly double of expectation of 6.6% and almost four times of prior quarter’s 3.4%.

Mixed Australia data: Retail sales missed, manufacturing PMI rose

Australian Dollar weakened in early Asian session after mixed economic data. But Aussie quickly recovered, partly helped by oversold conditions. On the negative side, retails sales rose 0.0% mom in July, below expectation of 0.3% mom. There were falls in three of the six industries, including household goods retailing (-1.2%), clothing, footwear and personal accessory retailing (-2.0%) and department stores (-1.9%). The declines were offset by other retailing (1.7%), food (0.3%) and cafes, restaurants and takeaway food services (0.6%)”. Also, ANZ job advertisements dropped -0.6% mom in August. That could point to easing momentum in job growth.

On the positive side, AiG Performance of Manufacturing Index rose 4.7 pts to 56.7 in August, indicating faster growth across the manufacturing sector. In particular, exports sub-index has jumped 8.5 points to 58.4 points. However, drought conditions in New South Wales and Queensland are now having an adverse impact on input costs and sales for some manufacturers. Company operating profits rose 2.0% qoq in Q2. TD securities inflation rose 0.1% mom in August.

New Zealand Terms of Trade rose only 0.6% qoq, missed expectations

New Zealand Dollar weakens broadly today and stays generally weak as Terms of Trade Index rose only 0.6% qoq in Q2, versus expectation of 1.1% qoq. Prior quarter’s figure was also revised down from 1.9% qoq to -2.0% qoq. Looking at the details, export prices for goods rose 2.4%, while import prices for goods rose 1.7%. Seasonally adjusted goods export volumes rose 1.1%, and goods import volumes rose 0.9%. Seasonally adjusted goods export values rose 3.0%, and goods import values rose 1.7%.

China Caixin PMI manufacturing dropped to 50.6, Economy facing obvious downward pressure

China Caixin PMI manufacturing dropped -0.2 to 50.6 in August, missed expectation of 50.7. In the release, it’s noted that “output expands at faster pace… but new order growth weakens and employment continues to decline”. Also, confidence towards the 12-month business outlook remains lacklustre”. Also it’s the third straight month of decline and the lowest level since June 2017.

Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group noted that “the manufacturing sector continued to weaken amid soft demand, even though the supply side was still stable”. Also, “worsening employment situation is likely to have an impact on consumption growth.” He warned that “China’s economy is now facing relatively obvious downward pressure.”

Looking ahead

Swiss will release retail sales and PMI manufacturing today. Eurozone will release PMI manufacturing revision. But the biggest mover could be UK PMi manufacturing. Meanwhile, US and Canada are on bank holiday.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8932; (P) 0.8960; (R1) 0.8985; More…

EUR/GBP’s breach of 0.8992 minor resistance suggests that pull back from 0.9097 has completed at 0.8937, after drawing support from near term rising channel. Intraday bias is turned back to the upside for retesting 0.9097 first. Break will extend the larger rally from 0.8620 towards 0.9305 high. Over all, outlook will remain bullish as long as 0.8895 support holds. However, sustained break of channel support, followed by break of 0.8895, will argue that whole rise from 0.8620 has completed. And consider that it’s not clearly impulsive in structure, break of 0.8895 will also suggest reversal and turn outlook bearish.

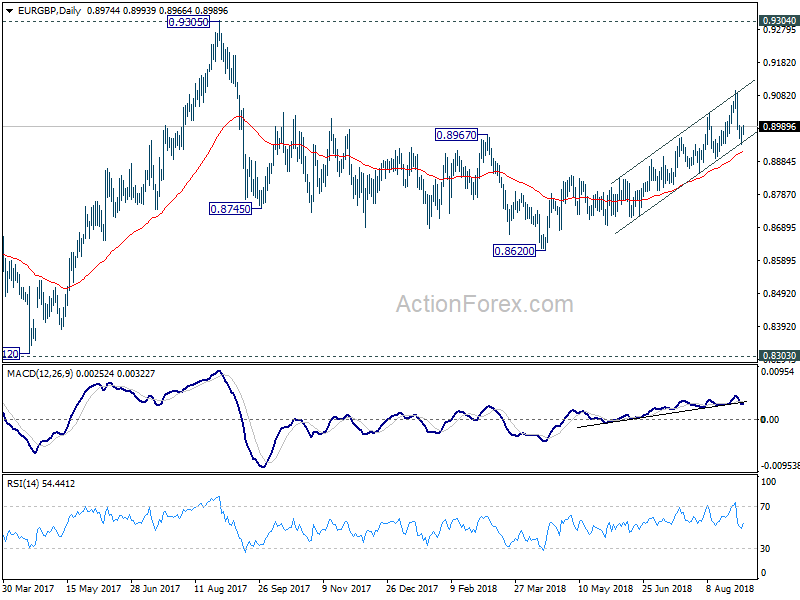

In the bigger picture, EUR/GBP is staying in long term range pattern from 0.9304 (2016 high). The corrective structure of the fall from 0.9305 to 0.8620 is raising the chance that rise from 0.8312 to 0.9305 is an impulsive move. But we’re not too confident on it yet. In any case, we’d stay cautious on strong resistance from 0.9304/5 to limit upside in case of further rally. Meanwhile, if there is another medium term decline, strong support will likely be seen from 0.8303 to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index Aug | 56.7 | 52 | ||

| 22:45 | NZD | Terms of Trade Index Q/Q Q2 | 0.60% | 1.10% | -1.90% | -2.00% |

| 23:50 | JPY | Capital Spending Q2 | 12.80% | 6.60% | 3.40% | |

| 0:30 | JPY | PMI Manufacturing Aug F | 52.5 | 52.5 | 52.5 | |

| 1:00 | AUD | TD Securities Inflation M/M Aug | 0.10% | 0.10% | ||

| 1:30 | AUD | ANZ Job Advertisements M/M Aug | -0.60% | 1.50% | 1.40% | |

| 1:30 | AUD | Company Operating Profit Q/Q Q2 | 2.00% | 1.40% | 5.90% | |

| 1:30 | AUD | Retail Sales M/M Jul | 0.00% | 0.30% | 0.40% | |

| 1:45 | CNY | PMI Manufacturing Aug | 50.6 | 50.7 | 50.8 | |

| 7:15 | CHF | Retail Sales Real Y/Y Jul | 1.20% | 0.30% | ||

| 7:30 | CHF | PMI Manufacturing Aug | 61 | 61.9 | ||

| 7:45 | EUR | Italy Manufacturing PMI Aug | 51.2 | 51.5 | ||

| 7:50 | EUR | France Manufacturing PMI Aug F | 53.7 | 53.7 | ||

| 7:55 | EUR | Germany Manufacturing PMI Aug F | 56.1 | 56.1 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Aug F | 54.6 | 54.6 | ||

| 8:30 | GBP | PMI Manufacturing Aug | 53.9 | 54 |